The question of whether pensions are “sustainable” may get an answer as a CalPERS board action last week ratchets up annual state and local pension costs during the next seven years.

A former CalPERS chief actuary, Ron Seeling, gave pension critics ammunition in 2009 when he said his personal view was that “without a significant turnarounds in assets” the big system could be facing decades of “unsustainable pension costs.”

Now actuarial methods adopted by CalPERS will raise many employer rates to what Seeling worried could be “unsustainable costs of between 25 percent of pay for a miscellaneous plan and 40 to 50 percent of pay for a safety plan (police and firefighters).”

The official CalPERS view ignores the possibility that the big rate increase could squeeze funding for other programs enough to trigger a backlash, perhaps even rekindling fear among public pensions of a switch to 401(k)-style individual investment plans.

Instead, the rate hike is said to be needed to put CalPERS back on the path to full funding in 30 years and build a cushion against another deep economic recession, which could slash investment earnings and pension funding levels.

“This was one of the most difficult, yet most important decisions we have had to make,” Rob Feckner, the CalPERS board president, said in a news release last week. “Moving our plans more swiftly toward full funding will ensure a sustainable pension system for our members, employers and ultimately taxpayers over the long-term.”

Moody’s, a Wall Street bond rater that tracks pension debt, gave the CalPERS rate hike a qualified thumbs up, summed up by a headline in its weekly credit outlook: “Near-term Pressure but Long-Term Positive.”

The new rates do not begin until 2015, giving employers time to plan and adjust. But after years of budget cuts, Moody’s suspects some local governments may “lose their willingness and ability” to make further cuts needed to maintain their credit rating.

“While marginal increases in required pension contributions phased in over five years will likely be manageable for the state and most California local governments, the most fiscally challenged local governments could find these proposed increases unmanageable,” said Moody’s.

“These governments will likely follow the developments in the Stockton and San Bernardino bankruptcy proceedings with even greater interest, since the ability of a CalPERS participant to use the bankruptcy courts to adjust pension liabilities will be a significant issue in these proceedings.”

The giant California Public Employees Retirement System serves state workers, non-teaching school employees and 1,576 cities, counties and special districts that have 2,044 separate retirement plans, each with its own benefits and funding level.

After using complicated actuarial methods that kept a lid on rate increases during the recession, CalPERS switched to a direct method that will show employers how much their rates will increase during the next seven years.

Projected rates shown last week (see benefits committee agenda item 9, attachment 6) show an increase of roughly 50 percent from the current rates after seven years, about half of which was previously planned.

