The question of whether pensions are “sustainable” may get an answer as a CalPERS board action last week ratchets up annual state and local pension costs during the next seven years.

A former CalPERS chief actuary, Ron Seeling, gave pension critics ammunition in 2009 when he said his personal view was that “without a significant turnarounds in assets” the big system could be facing decades of “unsustainable pension costs.”

Now actuarial methods adopted by CalPERS will raise many employer rates to what Seeling worried could be “unsustainable costs of between 25 percent of pay for a miscellaneous plan and 40 to 50 percent of pay for a safety plan (police and firefighters).”

The official CalPERS view ignores the possibility that the big rate increase could squeeze funding for other programs enough to trigger a backlash, perhaps even rekindling fear among public pensions of a switch to 401(k)-style individual investment plans.

Instead, the rate hike is said to be needed to put CalPERS back on the path to full funding in 30 years and build a cushion against another deep economic recession, which could slash investment earnings and pension funding levels.

“This was one of the most difficult, yet most important decisions we have had to make,” Rob Feckner, the CalPERS board president, said in a news release last week. “Moving our plans more swiftly toward full funding will ensure a sustainable pension system for our members, employers and ultimately taxpayers over the long-term.”

Moody’s, a Wall Street bond rater that tracks pension debt, gave the CalPERS rate hike a qualified thumbs up, summed up by a headline in its weekly credit outlook: “Near-term Pressure but Long-Term Positive.”

The new rates do not begin until 2015, giving employers time to plan and adjust. But after years of budget cuts, Moody’s suspects some local governments may “lose their willingness and ability” to make further cuts needed to maintain their credit rating.

“While marginal increases in required pension contributions phased in over five years will likely be manageable for the state and most California local governments, the most fiscally challenged local governments could find these proposed increases unmanageable,” said Moody’s.

“These governments will likely follow the developments in the Stockton and San Bernardino bankruptcy proceedings with even greater interest, since the ability of a CalPERS participant to use the bankruptcy courts to adjust pension liabilities will be a significant issue in these proceedings.”

The giant California Public Employees Retirement System serves state workers, non-teaching school employees and 1,576 cities, counties and special districts that have 2,044 separate retirement plans, each with its own benefits and funding level.

After using complicated actuarial methods that kept a lid on rate increases during the recession, CalPERS switched to a direct method that will show employers how much their rates will increase during the next seven years.

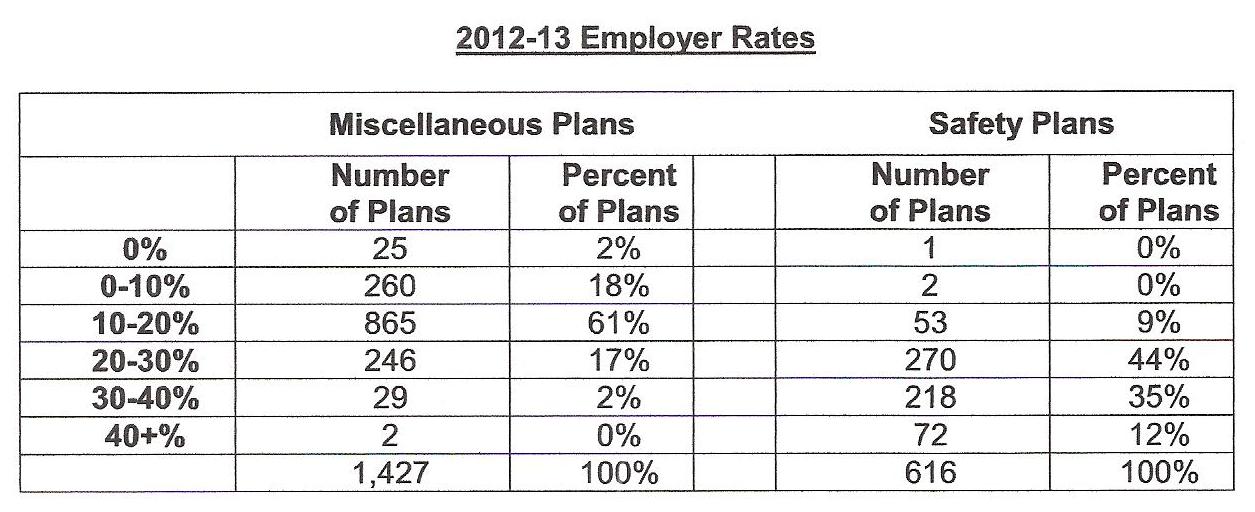

Projected rates shown last week (see benefits committee agenda item 9, attachment 6) show an increase of roughly 50 percent from the current rates after seven years, about half of which was previously planned.

