The University of California began internal borrowing to pay pension costs six years ago, apparently becoming the model for a state $6 billion loan this year to pay down CalPERS state worker pension debt.

Now UC may inspire others to follow another retirement plan option: offering new hires a choice between a pension and a 401(k)-style plan.

Surprising some, 35 percent of the 6,411 eligible UC new hires chose a 401(k)-style individual investment plan, instead of a pension, during the first 10 months of the new program that began last year, a UC spokeswoman, Claire Doan, said last week.

A new pension funding plan aproved by UC Regents last month — increasing the total loans to $6.4 billion and raising employer rates from 14 percent of pay to 15 percent — only assumes 20 percent of new hires will choose the 401(k)-style plan.

Among California public pension systems, the University of California Retirement Plan has a history of leading, but not always in a good way.

In a record “contribution holiday,” most UC employers and employees did not make payments into the pension system for two decades. Investment earnings covered current and future costs, peaking in 2000 when the system was 156 percent funded.

The need to restart contributions became clear about 15 years into the holiday, around 2005. But for various reasons, including the deep economic recession and a reluctance of the state to resume aid, contributions did not begin again until 2010.

A staff report to the Regents in 2010 said if there had been no holiday and normal cost contributions were made, UC pensions would be 120 percent funded instead of 71 percent funded using market value assets and 86 percent funded at actuarial value.

The California Public Employees Retirement System had a contribution holiday, for employers not employees, when it was more than 100 percent funded, but only for several years. The employer contribution for state workers, $1.2 billion in 1997, dropped to less than $160 million in 1999 and 2000.

Still, the UC system has been better funded than CalPERS (77 percent last year compared to 69 percent) and has a much lower rate for employers than CalPERS (14 percent of pay this year compared to 28.4 percent of pay for most state workers).

The option of a 401(k)-style plan for new workers was recommended by a UC task force. Gov. Brown wanted a cap on UC pensions similar to the one his pension reform imposed on most state and local government new hires four years ago.

UC officials said pensions are important in recruiting top talent, particularly when competing with private universities that offer higher salaries but a 401(k) plan instead of a pension.

The task force proposed that a 401(k)-style plan be added to a capped pension as a supplement and also offered to new hires as a pension alternative. The pension cap became part of a budget deal with Brown that included $436 million over three years to pay pension debt.

Unions usually oppose a switch to 401(k) plans, a private-sector trend shifting the risk of investment losses from the employer to the employee. But some UC unions have agreed to the option, notably 11,000 clerical workers represented by the Teamsters.

A UC guide tells employees to consider the pension if they “expect to work for UC for most of your career” and “want predictable retirement income payments.” Most UC employees contribute 8 percent of their pay to their pension.

The guide tells employees to consider the 401(k)-style plan if they “want a portable retirement benefit you can roll over into an IRA or another employer’s retirement plan if you leave UC” and “are comfortable choosing and managing your investments.”

For the stand-alone 401(k)-style plan UC contributes 8 percent of pay, well above the private-sector average of 3 percent, and the employee contributes 7 percent of pay. For the 401(k) pension supplement, UC contributes 3 to 5 percent, employees 7 percent.

Pension systems that expect to get much of their money from risky and unpredictable investments, like stocks, have a built-in problem.

An economic downturn or stock market crash that cuts investment earnings, creating a pension funding gap, can also squeeze the budgets of employers expected to put more money into the pension system to help close the gap.

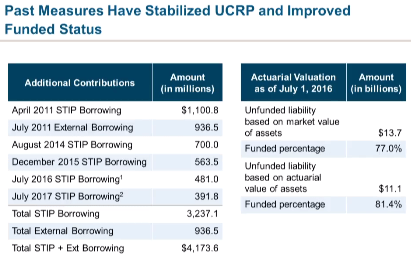

UC campuses got a hard squeeze when employer contributions, restarting in 2010, jumped from zero to 14 percent of pay in five years. To ease the strain, UC began borrowing in 2011 to help make the annual required contribution to the pension system.

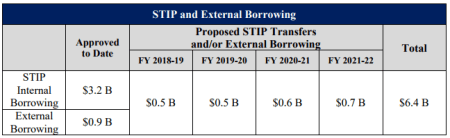

Five internal loans from the Short Term Investment Pool and one external bond issue total $4.1 billion. Last month the Regents approved additional loans totaling $2.3 billion over the next four years, bringing the total to $6.4 billion.

The new loans will be paid off by 2041 through employer payroll assessments. All of the loan assessments and the 14 percent of pay pension contribution are expected to cost employers 18.5 percent of pay by 2021.

A public pension critic, Moody’s ratings service, said in its Weekly Credit Outlook last month that the Regents’ vote to raise the employer contribution and borrow to make supplementary contributions is “credit positive.”

Moody’s thinks the investment earnings forecasts used by public pensions to discount pension debt are too optimistic. So it’s recently used 4.3 percent for California, well above the 7.25 percent assumed by UC and the 7 percent assumed by CalPERS.

Along with the thumbs up for addressing pension debt, Moody’s said UC pension debt is growing: “The university had a $40.5 billion three-year average Moody’s adjusted net pension liability as of June 30, 2016, up from $23 billion as of June 30, 2012.”

A concern of the bond rating services, the Regents were told, is that UC retain at least $5 billion of “liquidity” in the investment pool, money that could be quickly tapped if there is an earthquake or other unforeseen need.

An added loan benefit is that money borrowed at a low rate goes into the pension investment fund assumed to earn 7.25 percent. The interest on all of the loans issued through this fiscal year is expected to be 1.3 to 2.1 percent over the next 10 years.

“Our actuary did an analysis and our funding level is probably six points higher because of this borrowing program,” Nathan Brostrom, UC chief financial officer, told the Regents last month. “In fact, I would say the state has followed our lead in this year’s budget.”

The new state budget borrows $6 billion from the state short-term investment fund to more quickly pay down the debt or unfunded liability for state worker pensions, saving an estimated $11 billion over the next two decades if all goes as planned.

Brostrom said he worked with Brown’s Department of Finance and state Treasurer John Chiang’s staff on the state plan. The borrowed $6 billion doubles the state’s annual contribution to CalPERS this fiscal year.

With the borrowing and contribution increase approved by Regents last month, the UC pension system is expected to be 90 percent funded by 2031. If the funding plan had not been approved, the system would not be expected to be 90 percent funded until 2045.

As the last of the new loans is made in four years, said Brostrom, “obviously we will reassess then whether we have the liquidity or the need to continue that program.”

(CORRECTION: The original version of this post erroneously said the 401(k) plans were part of the budget deal with Gov. Brown.)

Reporter Ed Mendel covered the Capitol in Sacramento for nearly three decades, most recently for the San Diego Union-Tribune. More stories are at Calpensions.com. Posted 7 Aug 17

December 30, 2019 at 3:46 pm

“In a record “contribution holiday,” most UC employers and employees did not make payments into the pension system for two decades. Investment earnings covered current and future costs, peaking in 2000 when the system was 156 percent funded.”

UC as an employer indeed did not make payments in to the pension system.

The UC employees *did* make payment into the *pension system*, just not into the DB portion of it. They had no choice… the amount of their pre-1990 contribution was displaced from DB to DC, but both are under the “UCRS”. The employees had no choice, and couldn’t get the DC $ until after retirement.