A worried Herald Fire Protection District board discussed the possibility last week that the fee for leaving CalPERS may be around $400,000, an amount some members fear could push the small district in southern Sacramento County into bankruptcy.

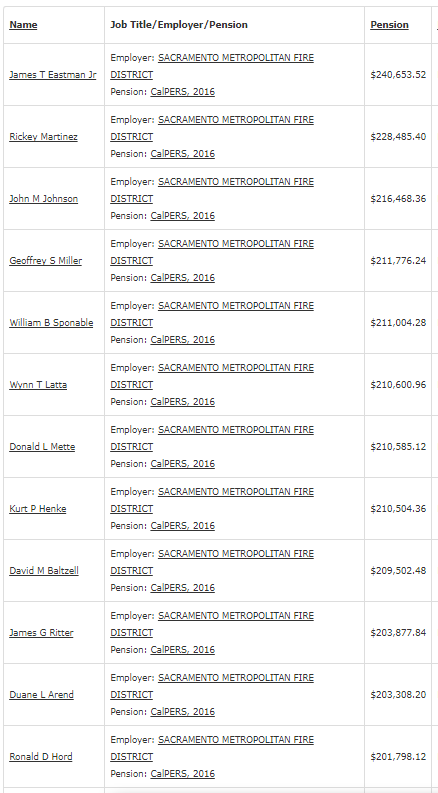

Earlier this month, Transparent California reported that the suburban Sacramento Metropolitan Fire District has 216 retirees receiving annual pensions of $100,000 or more, and a dozen of those are $200,000 or more.

Sacramento Metropolitan was formed from 16 smaller fire districts, several in rural areas similar to Herald. How the large consolidated district and tiny Herald evolved in such drastically different ways might make a good case study of local government efficiency.

Now Sacramento Metropolitan provides some of the most generous pensions in the state. The Herald district, which approved a $655,000 budget last week, filed to leave CalPERS in January 2016 because pension costs were becoming unaffordable.

On the Transparent California list of the 25 local governments with the most annual pensions of $100,000 or more, Sacramento Metropolitan ranks above the city of Sacramento, which is 13th with 167 pensions. The highest is former police chief Rick Braziel at $198,412.

Sacramento Metropolitan also ranks above two large regional districts. The Metropolitan Water District of Southern California is 15th with 159 pensions of $100,000 or more, a half dozen above $200,000. The highest is Gilbert Ivey, $298,233.

The San Francisco Bay Area Rapid Transit District is 24th with 133 retirees receiving pensions of $100,000 or more. Three of the pensions are above $200,000, topped by Gary Gee, $218,666.

Sacramento Metropolitan says it’s the seventh largest fire agency in the state. The only other fire district on the top 25 list, Alameda County, ranked 25th with 126 pensions of $100,000 or more, led by Daniel Berfield, $172,475.

The Alameda County Fire Distict has a smaller staff than Sacramento Metropolitan, 450 compared to 700. But it covers a higher-cost area, particularly for housing, that includes San Leandro, Newark, Union City, Emeryville, Dublin and the unincorporated area of the county.

Sacramento Metropolitan covers eastern and northern Sacramento County and a tiny piece of Placer County. It’s 358 square-mile service area has a population of 738,000 and includes Rio Linda, Citrus Heights, Orangevale, Fair Oaks, Carmichael, and Rancho Cordova.

So, why does Sacramento Metropolitan have what seems to be an unusually large number of retirees with high pensions: 216 receiving $100,000 or more a year, and the top dozen receiving $200,000 or more?

A spokesman said Sacramento Metropolitan firefighters tend to work a full career of three decades. “We do have a higher percentage of employees who reach that level,” Capt. Chris Vestal said in a brief interview, cut short.

Five years ago, a former Sacramento Metropolitan Fire chief, Kurt Henke, was among the local officials who successfully urged the CalPERS board to phase in a lower investment earnings forecast over two years, softening the impact of an employer rate increase.

Henke told the CalPERS board that Sacramento Metropolitan had closed six of 42 fire stations, cut the budget from $159 million to $132 million, and obtained $28 million in labor concessions.

He said the proposed rate increase would cost his agency $2 million to $2.5 million, adding to an expected loss of $6 million in revenue as Sacramento area property values continue to drop.

“You have a lot of local agencies that are on the verge of economic hardship and/or bankruptcy, and to implement this in one fell swoop would push a lot of those entities over the edge,” Henke said.

Top Sacramento Metropolitan pensions (Transparent California)

Herald has told the California Public Employees Retirement System that a termination fee of around $400,000 might push the small fire district into bankruptcy, said Lindsey Liebig, the Herald board chairwoman.

After filing to leave CalPERS last year, Herald waited the mandatory year before completing the exit in January. Liebig said the district was told to expect a final termination fee in four to six weeks.

But Herald is still waiting for the termination fee that could determine its future. The district has retained an attorney and is contesting some of the seven or eight former employees CalPERS thinks are eligible for a pension.

A CalPERS spokeswoman, Amy Morgan, said via email: “The District found some discrepancies for the termination valuation data (i.e., contesting employment classifications, compensation, and dates of employment) that CalPERS is validating in order to issue an accurate final termination valuation.”

