Public pension debt took an unusual bite out of taxes in Sonoma County last year, playing a role in the rejection of a ¼-cent sales tax increase by 63 percent of voters.

A broad business-labor-environmental coalition said the tax increase was needed to repair deteriorating streets and roads, reduce traffic congestion, improve transit services, create safer pedestrian and bicycle routes, and allow faster emergency response.

But the opposition ballot argument said that instead of being a specific tax to fund roads, requiring approval of two-thirds of voters, Measure A was a “bait and switch” general tax, only requiring majority approval, that could be used for any lawful purpose.

“It is also well known the County has a generous employee pension plan that has a significant funding deficit,” said the argument. “Probably it is fair to say the drain the pensions have on the General Fund have a role in the County’s motivation to enact this new tax.”

After the vote in June last year, Dan Drummond, Sonoma County Taxpayers executive director, told the Santa Rosa Press-Democrat that voters had spoken loud and clear.

“This shows that there was a real concern about the county’s unsustainable pension costs, and it sends the message that the board of supervisors needs to continue its forward march toward pension control,” he said.

Among the 20 independent county pension systems operating under a 1937 act, Sonoma County has been one of the leaders in trying to control pension costs, pushed by key county supervisors and at least two grass-roots groups.

To get to full funding, many public pension systems rely on rate hikes, mainly from employers not employees, and the all-important but unpredictable pension fund investment earnings expected to pay about two-thirds of future pension costs.

Sonoma supervisors went further in 2011 by adopting a 10-year goal of cutting pension costs from 20 percent of total compensation to 10 percent. Annual pension costs soared from $20 million in 2000 to $113 million last year.

A seven-member citizens committee, including a retired actuary and others with financial expertise, was appointed by supervisors last September to review previous pension reforms and recommend more.

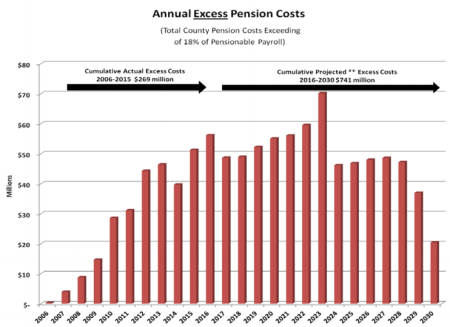

The 95-page committee report delivered to supervisors in July is not only a detailed analysis of a pension system by independent outsiders, but also a rare attempt to measure excess pension costs.

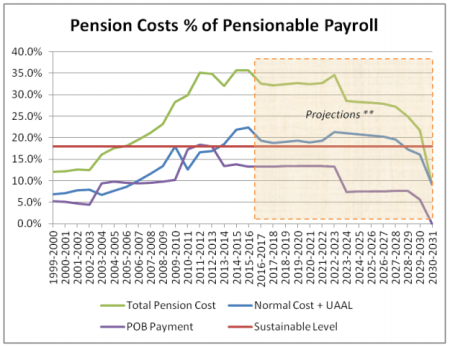

The report restates the county goal of 10 percent of total compensation as a percentage of the pensionable payroll, a more conventional measurement used by the county retirement system, which turns out to be 18 percent of pay.

So, if pensions costing 18 percent of the payroll is considered by the supervisors to be sustainable, said the committee report, then annual pension costs over 18 percent are excess.

“We calculated that cumulative excess costs between 2006 and 2015 were $269 million,” said the committee report. “If the projections of future costs hold true, an additional $741 million in excess costs would be accumulated between 2016 and 2030.”

What could the county do with the excess money spent on pensions? With an additional $10 million a year, said the report, the county could fund 44 additional deputy sheriffs or pay for 40 miles of road improvements each year.

Much of the initial Sonoma County pension funding gap was created by a large retroactive pension increase in the early 2000s, later widened by court decisions expanding pensionable pay and heavy investment losses in the 2008 market crash and recession.

Safety workers got the “3 at 50” formula (3 percent of final pay for each year served at age 50) given the Highway Patrol by landmark legislation for state workers, SB 400 in 1999, which became the standard for urban police and firefighters.

Others got the “3 at 60” formula, the most generous of three higher pensions for local government authorized by AB 616 in 2001. The California Public Employees Retirement System board, despite opposition from its chief actuary, offered to inflate the market value of investment funds to help pay for the higher pensions.

Sonoma County, not part of CalPERS, took a higher road and got workers to pay more for the higher pensions. The average Sonoma worker contributes 10 percent of pay, plus an additional 3 percent for the generous pension.

The employer contribution is 36 percent of pay, said the committee report, which includes 22.4 percent for pensions and 13.3 percent to pay off pension bonds. CalPERS has 135 local governments with safety plan rates over 40 percent of pay.

Sonoma County has issued an unusually large amount of pension bonds. The bonds can stabilize or “smooth” pension payments. But there can be gains or losses, depending on whether the invested bond money earns more or less than its borrowing cost.