The rates shown are near or above the levels Seeling feared may be unsustainable. But they are medians or middle points, and there is a wide range of rates among the more than 2,000 CalPERS plans.

For example, 72 of the local safety plans for police and firefighters already have rates that are 40 percent of pay or more and 29 of the local miscellaneous plans have rates between 30 and 40 percent of pay. (benefits committee February agenda, item 5d)

Local safety plans with rates of 40 percent of pay or more:72

It’s difficult, through available data, to measure the “willingness and ability” of employers to squeeze funding for other programs in order to pay for the rising cost of CalPERS rates.

When voters in San Diego and San Jose were successfully asked to approve cost-cutting pension reforms last year, some of the debate mentioned cuts in other programs and the growing share of budgets spent on pensions.

Pensions and retiree health care were about 20 percent of the general fund in both cities, which are not in CalPERS and operate their own pension systems. Personnel costs, particularly for police and firefighters, are a big part of city budgets.

A governor’s pension commission report in 2008 said a survey of all 85 public pension systems in California found pension costs among the respondents were “a relatively stable 3.5 to 4 percent” of general fund revenue.

The annual pension cost paid by employers is a firm number. Much of the debate about “sustainable” pensions focuses on the “unfunded liability” or pension debt, a moving target that is not like a mortgage or a bond that must be paid off.

The unfunded liability is usually the shortfall between projected pension costs over 30 years and the projected assets available to pay for them: employer-employee contributions and investment earnings.

About two-thirds of the revenue often is expected from unpredictable investment earnings. Current pension earnings forecasts, 7.5 percent a year, are said by critics to be too optimistic, concealing massive debt.

Using a much lower forecast causes the unfunded liability to soar, as Stanford graduate students showed three years ago. On the other hand, higher than expected earnings, unlikely but not impossible, can erase much or all of the unfunded liability.

The unfunded liability is calculated on the amount needed to be 100 percent funded in 30 years. But pension funds are seldom fully funded. Under the old CalPERS method, the main state worker plan was expected to be 68 percent funded in 30 years.

A third thing that makes the unfunded liability a moving target is the way actuaries value pension fund assets. CalPERS reported two quite different unfunded liabilities on the same page of its latest annual financial report. (See page 128)

Using market value assets, CalPERS reported a funding level of 73.6 percent and an unfunded liability of $86.8 billion. Using actuarial value assets, CalPERS reported a funding level of 82.6 percent and an unfunded liability of $57.2 billion.

CalPERS publicly uses the market value unfunded liability, even though it’s $30 billion higher. A funding level below 80 percent, regarded as acceptable under an old rule of thumb, bolsters the argument for a rate hike.

But among other problems, an actuarial method that “smoothed” asset gains and losses by spreading them over 15 years, well beyond the three to five years used by most pension funds, was difficult to defend as actuary professional groups urge full funding.

The new CalPERS actuarial method will have a single unfunded liability and be more in line with the tighter new rules adopted by the Governmental Accounting Standards Board.

Reporter Ed Mendel covered the Capitol in Sacramento for nearly three decades, most recently for the San Diego Union-Tribune. More stories are at https://calpensions.com/ Posted 22 Apr 13

April 22, 2013 at 3:31 pm

Thanks… you answered one of my questions… about 2% of miscellaneous plans have total contribution rates >30%. 98% are less than that.

Even more interesting would be to split up the costs into normal costs and costs associated with catching the system back up.

It may also be that the plans with the highest payments now had the biggest holidays and/or benefits increases in the past. That would be very interesting information.

April 22, 2013 at 5:06 pm

Its all a matter of proper budgeting. With the new pension reform law, miscellaneous employees will be required to pay up to 8% of their CalPERS contributions and safety will pay up to 11%. After the projected revenue figures are matched with costs of necessary public services, the respective entities will be able to determine how much they can afford to pay each employee, in base salary and other benefits. No entity can afford not to make its CalPERS payments.