Presumably, CalPERS is proceeding wtih caution because it recently cut pensions for the first time when termination fees were not paid by a tiny Sierra town, Loyalton, and a disbanded job-training agency, LA Works.

Herald could be the third round of CalPERS pension cuts, compounded this time by putting a small fire district out of business. But letting Herald off the hook could set a precedent at a time when local governments are struggling with rising pension costs.

The termination fee, due in a lump sum, is controversial. Employers and employees no longer contribute to a terminated pension plan. So CalPERS says the fee must be large enough to invest and cover all of the future costs of pensions.

If the termination fee is not paid, CalPERS cuts the pensions to the amount covered by the employer’s pension fund. The Loyalton pensions were cut by about 60 percent, currently being replaced by city payments, and LA Works pensions were cut by 63 percent, not being replaced.

In 2011 CalPERS sharply increased termination fees. The investment earnings forecast used to calculate the fee was dropped from the regular forecast, now 7 percent, to a risk-free bond rate, now 2 to 3 percent in the termination fee estimates in annual plan valuations.

Several cities, notably Villa Park, considered exiting CalPERS but balked at the high termination fee. The judge in the Stockton bankruptcy called the fee a “poison pill.” Others refer to the old “Hotel California” pop song: You can check in, but you can’t check out.

With new leadership, the Herald district is still responding to a county grand jury report in 2014. “A Firestorm Raging in Herald” said the close-knit community had been torn apart by two years of criticism of the district.

The grand jury said a bank account was not revealed to the county finance department or auditors. Firefighters were not given due process. Staff did not respond to a subpoena for financial information. And the board did not candidly respond to the public at meetings.

Last week, Liebig said a grand jury followup in June criticized the district for not budgeting money for the CalPERS termination fee. She said that would be difficult when the fee amount is uncertain and the district is continuing to spend to make more improvements.

Herald now has only one full-time employee, an administrative assistant, said Liebig. About 30 volunteer firefighters are paid by shift and per call, providing 24-hour staffing with one to three firefighters depending on the shift.

Previously, she said, three full-time firefighters only provided staffing Monday through Friday from 8 a.m. to 5 p.m. Last month the district, which has a 96 square mile service area, responded to 45 calls.

In discussions with CalPERS, Liebig said, estimates of the CalPERS termination fee have ranged from zero to about $400,000. She said the district is in “limbo” while waiting for a fee that may determine whether it continues to operate, closes, or merges with another district.

“I wish they would give us some sort of news, whether it’s good, bad or ugly,” Liebig said.

Reporter Ed Mendel covered the Capitol in Sacramento for nearly three decades, most recently for the San Diego Union-Tribune. More stories are at Calpensions.com. Posted 28 Aug 17

August 28, 2017 at 1:35 pm

Quoting ….

“The termination fee, due in a lump sum, is controversial. Employers and employees no longer contribute to a terminated pension plan. So CalPERS says the fee must be large enough to invest and cover all of the future costs of pensions.”

That statement would be a LOT more accurate if included the addition in parenthesis:

“The termination fee, due in a lump sum, is controversial. Employers and employees no longer contribute (the ludicrously-low contribution levels that CalPERS has charged for decades to make pensions appear far less costly than they really are …… thereby having and keeping in place pension benefit promises MUCH greater than those Taxpayers would agree to if CallPERS told them the TRUE expected costs) to a terminated pension plan. So CalPERS says the fee must be large enough to invest and cover all of the future costs of pensions.”

*****************************************************

And there is ZERO reason why a town should not be able to exit CALPERS while agreeing to pay annually the sum of the employee and employer contributions calculated on the SAME basis that was used befog the termination.

I am astounded that there has (as far as I know) been no litigation on this issue.

August 28, 2017 at 1:40 pm

Excellent article, highlighting the challenge facing many emergency response agencies, including the East Contra Costa Fire Protection District, operating in the Brentwood/Oakley area. ECCFPD is down to three stations from eight, and now regularly declines 911 calls.

Bankruptcy may be the only viable solution.

August 28, 2017 at 2:14 pm

While this article is revealing why did the departments combine? All this did is put the smaller agencies in jeopardy. I am curious what the classification of the high earners are more than the names. It would be easier to determine where the significant cuts can be made before retirement or at hire. This is a spilt milk article and could be a “how do we fix it” one. That should have been the story from the beginning with CalPERS.

August 28, 2017 at 3:09 pm

“And there is ZERO reason why a town should not be able to exit CALPERS while agreeing to pay annually the sum of the employee and employer contributions calculated on the SAME basis that was used befog the termination.

I am astounded that there has (as far as I know) been no litigation on this issue.”

Astounded? LOL! And you tout yourself as a pension expert. I’ll provide you the very simple reason.

A non-terminated pension fund invests money, with market fluctuation along the way. When the market returns are below the assumed rate, an unfunded liability is created and the employer–who legally promised the pension–must contribute to cover that difference. When market returns are above the assumed rate, that offsets the prior dips, and decreases or eliminates the amount that had been required to pay the unfunded liability. This allows for a higher assumed rate of return to be used.

