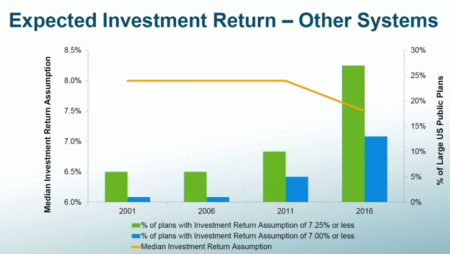

The California State Teachers Retirement System yesterday lowered its investment earnings forecast from 7.5 percent to 7 percent over the next two years, taking a bite out of the paychecks of about 80,000 teachers hired since 2012.

The larger California Public Employees Retirement System cited the same reasons last month while lowering its earnings forecast from 7.5 percent to 7 percent: changing economic conditions and longer retiree life spans.

Both pension boards were told by school groups, who did not oppose the changes, that growing pension costs for teachers in CalSTRS and non-teaching employees in CalPERS are eating into the money needed for students.

A representative of the Association of California School Administrators told the CalSTRS board his group thinks that a school pension cost increase of about $1 billion, before the earnings forecasts were lowered, exceeds the “new dollars” expected by schools.

But representatives of the school employer groups told the CalSTRS board pensions are important to recruit and retain talented teachers, giving their direct or implied support to painful but necessary rate increases.

The lower earnings forecast was phased in over two years to ease the impact on about 80,000 teachers hired since 2012 who get lower pensions under a cost-cutting pension reform. Their CalSTRS rate will increase by 1 percent of pay, up from the current 9.21 percent of pay.

The rate increase is expected to take $400 a year from the average salary of $40,000 for the new teachers. About $200 a year would have been taken if the earnings forecast had been lowered to 7.25 percent as actuaries recommended, a 0.5 percent rate increase.

Board member Harry Keiley, a Santa Monica-Malibu Unified high school teacher, said taking $200 or $400 a year from a new teacher “means something,” but 1 percent of pay during a career of 25 or 39 years to help secure a pension is a deal he would take.

“I also think it’s a reflection of us being good stewards of a system and saying, ‘It’s a good modest pension, and we expect our members to contribut to it, a shared sacrifice,” Keiley said.

Ruben Ingram of the School Employers Association of California told the CalSTRS board its action will help schools face “a severe teacher shortage” by strengthening pensions that are a recruiting incentive.

“Nonetheless,” Ingram said, “rising pension costs both at CalSTRS and CalPERS are pushing our member districts into precarious waters.”

Ingram said school districts project that “before long” 25 to 33 percent of their general funds will be taken by retirement and health benefits. “That’s money that can’t go toward operating expenses like teacher salaries and educational programs.”

Carlos Machado of the California School Boards Association said his group expects the combined CalSTRS and CalPERS rate increases to add $1.8 billion to the annual $60 billion cost facing school districts.

“Those two combined are about $1,300 per student,” Machado said.

The school boards do not oppose the rate increase, he said, but funding is being squeezed for health care, upgrading technology, and implementing curriculum.

Derick Lennox, representing the Association of California School Administrators, told the CalSTRS board that secure pensions are important for recruiting and retaining talented teachers because California school funding trails most states.

He said a new report expected soon from the Legislative Analyst’s Office will show school CalSTRS and CalPERS pension costs increase about $1 billion next year, not counting the cost from the lower earnings forecasts.

Lennox said his group thinks that “exceeds the actual amount of new dollars that we are going to be receiving into the school system.”

CalPERS confirmed an estimate in a CalSTRS report last week that the CalPERS rate for the non-teaching employees of school districts will double as the new rate from the lower earnings forecast is phased in.

A CalPERS chart shows the rate for non-teaching school employees increasing from 13.888 percent of pay this fiscal year to 28.2 percent of pay in fiscal 2023-24.

Jennifer Baker of the California Teachers Association told the CalSTRS board her union appreciated comments about the impact of the rate increase on new teachers. She reminded the board of its long history of pushing for equal pensions among different groups.

“We do want to encourage you to come back to this discussion on the two-tier that is happening at a proper time in the future,” she said.

The action by the CalSTRS board yesterday was the first use of its limited new power to raise rates authorized by funding legislation in 2014. Unlike nearly all California pension systems, CalSTRS lacks the power to raise employer rates.

The funding legislation increased the rate paid by teachers before the reform from 8 percent of pay to 10.25 percent.

The funding legislation will more than double CalSTRS rates paid by school districts, up from 8.25 percent of pay to 19.1 percent by 2020. After that, CalSTRS can raise school district rates to no more than 20.5 percent.

Rates paid by the state to CalSTRS increased from 4.5 percent of pay to 8.8 percent this year. The legislation authorized CalSTRS to raise state rates by up to 0.5 percent a year, reaching a maximum of 23.8 percent of pay before the legislation expires in 2046.

A state budget proposed by Gov. Brown for the new fiscal year beginning in July expected CalSTRS to lower its earnings forecast and trigger a 0.5 percent of pay increase, costing the state $153 million and bringing the total payment to $2.8 billion.

The CalSTRS power over new teacher rates comes from cost-cutting reform legislation that gives lower pensions to employees hired after Jan. 1, 2013, by the state and local governments in CalPERS, CalSTRS and the 21 independent county retirement systems.

The new employees are expected to pay half of their pension “normal” cost, the amount needed to pay for the pension earned annually, excluding the debt or “unfunded liability” from previous years that can be higher than the normal cost and is paid only by employers.

Reporter Ed Mendel covered the Capitol in Sacramento for nearly three decades, most recently for the San Diego Union-Tribune. More stories are at Calpensions.com. Posted 2 Feb 17