April 22, 2013 at 7:23 pm

As I’ve said many times before, we don’t have a pension “FUNDING problem, we have a pension GENEROUSLY problem.

All promised Public Sector pensions need to be HALVED (with a BIGGER cut for Safety workers with the richest pensions) and for CURRENT, not just new workers.

April 22, 2013 at 7:29 pm

SeeSaw, you’re clueless.

If, as you said …”.. projected revenue figures are matched with costs of necessary public services, the respective entities will be able to determine how much they can afford to pay each employee, in base salary and other benefits.”

If that “matching” were done correctly and appropriately, which means paying the full cost of pension and benefit accruals IN THE YEAR EARNED (as they should be), the available funds for pay and benefits would be halved (or less).

And EVERY CA gov’t entity should tell CalPERS to “go stick it”.

April 22, 2013 at 8:13 pm

Of course, in my first comment (above), the word “GENEROUSLY” was supposed to be “GENEROSITY”.

April 22, 2013 at 11:38 pm

spension Says: “Thanks… you answered one of my questions… about 2% of miscellaneous plans have total contribution rates >30%. 98% are less than that.”

– that may be true in the short term but those numbers are set to grow. The numbers also do not include the 15% of cities that also pay social security contributions on top of the pension formula, nor do the numbers include the cost to cities that also pay the employee pick-up.

“Spension says: Even more interesting would be to split up the costs into normal costs and costs associated with catching the system back up.”

– Spension, you can do that yourself. From the 2011-12 “CalPERS Optional Benefit Listing”:

Benefit Formula Employer Normal

Cost:

Pool 1 2% @ 60 Miscellaneous 6.6%

Pool 2 2% @ 55 Miscellaneous 7.7%

Pool 3 2.5% @ 55 Miscellaneous 8.7%

Pool 4 2.7% @ 55 Miscellaneous 9.9%

Pool 5 3% @ 60 Miscellaneous 10.3%

Pool 6 2% @ 55 Safety 13.1%

Pool 7 2% @ 50 Safety 14.0%

Pool 8 3% @ 55 Safety 15.7%

Pool 9 3% @ 50 Safety 17.2%

“Spension says:” It may also be that the plans with the highest payments now had the biggest holidays and/or benefits increases in the past. That would be very interesting information.”

– CalPERS has addressed this issue and Mr. Mendell has written about it. The disparity between plans has nothing to do with the pension holiday that was provided/promoted by CalPERS in an effort to get SB 400 passed. The disparity has everything to do with reduced age requirements, compensation increasing faster than the CalPERS assumptions, addinging many of the “Optional Benefits” CalPERS has made availabe to their members, the “employer Pick-Up nonsense that CalPERS provided, and, last but not least – RETROACTIVE PENSION BENEFITS.

Spension, as you can see (above) the misc. plans have also increased at alarming rates. The top 2@ X pension formula is 9.9 percent of payroll. Yet we have cities already paying above 30% of payroll for the benefit – and those numbers are going way up.

Hardly a bargain!

April 22, 2013 at 11:45 pm

You’re starting to sound a bit shrill again, TL. Perhaps you should dial it back a bit before you become a complete caricature of yourself.

April 22, 2013 at 11:54 pm

BTW, Spension, you can compare those “Normal Costs” to the ones frome 2010-11:

2010-2011 Pool Number Benefit Formula Employer Normal Cost

Pool 1 2% @ 60 Miscellaneous 6.6%

Pool 2 2% @ 55 Miscellaneous 7.7%

Pool 3 2.5% @ 55 Miscellaneous 8.5%

Pool 4 2.7% @ 55 Miscellaneous 9.7%

Pool 5 3% @ 60 Miscellaneous 10.5%

Pool 6 2% @ 55 Safety 11.0%

Pool 7 2% @ 50 Safety 11.5%

Pool 8 3% @ 55 Safety 13.3%

Pool 9 3% @ 50 Safety 15.7%

It will be intersting see how the new CalPERS policy changes impact the “normal cost”.

April 23, 2013 at 1:47 am

SeeSaw Says: “Its all a matter of proper budgeting. With the new pension reform law, miscellaneous employees will be required to pay up to 8% of their CalPERS contributions and safety will pay up to 11%.”

– Peanuts.