However, in a terminated plan the employer no longer contributes on an ongoing basis. Therefore, if the investments don’t return the assumed rate there are no contributions to pay the unfunded amount. Therefore, the most conservative investment rate is chosen so that no unfunded liability will be created–and the amount that must be deposited upon termination of a plan must be large enough to compound at the lower rate to ensure the legally obligated pension benefits are paid.

August 28, 2017 at 3:57 pm

Pete, you missed the point. Herald is not going out of business and can made additional payments on its unfunded liability, just like every other member. There is no reason to collect the entire unfunded liability payment up front, other than keeping employers in CalPERS. The employer can make payments based upon CalPERS’ actual investment results instead of a very low assumption.

This link will help you better understand the difference between normal cost, paid each year for new services rendered and UAL payments that can be made long after an employer closes its plan to new earnings — https://www.calpers.ca.gov/page/employers/actuarial-services/employer-contributions/public-agency-contributions

August 28, 2017 at 4:45 pm

Pete, You not only “missed the point” (as Daniel Pellissier stated), but apparently (perhaps because you so despise those such as myself who strongly advocate for very material pension reform) that didn’t even read what I stated.

CLEARLY, I called for a CONTINUATION of total (EE + ER) annual pension contributions all made by the City AFTER Plan exit …. and on the SAME basis that they were calculated BEFORE Plan exit.

*******************

And Daniel Pellissier is correct. CalPERS actions in demanding a “termination fee” calculated using a Treasury Rate investment return assumptions are not NECESSARY, but only PUNITIVE, to prevent Towns/Cities from escaping the clutches of union-supporting CalPERS.

August 28, 2017 at 6:47 pm

How is it okay to publish the pension incomes of these retired public servants

August 28, 2017 at 9:41 pm

Responding to H Lynn Massey….

(a) because the Taxpayers are responsible for all but the 10% to 20% of total Plan costs actually paid for by Plan participants (INCLUDING all the investment return on their contributions).

(b) because by seeing what our self-interested, vote-selling, contribution-soliciting, taxpayer-betraying Elected Officials provided Public Sector workers, we can compare that to the pensions typically granted Private Sector workers by their employers. Such a comparison CLEARLY shows that Public Sector pensions ROUTINELY have a “value upon retirement” 2 to 4 times (4 to 6 times for Safety workers) greater than those of COMPARABLE private Sector workers who retire with the SAME wages, at the SAME age, and with the SAME years of service. The upshot is that ALL Public Sector pensions are ludicrously excessive by any and every reasonable metric.

August 29, 2017 at 12:14 am

Quoting H Lynn Massey

“How is it okay to publish the pension incomes of these retired public servants”

……………………

Good question. Perhaps Ed Mendel could answer that question. In about 2005, I refinanced my house, and the state could not even divulge my annual earnings to the bank. I signed a form listing my monthly salary, and the state would only confirm (or deny) my statement.

Since then, there apparently was either a new law, or a court decision, making this information public knowledge. That’s the legal part. If it could be changed, I would support that change.

Ethically, there is no reason to divulge the pay (or pension) of a public employee by name. Yes, it is “taxpayer money”. Fine if the taxpayer wants to know how many janitors work for your local high school, and how much each were paid, including overtime and benefits. OK to publish that a firefighter in Modesto retired at age 56 with 28 years service and a pension of $72,000 annually. No names needed. The State Controller publishes pay and benefits without names. CalPERS could do the same with pensions. No names needed.

Tough Love is incorrect, we can NOT “compare that to the pensions typically granted Private Sector workers by their employers.”

We have no idea how much private sector pay or pensions are for comparable employees.

When Transparent California publishes that information (with names redacted, of course), we can talk.

We can likewise be assured that “Public Sector pensions ROUTINELY have a “value upon retirement” 2 to 4 times (4 to 6 times for Safety workers) greater than those of COMPARABLE private Sector workers who retire with the SAME wages, at the SAME age, and with the SAME years of service.” …

Is total nonsense and…

“The upshot is that ALL Public Sector pensions are ludicrously excessive by any and every reasonable metric.”

Is nothing but propaganda.

August 29, 2017 at 1:44 am

We appear to have a difference of opinion here.

Daniel Pellissier Says:

“There is no reason to collect the entire unfunded liability payment up front, other than keeping employers in CalPERS. ”

Were this true, I assume Loyalton could have successfully sued CalPERS, but they didn’t. Does anyone have actual facts, instead of opinion and conjecture?

I am assuming there is a legal or contractual reason, and further assuming that this is something which could set aside in the case of bankruptcy.

August 29, 2017 at 2:07 am

Quoting SMD …..

“Tough Love is incorrect, we can NOT “compare that to the pensions typically granted Private Sector workers by their employers.”

We have no idea how much private sector pay or pensions are for comparable employees.