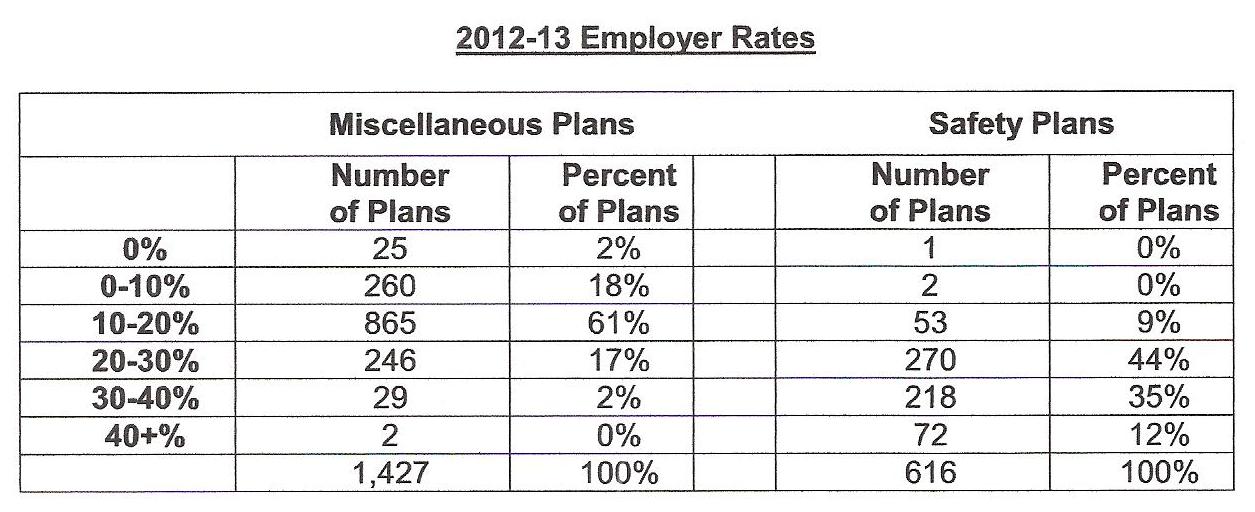

The rates shown are near or above the levels Seeling feared may be unsustainable. But they are medians or middle points, and there is a wide range of rates among the more than 2,000 CalPERS plans.

For example, 72 of the local safety plans for police and firefighters already have rates that are 40 percent of pay or more and 29 of the local miscellaneous plans have rates between 30 and 40 percent of pay. (benefits committee February agenda, item 5d)

Local safety plans with rates of 40 percent of pay or more:72

It’s difficult, through available data, to measure the “willingness and ability” of employers to squeeze funding for other programs in order to pay for the rising cost of CalPERS rates.

When voters in San Diego and San Jose were successfully asked to approve cost-cutting pension reforms last year, some of the debate mentioned cuts in other programs and the growing share of budgets spent on pensions.

Pensions and retiree health care were about 20 percent of the general fund in both cities, which are not in CalPERS and operate their own pension systems. Personnel costs, particularly for police and firefighters, are a big part of city budgets.

A governor’s pension commission report in 2008 said a survey of all 85 public pension systems in California found pension costs among the respondents were “a relatively stable 3.5 to 4 percent” of general fund revenue.

The annual pension cost paid by employers is a firm number. Much of the debate about “sustainable” pensions focuses on the “unfunded liability” or pension debt, a moving target that is not like a mortgage or a bond that must be paid off.

The unfunded liability is usually the shortfall between projected pension costs over 30 years and the projected assets available to pay for them: employer-employee contributions and investment earnings.

About two-thirds of the revenue often is expected from unpredictable investment earnings. Current pension earnings forecasts, 7.5 percent a year, are said by critics to be too optimistic, concealing massive debt.

Using a much lower forecast causes the unfunded liability to soar, as Stanford graduate students showed three years ago. On the other hand, higher than expected earnings, unlikely but not impossible, can erase much or all of the unfunded liability.

The unfunded liability is calculated on the amount needed to be 100 percent funded in 30 years. But pension funds are seldom fully funded. Under the old CalPERS method, the main state worker plan was expected to be 68 percent funded in 30 years.

A third thing that makes the unfunded liability a moving target is the way actuaries value pension fund assets. CalPERS reported two quite different unfunded liabilities on the same page of its latest annual financial report. (See page 128)

Using market value assets, CalPERS reported a funding level of 73.6 percent and an unfunded liability of $86.8 billion. Using actuarial value assets, CalPERS reported a funding level of 82.6 percent and an unfunded liability of $57.2 billion.

CalPERS publicly uses the market value unfunded liability, even though it’s $30 billion higher. A funding level below 80 percent, regarded as acceptable under an old rule of thumb, bolsters the argument for a rate hike.

But among other problems, an actuarial method that “smoothed” asset gains and losses by spreading them over 15 years, well beyond the three to five years used by most pension funds, was difficult to defend as actuary professional groups urge full funding.

The new CalPERS actuarial method will have a single unfunded liability and be more in line with the tighter new rules adopted by the Governmental Accounting Standards Board.

Reporter Ed Mendel covered the Capitol in Sacramento for nearly three decades, most recently for the San Diego Union-Tribune. More stories are at https://calpensions.com/ Posted 22 Apr 13