“After the projected revenue figures are matched with costs of necessary public services, the respective entities will be able to determine how much they can afford to pay each employee,”

– while figuring out “how much they can afford to pay each employee” has been the M.O. over the past 15 years, without regard to comparable private sector pay, times are changing Seesaw.

” No entity can afford not to make its CalPERS payments.”

– I agree that not paying CalPERS is very costly considering the 7.5% discount rate, and many other factors that can increase the cost, but there are many cities that will struggle to pay CalPERs what they are about to charge. The legal challenges will be interesting.

While I applaud CalPERS for doing the right thing regarding the recent changes in their policy; they’ve created the problem.

April 23, 2013 at 3:15 am

Captain, CalPERS is certainly “doing the right thing” IF we cannot find a way to roll-back these excessive (and as you said, sometime retroactively increased) pensions.

The gross unfairness of the current pensions promises necessitates that all avenues to do so must be explored. Certainly any city or town that winds up in Bankruptcy should pursue a VERY material rollback of these excessive promises. And ALL should consider ending retiree healthcare subsidies … as a proxy for pension reductions where it’s not feasible to do so directly.

April 23, 2013 at 4:00 am

Tough Love Says: “Captain, CalPERS is certainly “doing the right thing” IF we cannot find a way to roll-back these excessive (and as you said, sometime retroactively increased) pensions.

The gross unfairness of the current pensions promises necessitates that all avenues to do so must be explored. Certainly any city or town that winds up in Bankruptcy should pursue a VERY material rollback of these excessive promises. And ALL should consider ending retiree healthcare subsidies … as a proxy for pension reductions where it’s not feasible to do so directly.”

TL, based on many metrics, I completely agree with you.

April 23, 2013 at 5:16 pm

To get some actual numbers rather than exaggerations back in the discussion…

See page 24 of http://www.fixpensionsfirst.com/docs/Full_Report.pdf .

Private pension value (including DC,DB,SS)… about $470,000

at age 62.

Public pension values… ranges from $590,000 (for CalSTRS) to $840,000 (for Local non-safety).

Not a factor of two. At most local non-safety exceeds private by a factor of 1.78. CalSTRS by only a factor of 1.26 .

The real public benefits bonus is healthcare, which has been seriously messed up by… the private sector. The private sector has suppressed competition, just like the railroad and utility monopolies of 100 years ago, and gets taxpayer dollars to pay $1.5 million salaries for healthcare administrators with cost+ contracts.

See http://www.time.com/time/magazine/article/0,9171,2136864,00.html .

I’d be happy with any plan that had an normal cost 30% total contributions for non-safety were those plans that cut back in 1999.

Of course it didn’t help that long ago (more like 1990) conservative politicians threatened to seize `excess’ funds in the California pension systems. Our conservative politicians are just as ignorant about pension math as liberal politicians… overfunding is just an illusion, brought about by securities market fluctuations.

April 23, 2013 at 5:29 pm

The problem with the thinking of both you TL, and Captain, is that the public and private sectors are supposed to operate alike. That is not possible. The private sector must operate for a profit; the public sector is responsible for providing services for the citizens, and protecting and maintaining the infrastructure. The private and public sectors are apples and oranges; there is no comparison and you will never be able to treat them alike.

April 23, 2013 at 5:44 pm

You are both wrong in your thinking that the rank and file workers are in collusion with union bosses and giving out orders to the politicians. As a long-time, former public employee, I can say that retirement is the farthest thing from an employee’s mind when they start out–the big concern is taking home enough to pay the bills, for operating households and providing for the children. I just recently had a conversation with a former, still–active, colleague, who is 20 years my junior. He mentioned to me that he will probably retire at age 57-58. I suggested that, when that time comes, he might want to consider working until he is 60, so that he will get the full 3% that his CalPERS plan promises. My suggestion caught him completely by surprise–he had not looked into how it works.

When I was nearing retirement, at the advanced age I was, compared to my colleagues, I had a chart handy and I knew what that chart promised, on the day we would sign those papers. I cannot imagine going to employees who are now on those, respective, tracks and telling them, “Sorry, we have to redo this, and you will not get what your chart says you will get”. Its not to going happen that way, I am glad to say. There is a pension reform act in effect–let the entities and employees abide by it and stop trying to stab them in their backs.

April 23, 2013 at 5:50 pm

Quoting Spension …”I’d be happy with any plan that had an normal cost 30% total contributions for non-safety ….”