When Transparent California publishes that information (with names redacted, of course), we can talk. ”

*******************************************************

Baloney …… all that need to be done is compare the Typical Public sector pension formula (separately for non-safety and Safety workers) to the typical Private Sector pension formula and the results will shake out EXACTLY as I described above ….. notwithstanding SMD’s claim to the contrary.. Specifically:

“Public Sector pensions ROUTINELY have a “value upon retirement” 2 to 4 times (4 to 6 times for Safety workers) greater than those of COMPARABLE private Sector workers who retire with the SAME wages, at the SAME age, and with the SAME years of service. “

August 29, 2017 at 3:41 am

Bee

and

Ess

Where do we find verifiable data on private sector pensions and salaries?

You have already admitted you don’t know Jack about many private sector pensions.

Show me the data!

August 29, 2017 at 4:01 am

Quoting TL:

“the undeniable FACT that Taxpayers are unjustly FORCED to provide you with Total Compensation (via pensions & benefits ROUTINELY 3, 4, 5 even 6 times greater in valise upon retirement than those of comparable and similarly situated Private sector workers) FAR greater than necessary, reasonable, just, fair, or affordable.”

Quoting SMD

“I believe we learned in the case of private sector truckers (average salary $45k – 55k, $4,200 pension @ 60 w/30 years) compared to New Jersey public sector drivers (max salary 48k, $2,556 pension @ 60 w/30 years) ……that “the undeniable FACT”, is in fact, quite deniable after all. Logic would dictate that this is not an isolated example.”

(Burypensions, April 14, 2016 )

August 29, 2017 at 2:59 pm

Oh, Danny Pellissier (and “TL), you amuse with your misleading attempt to rebut. But hey, I’m sure you are enjoying the pension check you get—you know, the one you inflated with your “airtime” purchase of service credits.

August 29, 2017 at 3:03 pm

Quoting SMD ……….

“You have already admitted you don’t know Jack about many private sector pensions. ”

Still with the lies and omissions ?

I’ve stated (in previous posts) that I am NOT familiar with Private Sector UNION (mainly multi-employer) Plans…… whcih includes your “trucker” pension example in your 2-nd comment. This is a VERY small segment of the Private Sector workforce.

I am very knowledgeable about Single-employer Corporate sponsored Private Sector Plans from work experience, and because of THAT knowledge, almost 15 years ago I became aware of and concerned about PUBLIC Sector pension Plans due to their MUCH richer “formulas” and MUCH more generous “provisions”.

August 29, 2017 at 4:22 pm

PBGC… 30 million in single employer, 10 million in multi-employer… Hardly a ” VERY small segment of the Private Sector workforce.”

TL also stated that private sector doctors DEFINITELY do not receive defined benefit pensions… also untrue.

‘There are known knowns. There are things we know that we know. There are known unknowns. That is to say, there are things that we now know we don’t know.’

Donald Rumsfeld

“I am often in error, but never in doubt.”

Tough Love.

Give us a reliable source on private sector pensions AND pay for equivalent public sector workers.

“I am very knowledgeable…” is beyond laughable.

August 29, 2017 at 5:27 pm

SMD, What % of all Private Sector doctors receive Final Average Salary DB pensions (the type granted Public Sector workers)?

I’d don’t know but I’m sure it’s VERY VERY VERY low. Likley the few that get them work as employee-doctors of very large Corporations that have in-house Medical units, and aren’t yet among the vast majority that have already frozen such Plans.

Do you know the % ? If not, why are you blabbering away? If you do know, tell the readers with a linked source.

August 29, 2017 at 6:00 pm

Quoting S Moderation Douglas…

“TL also stated that private sector doctors DEFINITELY do not receive defined benefit pensions…”

Mea culpa, the actual statement was “near-zero probability”…

Tough Love…

“And a Private Sector doctor (other than in a very small practice where they are fully funding it out of their own earnings) getting a traditional-style “final average salary” DB Plan (of the type almost ALL Public Sector workers get) has a near-zero probability.”

“And Please …. don’t weasel* your way out of your intentional mis-statements by claiming that you meant a “Cash Balance” Plan…”

…………………………..

Qui, moi?

Kaiser:

“Your highest average compensation during the ten years prior to retirement is used to derive your highest average monthly salary. Then they take 1/2 of your highest average monthly salary and multiply this amount by 4% for each year of service. For example, a physician who has worked for CPMG for 20 years would receive 80% of 1/2 of his highest average monthly salary.”

When you compute 90% of that fireman’s pay, that’s 90% of $74,000, not 90% of $200,000, or whatever total compensation you dreamed up. The doctor, at age 60, can get 40% of $250,000. Which would you choose? (60%, after 30 years, or 80% after 40)

(Fully company paid, mind you.)

(Pension Reform is BAD for Wall Street, and GOOD for California

California Policy Center, April 14, 2015/by Ed Ring

………………………………………………….

What other professions are you “knowledgeable” about? Attorneys? Accountants? MBAs? Engineers, Marketing?

What is the extent of your “unknown” unknowns?

………………………………………..

*”weasel”, “intentional mis-statements” ? you crack me up.

August 29, 2017 at 8:57 pm

Tough Love Says:

August 29, 2017 at 5:27 pm

SMD, What % of all Private Sector doctors receive Final Average Salary DB pensions (the type granted Public Sector workers)?