The committee report said the Sonoma County bonds have been “beneficial” so far. A $97 million bond issued in 1993 has been paid off. The county issued a $231 million pension bond in 2003 and a $289 million pension bond in 2010.

Now the debt the county owes for pension bonds, $425 million, is larger than the county debt or “unfunded liability” for pensions, $406 million. The committee report said the total debt, $831 million, results in a pension funding ratio or level of 73 percent.

Among the Sonoma County attempts to reduce long-term pension costs are a 7.25 percent earnings forecast to discount future pension debt and no cost-of-living adjustments for retirees since 2008.

CalPERS has a 7.5 percent discount rate, like the California State Teachers Retirement System and UC Retirement, and this year gave more than half of its retirees a cost-of-living adjustment of 1.5 to 4 percent.

Sonoma County also bargained an end to some “spiking” pension boosts before more anti-spiking provisions were included in the statewide Public Employees Pension Reform Act, which gives new hires after Jan. 1, 2013, lower pensions.

The committee report said Sonoma County is on track to cut costs to the sustainable target of 18 percent of pay by about 2030. (see chart below) But that assumes investment earnings will average 7.25 percent, which pension critics say is unlikely.

Sonoma County is a “mature” retirement system, with active workers (4,071 last year) outnumbered by retirees (4,563) receiving pensions. As a result, a small decline in expected investment earnings causes a larger increase in pension debt.

The county’s actuary, Segal Company, estimates that dropping the discount rate from 7.25 percent to 6.25 percent would increase the pension unfunded liability from $406 million to $716 million, presumably triggering a rate increase for employers who, unlike employees, must cover the cost of unfunded liabilities.

The citizens committee recommended a number of changes, including extending the 3 percent supplemental payment beyond the expiration in 2024, if it is not covering the $200 million debt from the retroactive pension increase, as appears to be the case.

The committee urged a push to get employees to share more costs through higher contributions. But with 13 percent of pay for pensions and 6.2 percent for Social Security, workers already have about 20 percent deducted from their paychecks.

A big recommendation would give new hires a federal-style “hybrid” plan combining a smaller pension and a 401(k)-style investment plan. But that would require action by the Legislature, which rejected Gov. Brown’s proposal for a hybrid plan.

San Diego and San Jose voters approved broad cost cuts in city pension systems. But in Ventura County, a judge blocked a vote on a proposal to switch new hires to a 401(k) plan, ruling the 1937 act does not allow counties to terminate their pension plans.

A federal judge ruled bankrupt cities like Stockton and San Bernardino can cut CalPERS pension debt. But the two cities chose not to alter their pensions, saying they are needed to be competitive in the job market, particularly for police and firefighters.

Last month, a state appeals court ruled in a Marin County case that reasonable cuts can be made in the pensions current workers earn in the future, contrary to previous “California rule” decisions that pensions can’t be cut unless offset by a new benefit.

But the state Supreme Court may not agree with the appeals court ruling giving pension reformers a long-sought way to control pension costs. If the unions do not appeal, the appeals court ruling may at a minimum give employers leverage in bargaining with unions.

“We don’t doubt the obstacles that exist to implementing reforms,” said the Sonoma County citizens committee report, “but we are also mindful of the substantial cost to the community of reduced services and/or higher prices for government services due to the substantial costs of pensions.”

Reporter Ed Mendel covered the Capitol in Sacramento for nearly three decades, most recently for the San Diego Union-Tribune. More stories are at Calpensions.com. Posted 6 Sept 16

September 6, 2016 at 1:08 pm

“The report restates the county goal of 10 percent of total compensation as a percentage of the pensionable payroll, a more conventional measurement used by the county retirement system, which turns out to be 18 percent of pay.”

What all state and local governments need to do is cut taxes, tolls and fees to just what is required to pay for “reasonable” and “sustainable” retirement benefits, actual public services, and bonds used to actually expand the infrastructure. Not just replace it on an ongoing basis, which is really just maintenance, or pay for other things.

And then fund the excess costs from the past with separate surcharges that everyone could see. Here is your property tax, and here is your additional “Generation Greed surcharge.” Here is you water bill, and here is your additional “Generation Greed surcharge.” Here is your transit fare or toll, and here is your additional “Generation Greed surcharge.” Let people know that in exchange for these surcharges, they get nothing.

To do otherwise is to continue Generation Greed’s deceptions.

September 6, 2016 at 3:42 pm

Sonoma County is in my view the most corrupt of all the 37 Act systems. Every govt. workers gets 3% of final salary retirement at some age. That happened before the 2008 financial crash.

The Sonoma committee report relied on Retirement system calculations to arrive at the size of the deficit. A market analysis by professor Rauh of the Hoover Institute indicates that because such reports use a 7to8% discount rate instead of market(2.75%), the size of the pension liability is understated by a factor of 3. The liability is three times larger than the sum stated by the plan administrator.

Prof. Rauh recently published a report that concluded that because pension liabilities out grow contributions and investment returns, no matter what, most DB plans will be unable to pay full pensions in just eight years.