It’s that kind of statement why I believe you or a family member are benefiting from the rich Public Sector pensions. 30% for non-safety would rise to 50+% for safety workers, and being just the “normal cost”, we would need to add another 10-20% of pay to pay off the unfunded liabilities.

Only someone who benefits from these Public Sector pension would support such ridiculously excessive contribution levels when Private Sector workers RARELY get more than their employer’s Social Contribution on their behalf and another 3-5% of pay matching contribution into a 40K Plan.

April 23, 2013 at 5:52 pm

SeeSaw, and how does anything you said justify overcompensating Public Sector workers with these grossly excessive pensions and benefits ?

April 23, 2013 at 5:52 pm

The retiree health care subsidy is of minimum help, TL. My share is more than the subsidy, and it rises and rises–my Part D premiums are $200/mo. when the industry average for separate plans, is $40/mo. The subject of health care is much less predictable than the subject of retirement plans. There is no chart, with an end in sight, for these medical insurance premiums.

April 23, 2013 at 6:27 pm

SeeSaw, Clearly you are living on planet “delusional”.

April 23, 2013 at 6:46 pm

My salary was never excessive and neither were my benefits, TL. My pension is above the average, but modest when you consider the expenses I must cover with such pension. Ninety-eight per-cent of CalPERS retirees are not receiving excessive pensions. I am not in the business of making everyone else’s business my business. I am in the business of going about my everyday life as a responsible citizen of this state and of this country.

April 23, 2013 at 8:01 pm

SeeSaw You won’t get any argument from me about your salary, but the Taxpayer paid-for share of your pension (expressed as a % of pay) should be no greater than that of comparable Private Sector worker doing a similar job …. and I’m CERTAIN your pension (as well as those of all other Public Sector workers) is AT LEAST double that percentage.

There is no justification for this financial abuse of the Taxpayers.

April 23, 2013 at 10:01 pm

There you go again–trying to compare apples and oranges.

April 23, 2013 at 10:06 pm

SeeSaw, Every time you say that you reaffirm your delusional view of the world.

How does working in the Public Sector justify greater taxpayer-funded pension & benefits when you earn no less in cash pay than your Private Sector counterpart ? Do the Taxpayer work for you ?

I’d really love to hear your justification.

April 23, 2013 at 10:28 pm

I never chose the sector to work for. I went to work for the pittance of $1,85/hr. to help put food on the table for my family. So it happened to be a public agency–and it worked out well for me in 40-years’ time. I have no obligation to study the comparisons of my job vs. the same job in the private sector–I have not done that, and therefore have no justification points one way or the other. I am all for good jobs and economic stability for everyone.

April 24, 2013 at 1:11 am

Tough Love saide…. Quoting Spension …”I’d be happy with any plan that had an normal cost 30% total contributions for non-safety ….”

geez, you cut off the …., which was `were those plans that cut back in 1999′. The point is: is the average over time reasonable. The other point is: darned few plans cut back in 1999. `30% total’ was what I said, not just normal cost.

Quoting `Tough Love’ above at 8:01pm:

Taxpayer paid-for share of your pension (expressed as a % of pay) should be …. greater than that of comparable Private Sector worker doing a similar job.

Which convinces me you want exorbinant pensions.

April 24, 2013 at 3:14 am

Spension, Then be clearer in what you say . Your exact words were …”…had an normal cost 30% total contributions for non-safety…”

While that’s a strange combination of words, it certainly sounds like your suggesting 30% for the normal cost even after re-reading it 3 times.

And where you quoted from my earlier comment, you inserted dots where I used the word “no”. I have no idea how my statement could possibly lead to your conclusion….. especially since anyone who has read my comments over time knows that I would be absolutely thrilled to get Public Sector pensions DOWN to the level typically afforded Private Sector workers … which is certainly not “exorbitant”.

April 24, 2013 at 2:48 pm

Right back at you, Tough Love. Anyone who reads my comments knows I think pension payouts got way too high and/or contributions too low. And you eliminated my qualifications in the …. about 1999.