……………………..

Tough Love, You not only “missed the point” etc., etc., etc.

Thou art the one who claims to be “very knowledgeable” about Single-employer Corporate sponsored Private Sector Plans.

It was Thee who assured H Lynn Massey that “we can compare that to the pensions typically granted Private Sector workers by their employers.”

And you are asking ME for the data?

…………………………………………………..

And my standard answer.. I don’t care. The average pay for private sector doctors and other professionals is so much higher than public pay, that, even with the allegedly “exorbitant” public pensions, the private sector earns much more in total compensation.

You cannot compare pensions outside the context of total compensation.

……………………………………..

Incredible!…

Typical TL…

“I’d don’t know but I’m sure it’s VERY VERY VERY low.”

Duh!… Now there is some “data” you can count on.

TL…

“If not, why are you blabbering away?”

Good question, TL.

TL…

“If you do know, tell the readers with a linked source.”

If the best link you can get is to “I’m sure it’s VERY VERY VERY low.”, don’t bother.

August 29, 2017 at 10:34 pm

SMD, You’ve answered nothing and just blathered some more. If you know the % of doctors that get Final Average Salary DB Plans state it (with a link).

Now lets do a Comparison of the “value upon retirement ” of the Kaiser Doctor vs your CA Fireman.

First (to get clearer Plan details for the Doctor’s Plan), I Googled “KAISER CPMG” and the first item listed showed the following DB pension Plan details:

******************************************************

“CPMG provides a defined benefit pension plan, funded by the Medical group at no cost to the physician. The plan has a vesting requirement of five years of service. Typically, physicians become eligible for benefits upon their retirement at age 65, if they have at least ten years of qualifying service. Otherwise, if a physician meets the “Rule of 80″ (the sum of your years of service and age equal the number 80), you may retire with full benefits beginning at age 60.

The exact amount of your pension is reached by using a specific formula. Your highest average compensation during the ten years prior to retirement is used to derive your highest average monthly salary. Then they take 1/2 of your highest average monthly salary and multiply this amount by 4% for each year of service. For example, a physician who has worked for CPMG for 20 years would receive 80% of 1/2 of his highest average monthly salary.”

*************************************************************************

Lets work up a comparison working 30 years starting at age 25 (attained age at retirement is 25+30=55).

The CA fireman gets 90% of final (or is it the final 3 years average?) pay, COLA increased thereafter starting at age 55 with no reduction in the otherwise calculated pension for retiring at the young age of 55.

The doctor gets 30x 4% = 120% of 1/2 of his/her “highest average compensation during the ten years prior to retirement”, or 60% of that final average pay. He gets NO COLA increases and because he is retiring 5 years early than the age at which he can get an unreduced pension, his pension is likely reduced by about 25% (5% for each of the ages between 55 to 60 …….. noting that Social Security uses about 6% per-year-of-age in such calculations).

Now lets make them apples-to-apples, and to make it easier to understand I will use a pensionable pay level of $100,000 in both pension calculations.

The fireman gets $90K in year 1, COLA increased thereafter and no early retirement reduction. The 1-st adjustment is to determine the amount of a LEVEL pension equivalent to the fireman’s COLA-increased pension. A COLA-increased pension that begins at age 55 is worth about 30% MORE than an otherwise identical pension but WITHOUT COLA increases. Therefore the Fireman LEVEL-equivalent pension is about $90k x 1.3 = $117K annually.

Next, we need to reduce that $117K equivalent level pension to the share paid for by the Taxpayers (because the Doctor doesn’t contribute to his/her pensions). All of the Fireman’s contributions (INCLUDING all the investment income earned on those contributions) is sufficient to pay for only about 15% of the Total cost of his/her ver rich promised pension. Hence, we need to use only 100%-15%=85% of the $117K = $99.5K.

The Doctor’s pension would be $60K annually IF he was age 60 at the time of retirement, but because he/she is only 55, his level annual pension will be reduced to $60K x .75 = $45K.

The bottom line is that (starting with the SAME final average wages of $100,000) the Fireman’s pension is $99.5K/$45K = 2.2 times that of the Doctor.

This IS (yes it IS) the proper apples-to-apples comparison showing how grossly excessive the taxpayer-paid-for share of the Fireman’s pension is relative to that of the Private Sector Doctor.

Now, from comments you (SMD) made above, I expect you to INCORRECTLY dismiss this 2.2 times multiple by saying that (using your final wages of $74,000 for the Fireman and $200,000 for the Doctor) that the Fireman’s expected level-equivalent pension (adjusted for the COLA-increases) is $99.5K x $74K/$100K = $73.6K annually vs the Doctor’s pension of $45K x $200K/$100K = $90K….. so in absolute $ value the Doctor annual pension is greater.

I’ll be blunt. Undoing the 2.2 times greater Fireman vs Doctor pension relationship via the logic of the preceding paragraph is idiotic, as is effectively tries to erase the deservedly higher salary of the Doctor …. and that his/her pension should be compared to that of the Fireman ….. AS A PROPORTION of his/her salary.

