If not for pension and benefit increases as the stock market boomed more than a decade ago, CalSTRS would be one of the nation’s best-funded large retirement systems with 88 percent of the assets needed to pay promised pensions.

Instead, an annual report said last week, the CalSTRS funding level dropped from 69 percent in the previous year to 67 percent, while the “unfunded liability” or debt increased from $64.5 billion to $71 billion.

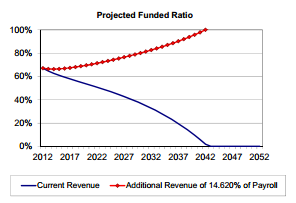

To reach full funding in 30 years, the annual payments to CalSTRS from employers, teachers and the state, estimated at $5.7 billion this fiscal year, would have to nearly double with an additional payment of more than $4.5 billion a year.

In their new report, Milliman actuaries include a calculation, required to see if a small increase in state payments is triggered under an old law, that puts new light on the cost of a half dozen benefit increases enacted around 2000.

“If we were still operating under the 1990 benefit structure, the plan would be about 88.4 percent funded instead of 67 percent,” Mark Olleman of Milliman told the CalSTRS board last week. “So the difference between 88.4 percent and 67 percent shows that one of the impacts on the funding of the plan currently is benefits.”

The Milliman actuaries went a step further with a chart showing how much of the steep drop in CalSTRS funding since 2000 is due to the benefit increases, an issue raised at a board meeting in February by a representative of a retiree group.

CalSTRS was 120 percent funded in 2000 using the market value of assets rather than the actuarial value, which spreads gains and losses over three years. (Using market value, CalSTRS is 62 percent funded now, not 67 percent as with the actuarial value.)

Most of the decline in funding from 2000 through June 30 of last year was due to investment losses. The fund peaked at $180 billion in 2007, dropped to $112 billion in 2009 and was back up to $161.5 billion as of Feb. 28.

But benefit increases enacted around 2000, when CalSTRS briefly reached 100 percent funding after a long climb from 30 percent funding during the 1970s, were a major contributor to the funding decline.

“The blue bars, the biggest one, that is investment returns,” Nick Collier of Milliman said of a chart shown on a vide screen in the board room, but not included in the meeting agenda packet.

“That resulted in a decrease over the entire period of about 46 percent,” Collier said. “The green bars of benefit changes — that resulted in about a 25 percent decrease.”

At a board meeting in February, Lois Shive, who lobbied in 2000 for several benefit increases as vice chairman of the California Teachers Association retirement committee, said a big bill that year was not sponsored by the union.

She said a “rogue member” pushed legislation that quietly converted CalSTRS into a “hybrid” plan by adding to the pension a 401(k)-style individual investment plan with a guaranteed minimum return based on the 30-year Treasury bond. (See Calpensions 15 Feb 13)

For a 10-year period ending Jan. 1, 2011, a quarter of the teacher contribution to the pension fund (2 percent of pay from a total of 8 percent of pay) was diverted into the new “Defined Benefit Supplement” for each CalSTRS member.

The legislation, never heard by a committee, was amended into a bill that previously dealt with credit cards, AB 1509, and passed by the floors of both houses. “The STRS surplus will absorb the cost,” said an unusually brief floor analysis of the bill.

“That was our 2 percent side car that established the DBS fund,” Shive told the board, “and short-funded this wonderful pension fund by a huge amount, building on to what we have now is a snowballing effect.”

Collier told the board last week that the impact of the Defined Benefit Supplement was included in the benefit changes bars on the chart, but could be difficult to see.

“In each incremental year the impact of the Defined Benefit Supplement was very small,” he said. “But if you add it up there also was an impact of the DBS — not as big as the other changes.”

Current CalSTRS funding runs out in 30 years

After years of ignoring CalSTRS requests for more money, the Legislature held a committee hearing last month to begin looking at funding options: What would be the funding level goal and who pays, when and how much?

Unlike most California public pension systems, CalSTRS lacks the power to set annual rates that must be paid by employers, needing legislation instead. But CalSTRS presumably shares a worry with the California Public Employees Retirement System.

The nation’s two largest public pension systems both have low funding levels, and both expect to get about two-thirds of their revenue from investment earnings. Another recession could drop their funding levels below a point of no return.

In the view of experts mentioned at CalPERS, if public pension funding levels fall below a certain point, 40 percent or possibly even 50 percent, reaching full funding would require big rate increases that are politically and financially impractical.

Some might say that CalSTRS is already there, particularly those who think that the current investment earnings forecast used by both funds to offset future pension obligations, 7.5 percent a year, is overly optimistic.

CalPERS kept a lid on employer rates during the recession with a radical actuarial method that spread investment gains and losses over 15 years, rolling amortization periods that refinanced debt every year and other techniques.

The CalPERS investment fund peaked at $260 billion in 2007, dropped to $160 billion in 2009 and was back up to $260 billion last week. The funding level, based on market value assets, was 73.6 percent as of June 30, 2011.

This week the CalPERS board is scheduled to consider a proposal, given tentative “first reading” approval last month, that would switch to a simplified actuarial method that could boost current employer rates roughly 50 percent over the next six years.

While CalPERS can set an annual rate that employers must pay, CalSTRS must compete for funding in the legislative arena. The state budget is back in the black after years of deficits.

But getting the Legislature to approve a long-term funding solution for CalSTRS could be more difficult than cutting a back-room deal to spend the “surplus” on increased benefits.

The priority for politically powerful teacher unions may be restoring deep classroom cuts. A recovering economy may revive hope that investment earnings can get CalSTRS funding moving in the right direction, up not down.

And there is the usual problem with getting things done: Where’s the urgency?

Reporter Ed Mendel covered the Capitol in Sacramento for nearly three decades, most recently for the San Diego Union-Tribune. More stories are at https://calpensions.com/ Posted 15 Apr 13