You definitely overstate the value of public relative to private pensions, which are pretty fairly reviewed in:

Click to access Full_Report.pdf

April 24, 2013 at 3:43 pm

Fantastic Frontline last night on the failures of the 401(k) industry…

http://www.pbs.org/wgbh/pages/frontline/

also great link from to Hiltonsmith’s work on the huge $ taken in fees… anyone who says the fees don’t matter is mathematically ignorant…

http://www.cnn.com/2012/06/27/opinion/hiltonsmith-retirement-savings

April 24, 2013 at 5:16 pm

My CalPERS COLA this year will be an extra $87/mo. I will bring home an extra $33/mo. My ABC medical insurance premium- increase will, most likely, be double the amount of my COLA. How come that private sector company gets to do that! I wish I could tell ABC to just, “stick it!”

April 24, 2013 at 7:52 pm

You’re right SeeSaw, read:

http://www.time.com/time/magazine/article/0,9171,2136864,00.html

The most efficient medical plan by far is Medicare, and even its costs are rising way faster than inflation. Private insurance is less efficient and has a way higher rate of cost escalation.

As that article explains, it is the private sector that is driving the breathtaking cost escalation in medical costs.

April 24, 2013 at 9:09 pm

Spension,

You’re wrong. What’s driving medical cost increases, is new and more expensive procedures and drugs, and increased usage, not the least of which is due to an aging population (think Baby Boomers).

That said, I agree that Medicare is MUCH more efficient as to controlling costs, and a single-payor Medicare-for-all healthcare system in America would be a great idea.

April 24, 2013 at 10:09 pm

spension Says: “Fantastic Frontline last night on the failures of the 401(k) industry…also great link from to Hiltonsmith’s work on the huge $ taken in fees… anyone who says the fees don’t matter is mathematically ignorant…”

Spension, so I guess I get to pay my own 401K fees while also paying CalPERS fees: including placement agent fees and SB 400 fees/costs, reduced retirement age fees/costs, retroactive benefit fees, and other extra fees (which compound) for someone else’s retirement plan. So I guess you’re OK with the taxpayer – who seems to be paying a lot of fees for a lot of people, paying both their own fees plus those of public employee union members. Can you see how the cost savings don’t add up? Even the Public Employee unions don’t want to pay more!

From a comment of mine, to you, on the previous Calpensions topic (edited):

“What seems to get lost in the pension formula analysis/contribution rate argument is the acceleration of the base wage and added perks that actually represent the unsustainable foundation of the pension plans. I think CalPERS has claimed that ONLY 25% of the unfunded liability is attributed to the great recession. The rest is the result of accelerated benefits & wages.

Just a quick example, in Vallejo a PD Captain earns 200k per year (before overtime). The pension cost for that employee is over 88K (44.1%).

Here are the Vallejo rates, from CalPERS, for the following years (before the 50% increase):

2013-14: 47.421% (actual)

2014-15: 51.8% (projected)

2015-16: 52.9% (projected)”

Back to today.

CalPERS also claims the “Normal Rate” for the Vallejo 3@50 plan is 16.679% of payroll. But the cost CalPERS is charging Vallejo, and these are 2012-13 numbers, is 47.421 percent of payroll. What category do you want, spensions, to put these ADDITIONAL FEES of 30.742 percent of payroll (47.421 – 16.679%) into?

Spension says, “…anyone who says the fees don’t matter is mathematically ignorant…” On that note, spensions, we agree!

April 25, 2013 at 5:32 am

I don’t know why you make up fantasies like I’m happy with the huge liability makeups beyond the normal cost. I’d be happy with limiting the normal cost to 10% employer, 5% employee, and never a liability makeup that exceeds an additional 5%, and that for no more than 3 years out of 10.

Safety pensions, like 3@50 are outrageously high.

I’m happy with sovereign default of the State of California if reductions can’t be negotiated.

But the *average* public pension value at age 62 of non-safety in California is $590,000 (for Calsters) to $840,000 (local), compared to private pension value (including DC,DB,SS)… about $470,000.

Still too high, but not the outrage of safety.

As for new procedures etc driving medical costs… the new procedures, diagnostic devices, and drugs are sold to hospitals and doctors through an elaborate *private sector* kickback system, which the taxpayer ultimately pays for via cost+ contracting. You can read all about it in the `Bitter Pill’ article by Brill that I’ve referenced.

April 25, 2013 at 12:51 pm

Quoting Spension ….”I’d be happy with limiting the normal cost to 10% employer, 5% employee, and never a liability makeup that exceeds an additional 5%, and that for no more than 3 years out of 10.”