August 29, 2017 at 11:34 pm

I stopped reading at “Now lets do a Comparison of the “value upon retirement ” of the Kaiser Doctor vs your CA Fireman.”

Compare a private doctor to a public one. And compare total compensation to total compensation. Anything else is irrelevant.

August 30, 2017 at 12:03 am

There is no comparison between a firefighter and a doctor. Firefighter got dragged into this because Ed Ring was trying gild the lilly, again, quote…

“Get that? California’s veteran firefighters, whose total compensation averages over $200,000 per year, make as much as the average medical doctor in the U.S.”

Total BS, but there’s a sucker born every minute.

However

Dot, dot, dot

A pipe burst in a doctor’s house. He called a plumber. The plumber arrived, unpacked his tools, did mysterious plumber-type things for a while, and handed the doctor a bill for $600.

The doctor exclaimed, “This is ridiculous! I don’t even make that much as a doctor!”

The plumber waited for him to finish and quietly said, “Neither did I when I was a doctor.”

……………………..

Nyuck, nyuck, nyuck. And a firefighter makes almost as much as a plumber.

Seriously, folks.

August 30, 2017 at 1:14 am

SMD,

The point was easily made by following the path you took …………

That PER $ of WAGES the Fireman’s pension was 2,2 times greater than that of the (VERY FEW) Private Sector Doctors that still participate in Final Average Salary DB pension Plans.

And that’s called “grossly excessive”.

August 30, 2017 at 1:57 am

ir·rel·e·vant

əˈreləvənt/

adjective

not connected with or relevant to something.

synonyms:beside the point, immaterial, not pertinent, not germane, off the subject, unconnected, unrelated, peripheral, extraneous, inapposite, inapplicable; etc.

August 30, 2017 at 4:07 am

For how many years have you been “proving” that public pensions are more generous than private pensions?

How many times, and in how many ways have I already agreed that public pensions (generally) are greater?

It is a given.

It is called deferred compensation.

According to the latest BLS report, for private sector workers, wages are 69.6% of compensation, benefits are 30.4%. for the public sector, wages are 62.9% of compensation, and benefits are 37.1%.

One more time, all the major studies agree that, on average, public sector workers earn wages less than equivalent private sector workers.

THEY ALL AGREE THAT PUBLIC SECTOR PENSIONS ARE HIGHER, ON AVERAGE, THAN THOSE IN THE PRIVATE SECTOR.

The only contention is whether or not the higher pensions are enough to offset the lower wages.

Need I repeat?

1) They all agree that at the higher educated, professional level, pensions and benefits are *not* enough to offset lower wages. Total compensation for the private sector is (much) higher. Ergo, pensions by definition, can not be considered “excessive”, whether they are 2 times, or 4 times, or whether, as in most cases, the private sector has no pension at all.

3) At the lowest educated, unskilled level, public and private wages are similar, so, due to pensions and benefits, total public compensation is (much) greater than the private sector.

2) Logically, in the middle group, greater benefits roughly balance the lower wages, so their total compensation is nearly equal. By definition, their pensions are not excessive.

Ergo, all your math may be correct (or may not be) but it is irrelevant.

Please stop me if you’ve heard this before.

If a private sector doctor earns wages 59% higher (Biggs) than a public sector doctor, in spite of the higher public pension, the private sector doctor will still earn 21% higher total compensation. That’s not a calculation of so-called “typical” formulas, it is the result of studies of actual nationwide empirical data.

To compare two doctors, you cannot just compare their pensions, you must compare total compensation. To compare a doctor and a firefighter is just nuts.

August 30, 2017 at 4:25 am

SMD,

“They all agree” ?

You’re not trustworthy.

Show us, ……………… “ALL” of them.

August 30, 2017 at 5:02 am

Ed Ring doesn’t count. He’s the one who tried to compare a firefighter to a doctor.

And you fell for it.

SMH

August 30, 2017 at 3:22 pm

SMH,

To be blunt, either you’re a charlatan or an idiot*.

The workup I provided above (timestamped August 29, 2017 at 10:34 pm) is not really about comparing a Fireman to a Doctor, but is a demonstration that when using the ACTUAL pension formulas & provisions applicable to each, PER-$1-OF-WAGES the Fireman’s pension is 2.2 times greater in value upon retirement than that of the Doctor.

There is no justification for it to be ANY (yes ANY) greater.

*********************************************************

* actually, I believe you are BOTH.

August 30, 2017 at 5:23 pm

Please stop me if you’ve heard this before.

If a private sector doctor earns wages 59% higher (Biggs) than a public sector doctor, in spite of the higher public pension, the private sector doctor will still earn 21% higher total compensation. That’s not a calculation of so-called “typical” formulas, it is the result of studies of actual nationwide empirical data.

To compare two doctors, you cannot just compare their pensions, you must compare total compensation. To compare a doctor and a firefighter is just nuts.

SMH

August 30, 2017 at 6:38 pm

Posted by Tough Love on April 17, 2016 at 1:57 pm

“SMD (and John ,,, see request at the bottom) ……..

