The debt or “unfunded liability” state Controller John Chiang reported last week for state worker retiree health care, $72 billion, is larger than the unfunded liability for state worker pensions reported by CalPERS in April, $50 billion.

It’s a legislative legacy, a debt for state worker services received by one generation that lawmakers decided to let the next generations inherit.

More than two decades ago legislation created a pension-like investment fund in the state treasurer’s office to help pay for state worker retiree health care. But lawmakers never put money in the retiree health care fund.

Former Assemblyman Dave Elder, D-Long Beach, the author of the legislation (AB 1104 in 1991) said he tried to make a small payment of his own to the fund to publicize the inaction, hoping to create some political momentum.

Another action in 1991 led to what Gov. Brown, in a 12-point pension reform plan three years ago, called the “anomaly of retirees paying less for health care premiums than current employees.”

A cost-cutting move by the administration of former Gov. Pete Wilson began requiring active state workers to pay some of the cost of their health care. No change was made in the payment for health care promised when they retired.

State worker retiree health care still pays 100 percent of the premium of the fully vested retiree (the average cost of several of the largest health plans) and 90 percent of the premium for dependents.

For the health care of active workers, the state usually pays 80 or 85 percent of the premium for the worker, depending on labor contract bargaining, and 80 percent of the premium for dependents.

Brown’s 12-point plan also called for more enforcement of shifting some of the health care costs for eligible retirees to Medicare, the federal health insurance program for persons age 65 and older.

“Contrary to current practice, rules requiring all retirees to look to Medicare to the fullest extent possible when they become eligible will be fully enforced,” said the governor’s plan.

Now Brown, after a pension reform in 2012 and a teachers’ retirement system funding plan last year, is moving on to the state worker retiree health care debt, which the controller estimated has grown $7 billion since a report last March.

“And without action, it will continue to grow by billions of dollars,” a spokesman for Brown’s finance department, H.D. Palmer, said in a statement issued as the controller issued the new report.

“That’s why the governor will put forward a plan to address this unfunded liability — and sustain health benefits for retirees for the long term — when he submits his budget to the Legislature next month,” Palmer said.

Under the 12-point pension reform plan Brown issued in October 2011, state workers would have to work five more years to become eligible for state-paid health care after retirement.

Ten years of service is required to become eligible for retiree health care, which begins at 50 percent coverage and gradually increases to 100 percent after 20 years of service. Brown’s plan pushed the thresholds back to 15 years and 25 years.

But the pension reform eventually approved by the Legislature (AB 340 in 2012) did not include retiree health care. An Assembly analysis of the bill said retiree health care was dropped because unions “have shown a willingness to bargain” the issue.

The Highway Patrol, giving up pay raises for several years, contributes 3.9 percent of pay to the retiree health care investment fund with a state match of 2 percent of pay, said Pat McConahay, Human Resources spokeswoman.

Physicians, dentists and podiatrists (bargaining unit 12) and craft and maintenance (bargaining unit 16) contribute 0.5 percent of pay with no state match to the retiree health care investment fund.

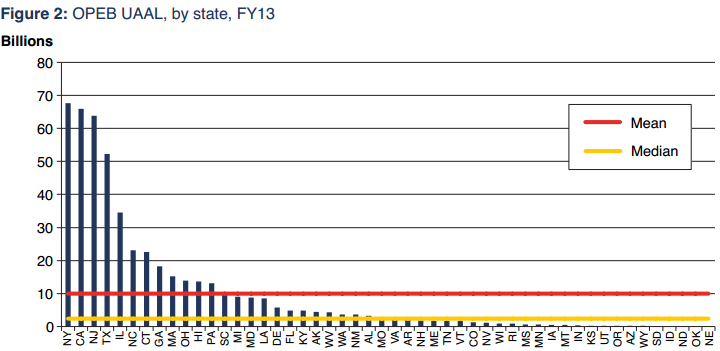

Like California, most states have contributed little or nothing to an investment fund to help pay for the retiree health care they have promised their employees, varying widely in generosity and duration.

The total state unfunded liability (“unfunded actuarial accrued liability”) for retiree health care (“other post-employment benefits”) in fiscal 2013 was nearly $498 billion, or 3.25 percent of national gross domestic product, according to a report issued this month.

More states are beginning to “prefund” retiree health care, setting aside money to invest and yield earnings, said the report by Alex Brown of the National Association of State Retirement Administrators and Joshua Franzel of the Center for State and Local Government Excellence.

Last fiscal year 33 states had set aside a total of $33 billion to “prefund” retiree health benefits, up from 18 states with prefunding in fiscal years 2009-11. Many pension systems expect to get two-thirds of their revenue from investment earnings, the rest from employer-employee contributions.

The growing retiree health care debt was a sleeper issue until the Governmental Accounting Standards Board adopted new rules a decade ago directing state and local governments to calculate and report their retiree health care unfunded liability.

Controller Chiang, elected state treasurer last month, issued the first California state worker calculation in 2007 — an estimated $47.8 billion owed for the retiree health care promised the current workers and retirees over the following 30 years.

Although the long-term debt, $72 billion in the estimate last week, continues to balloon, the cost of health care did not grow as rapidly as expected. Most of the recent debt increase is due to expected longer life spans: 2 years for men, 1.8 years for women.

The state is expected to pay $1.8 billion for retiree health care this fiscal year, nearly all from the general fund. Brown’s 12-point plan in 2011 said state worker retiree health care costs increased more than 60 percent in the previous five years.

In an annual “fiscal outlook” last month, nonpartisan Legislative Analyst Mac Taylor expects state retiree health care costs to grow at nearly the same rate during the next five years, going from $1.8 billion this fiscal year to $2.8 billion in fiscal 2019-20.

The analyst’s report urges the Legislature to “give strong consideration” to using a new debt payment fund created by voter approval of Proposition 2 last month to “pay state, CSU and/or UC retiree health liabilities,” beginning in a few years.

“Not setting aside funds for retiree health benefits earned during employees’ working lives violates a fundamental tenet of public finance — that costs should be paid in the year when they are incurred,” said Taylor’s report.

“The state’s current pay-as-you-go retiree health funding system is much more costly than if the state funded those benefits as they were earned. Accordingly, reducing and eventually addressing unfunded retiree health retirees of public entities could save taxpayers billions of dollars over the long term,” the report said.

Reporter Ed Mendel covered the Capitol in Sacramento for nearly three decades, most recently for the San Diego Union-Tribune. More stories are at Calpensions.com. Posted 22 Dec 14