Our self-interested political/Union-controlled structure will NEVER allow that…. which is WHY a switch to DC IS the ONLY answer (and including CURRENT workers).

When time permits, I’m going to take another look at that “fixpensionsfirst” linked article, as I don’t buy that relationship. While it might be true for CA teachers, all other Plans suggest a much wider spread.

April 25, 2013 at 2:11 pm

As for exorbitant post-retirement deals, here is a list of 20 in the private sector (whose companies do loads of cost+ contracting on the taxpayer’s dime) that got $100 million + per payout.

Don’t tell me they `earned them’ or that `shareholder democracy could have fired them’. BS. It is fraud, pure and simple. Getting the taxpayer to pay the `costs’ they rack up (including wildly high salaries) + a few percent due to powerful lobbyists and crony capitalism, usually in health care and in military procurement. And shareholders votes get ignored and evaded.

Not too different from the same lobbying that happens at the state level for pensions. So 50,000 or so safety personnel get $4 million retirements in California… $200 billion or so over 40 years. Just these 20 got on average $200 million each, for a $4 billion total for just them. You can bet that the next 2000 private sector fraudsters and greedsters in the private sector end up with a total equal to the safety payouts in California.

All on the taxpayers back.

Click to access GMI_GoldenParachutes_012012.pdf

April 25, 2013 at 8:44 pm

Spension, It’s an enormous stretch even remotely trying to justify the grossly excessive Public Sector pensions by way of excesses in the Private (VOLUNTARY) sector.

You’re a strange bird, jogging between calling for “sovereign default” (a distraction) as a condition for pension reductions, and an occasional throw-in that Safety worker pensions are excessive (gee wiz … who knew?) … while ALWAYS coming back to trying to justify (or deflect criticism of) the excessive Public Sector pensions, by pointing out excesses in the Private Sector that are hardly relevant.

Dollars-to-donuts you or a family member are riding this Public Sector gravy train and don’t want it derailed..

April 26, 2013 at 5:38 pm

Dollars to donuts you are riding on the graft and corruption rampant in the private sector, like military procurement and contracting, medical sector cost+ and charge master pricing, high fees in investment banking, or the $24 trillion bailout of wall street by the taxpayer, Tough Love.

I call a spade a spade. The private sector and the public sector in the US are equally corrupt.

It is a myth that the private sector is `voluntary’. Private sector lobbyists gouge the taxpayer through cost+ contracting from the government, special fees they charge for doing nothing, zoning regulations that protect existing business, etc.

I’ve always said: if any business voluntarily refuses all government contracts and pledges absolutely no lobbying, advertising, marketing, or any political contributions, they can pay their people what they want (including post-retirement benefits).

As soon as any business does any of those things, most likely they are stealing taxpayers blind, and are just the same as a public union.

April 26, 2013 at 7:22 pm

Never have said sovereign default is a condition for pension reductions.

Voluntary or negotiated reductions are always the first choice, in my opinion.

But the contractual obligations are very strong for the payout of pensions. A U.S. State is not a business or city or county, but a sovereign entity; it cannot go bankrupt. To get out of its contracts (as well as bonded indebtedness), bankruptcy is not an option.

Sovereign default is the only option if voluntary and/or negotiated pension reductions fail.

I do think that if pensions cannot be paid, other aspects of California’s indebtedness must be examined and defaulted upon too.

April 27, 2013 at 12:18 am

Spension, I summed you up quite well when I said …You’re a strange bird.

April 27, 2013 at 5:37 am

And you’re the only person in the US or perhaps the world who things the private sector doesn’t lobby like crazy for taxpayer-subidized trillions, Tough Love.

April 27, 2013 at 2:10 pm

Spension, Again, you are trying to divert attention (from the HUGE need to reduce the PUBLIC Sector pensions of CURRENT workers) by bringing up excesses in the Private Sector which are only marginally relevant, if at all.

Sorry, it’s NOT going to work.

April 27, 2013 at 4:28 pm

Sorry, you’re the one who brings up the private sector pensions as some sort of holy communion. If you never mentioned them I’d not mention the private sector. Your private sector references absolutely prove nothing.

May 1, 2013 at 3:20 am

Tough love is as always a clueless poster. Zzzz

May 4, 2013 at 2:58 am

Ted, You’re a old fool.

Your stupid changing handles say it all.