John, I sense you prefer to stay out of the VERY differing positions I and SMD have taken on the “value” of Public vs Private Sector pensions.

But as the actuary-expert as well as host/moderator, how about chiming in. If you think I’m wrong please say so, but if you agree that the value-differences I’ve stated above is essentially correct (obviously noting that specific differences with vary with the specifics of the Plans being compared), please state so as well.

I’m sure many of your readers don’t know whom to believe ……. you owe it to them to respond, given your expertise and experience.

Thanks in advance.”

………………………………….

Posted by PatB on April 17, 2016 at 11:50 pm

Of the actuaries and accountants who must read this blog, I can remember no one defending your math. Maybe this is the time for them to come to your rescue, for the sake of truth, which there seems to be so little of in public pensions.

Who can really understand the opaque rules and numbers that make up these pensions? Obviously not the pols, since they have not made a sound pension decision since before 1990. Not the unions, since they don’t want to be bothered at who will pay for the promises. And certainly not the members, who only understand what is promised, and believe in “the full faith and credit” of government to deliver.

So if anyone supports your math, speak now. If they agree but find fault in it, they should say so, maybe we can all learn something. And if its mostly BS, I hope you can handle the truth.

………………………………

Today, August 30, 2017.

S Moderation reiterates…

If anyone has come forward to verify your math on the “value” of Public vs Private Sector pensions, I haven’t seen it.

Clue me in.

And I just don’t know how many times or how many ways I can explain that to compare pensions independent of total compensation is meaningless. You yourself have said that many private sector workers have no defined benefit pensions. Yet, I say, if their wages significantly higher than the public sector worker (which they often are), then the public worker, even with the “value” of his higher pension, earns *less* than an equivalent private sector worker. THAT is why your “typical” pension math is irrelevant.

Also note, I have repeated many times that some public workers, usually the lower educated workers, because their wages are similar to equivalent private sector workers, have, as a result of their pensions (and retiree healthcare) much higher total compensation.

And the opposite at the higher educated and professional levels. Entirely possible for a public sector doctor to have a pension “value” more than twice that of a private sector doctor, and still have a lower overall compensation.

If you don’t believe this is true, your argument is with the Heritage Foundation. I am simply the messenger.

SMH

August 30, 2017 at 7:08 pm

Quoting SMH ….

“If a private sector doctor earns wages 59% higher (Biggs) than a public sector doctor……”

Source (with LINK) please.

And is that an MD or a PHD ?

August 30, 2017 at 8:32 pm

SMH, I believe I found your source ….. the Biggs AEI study:

https://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=1&cad=rja&uact=8&ved=0ahUKEwja78jT3P_VAhXrz1QKHfiXD6QQFggmMAA&url=https%3A%2F%2Fwww.aei.org%2Fwp-content%2Fuploads%2F2014%2F04%2F-biggs-overpaid-or-underpaid-a-statebystate-ranking-of-public-employee-compensation_112536583046.pdf&usg=AFQjCNEgBoTiN5n3CzTH49fPGFtEW8Bs8A

In Table 4 under the column labeled “Professional” (NOT the PHD column) Private Sector wages are shown as $155,797 while Public Sector Professional wages are shown as $97,685, the ratio of Private to Public Sector wages being 159%. I’m guessing that this was the source of your stated 59% differential in wages.

Just for completeness, further down in that same table, the 59% Private Sector “wage” advangage decreases to 17% on a “Total Compensation” (wages + pensions + benefits) basis.

And of course, the “Professional” column likely includes many occupations beyond doctors, such as Engineers, CPAs, Attorneys, Actuaries, etc.

I do wonder whether the employees in the 2 groups are truly comparable. For example, do they (on average) work the same hours per week? Are they equally “productive” in terms of the quality and quantity of work output? These are important questions because if you routinely work less hours/wk, or are less “productive” you DESERVE lower wages……. and in such cases, being paid LESS barbecue you work fewer hours or are less “productive” is NOT a valid basis to claim that you are underpaid.

Putting that aside, what financially impacts Taxpayers is not the impact of wage or total compensation differential for a SELECTED group of employees (i.e., “Professionals” in this case) but the relationship between Private vs Public Sector Total Compensation for ALL workers taken together.

If one looks at Figure 4 from the SAME AEI study (linked above), it becomes VERY clear that there is a HUGE PUBLIC Sector Total Compensation advantage. In fact, the Private Sector has the “advantage” in only 8 States (with that advantage never rising above 8% of wages) with the Public Sector having the advantage in the other 42 States (with that advantage rising to as high as 42% of wages).

Lets look at those Statistics for your home Sate of CA, and my home State of NJ.

In CA, there is a Private Sector “wage” advantage of 12% of wages (from AEI study Figure 1), that changes to a Public Sector Total Compensation advantage of 23% of wages (from AEI study Figure 6).

In NJ, there is a Private Sector “wage” advantage of 4% of wages (from AEI study Figure 1), that changes to a Public Sector Total Compensation advantage of 23% of wages (from AEI study Figure 6).

It’s just a coincidence that both CA and NJ show the SAME 23%-of-wages PUBLIC Sector “Total Compensation” advantage for all workers taken together………. but it is VERY meaningful.

Taxpayers ……… how much more would YOU have for YOUR retirement needs if YOU had an additional 23%-of-wages every years to save and invest throughout your career ? An extra $500,000, $1 Million, perhaps $2 Million ? Well, THAT is a good estimate of how much Taxpayers are (on average) OVER-COMPENSATING each and every CA & NJ Public Sector worker over their career.

August 30, 2017 at 9:17 pm

It looks like you’re halfway there.

Neither/both. That is from Biggs table 4 (nationwide) data for “Professional”.

Biggs describes it as a “State-private wage differential” of -37%.

Moderation calls it a… “Private-state wage differential” of +59%.

Tomato/tomahto

Please don’t do any more math. That is a quantitative representation of the principle of wage (and total compensation) compression in the public sector. The data is five to nine years old, and, due to data and interpretation difference, probably more of a rough “guesstimate” anyway. If it makes your union hating heart feel any better, that also means that, at the “HS Diploma” level, other researchers concur that public workers earn higher total compensation, and Biggs quantifies it as a 19% positive differential for public workers (or a 16% negative differential for private sector workers).

Anyone else interested, please read …

Overpaid or Underpaid? A State-by-State Ranking of Public-Employee Compensation

Biggs/Richwine, April, 2014.

And especially read his comments on methodology and data sources. One just cannot make a blanket statement that “all” public workers are overpaid OR underpaid. These are just averages. Real compensation will vary from state to state, city to city, even person to person.

TL… If you have difficulty understanding the above, just call it “blather” and move along.

#23%bulls hit

SMH

August 30, 2017 at 10:09 pm

Quoting SMH …..

“The data is five to nine years old……”

LOL………….. Oh, so that study was fine for YOU to reference for your (very selective and hence misleading) 59% greater Private Sector “Professional” category wage advantage, but now that I’ve called you out on how your have selectively distorted the study results (especially for CA and NJ), all of a sudden, the study is based on old/stale data.

Really ?

Yea, I was correct ,,,,,,,,,,,,, you’re BOTH a charlatan and an idiot.

August 31, 2017 at 4:45 am

Apparently, you are a skeptic.

SMH

September 12, 2017 at 4:42 pm

I’ve read a couple articles written by the author now. He could title each article ‘i don’t like pensions, and I’m going to try and make them look unsustainable because i don’t like pensions’.

At any rate. a key concept Ed touches on is that the decrease in investment returns softens the impact on employers’ contributions. This is exactly the opposite of what occurs; he should understand what that means before attempting to draw conclusions from it.

Another note regarding the vast cost a pension represents to employers Ed references, it’s a fixed % of salary for each employee. It isn’t some vague cost that ruins the system, it’s a predetermined amount. Employers contribute approximately 8% of each employee’s salary towards their CalPERS pension. for a reference, the social security contribution all employers pay is 6.2% of each employees salary.

Pensions programs provide actual retirement security for participants. The questions isn’t is it too expensive and should we quit… which is what Ed is not-so-overtly attempting to ask. The question is now do we expand these programs to all lines of employment.

-not a pessimist

October 13, 2017 at 6:32 am

Just saw the comment from Alex……….

Where to begin ?????????????

Ok, how about the obvious, Alex (or a family member) is now or will be receiving a public Sector pension and doesn’t want it’s high generosity (and hence high cost) known.

Quoting …………… “key concept Ed touches on is that the decrease in investment returns softens the impact on employers’ contributions.”

Ed neither stated that directly or indirectly………… period.

Next, referencing your 3-rd paragraph……….

The employEE contribution level is fixed (at an agreed upon % of wages), but the employER contribution is NOT “fixed” in a DB Plan because the employer (meaning the taxpayer) is responsible for the UNKNOWN ultimate cost of the promised pensions in excess of the FIXED contribution (and investment earnings thereon) from the employEES. You know a LOT less about DB pension than you think you do.

Referencing your last paragraph ………….

Pension of the type (Final Average Salary DB Plans) and generosity typical of Public Sector Plans sure do provide retirement security ………….. in fact Public Sector pensions are ROUTINELY 2 to 4 times (4 to 6 times for Safety workers) greater in “value upon retirement” than those typically granted Private Sector workers who retire at the SAME age, with the SAME pay, and the SAME years of service.

Do you think very generous pension formulas, being able to begin collecting an unreduced pension at a very young age (most often in the 50s), and with COLA increases after retirement comes cheap ?

This level of generosity, coupled with the fact that all of the employEES own contributions (including all the investment earnings thereon) rarely accumulate to a sum upon retirement sufficient to buy more than 10% to 20% of the total cost of their VERY VERY generous pensions.

This structure is unnecessary (to attract and retain a qualified workforce), is incredibly unfair to Taxpayers, results in ludicrously excessive pensions, and is clearly unaffordable.

And expanding “these programs” (at the generosity level now granted Public Sector workers) to the Private Sector is patently absurd, because Private Sector employers (that would be spending THEIR money, not Taxpayer money) would never be that STUPID.