BTW, after the Sonoma committee report, the BOS disbanded the committee.

On Aug. 17, the SF court of appeals, in a Marin Retirement system case reviewed the law and correctly found that The California Rule as defined in Casserrley, Kern,Allen and Miller always allowed reduction of pensions if necessary to preserve the ability of the system to pay benefits. Has anyone heard a single govt. atty. announce that because of the case, cities and counties may now reduce pensions for current workers to preserve the integrity of the pension system? Or has any city council person or member of a BOS made such a claim? Why not? Because govt attys. and administrators would be removed by the powerful labor unions if they failed to be untruthful about the ability to reduce pensions.(Casserrley reduced from 2/3 of final salary to 1/2 for current workers w/o off set)

The only pension reform is to replace union owned legislators,govt attys. and administrators with legislators who will establish pension and salary reform. There not a single example of that happening.

September 6, 2016 at 3:57 pm

In this globally competitive world we now live in,we cannot afford to pay for work done in the past.We’re having a hard enough time just keeping the bridges and roads up and running(just barely).

Sorry seniors,I hope you had kids like our competitors.It’s their responsibility now

September 6, 2016 at 4:10 pm

By freely mixing the state systems (PERS etc.) with your discussion of the County’s, you give some readers a false impression. Sonoma County’s system has some aspects that differ substantially from PERS, including:

No COLAs: Sonoma only grants COLAs when excess investment earnings are available, which hasn’t happened recently and is unlikely to happen soon. For most people, it’s a true fixed income with no allowance for inflation. A 401K or IRA to supplement it is needed for inflation coverage in retirement. On the plus side for miscellaneous members at least, it is coordinate with Social Security so once SS starts there’s some inflation coverage (minimal to none in recent years of course, and likely to remain so considering the changes in SS inflation benchmarks).

Formula: 3% at 60 for Sonoma doesn’t work the same as it would at PERS. At Sonoma, that’s the cap – no increase in % after 60. At PERS, the % at Age number is a point on a curve that keeps increasing until the “normal retirement age” – around 65 for miscellaneous members. So 3%@60 in Sonoma is closer in ultimate payment (assuming retirement at 65) to 2.5%@60 for PERS assuming similar final salary.

Spiking: as you noted, Sonoma County acted sooner than many agencies to rein in spiking, and is far better on that score than PERS.

Yes, for those who think all retirees (but especially public retirees) should just die as soon as they retire (such as the rabid anti-taxers), it’s still too much. As far as they’re concerned, ANY pension for a government employee is wrong, as is retirement for anybody but them. But even with the debt for the bonds (which did work out pretty much as they expected) they’re still in better shape than many places and arguably in better shape than PERS. It’s unfortunate that a small tax measure was needed for actually doing things in the County was killed using a largely untrue argument: a “general” tax increase with a list of things it will be used for is standard practice in California and is seldom used for other stuff.

September 6, 2016 at 5:08 pm

Mreky. According to The Pension Tracker, as of June 30, 2013, the Sonoma county pension plan had an unfunded deficit of $2,258,557,431(including pension bonds). It has increased substantially over the past two years. The Tracker uses the “market” cost of retirement benefits. It is independent but consistent with the analysis of Dr. Rauh of the Hoover Institute.

BTW, most genuine pension reformers agree with the Ca. Supreme court that govt. workers are entitled to a reasonable pension, and we agree with that. When crooked county counsels get about $450,000 a yr(like Marin),to prevent truthiness, it is indefensible.

Not to worry, there is not a single reformation plan out there. No govt. agency in Ca. has a reform group willing to even assert an Agenda for perform. Not a single govt. attorney, administrator or legislator. Not one. The power of the govt. unions is incredible.

September 6, 2016 at 5:42 pm

Mereky you are not properly informed about CalPERS. Three percent at 60 is the cap for employees on that formula, which was abolished with PEPRA. The PEPRA formulas are less generous for new employees although they do cap out at later ages. CalPERS abolished pensiion spiking behond the basic salary amount in 1993 and is far ahead of the 37Act County systems in that regard. In case you were unaware, most all public sector plans are paired with supplemental DC plans like the 457B. COLAS are not automatic with CalPERS either–they are bound by CA retirement law and depend on the federal CPI.

September 6, 2016 at 5:46 pm

“perform” should say “reform.”

September 6, 2016 at 5:53 pm

This court case was about egregious pension spiking–not about cutting normal pensions.

September 6, 2016 at 8:53 pm

More and more people are beginning to realize that Defined Benefit plans like public pensions are not sustainable, including the private sector which has more or less done away with them. Here is my solution to this looming crisis that is only going to get worse without any correction of course:

https://drive.google.com/file/d/0B90sU3A85q46OE9BZHJFSWEzbGM/view?usp=drivesdk

Please help spread the word…

September 6, 2016 at 9:48 pm

DC plans have proven to be a disaster… see the case of Penn Specialty… in the end there are no protections against arbitrarily high fees charged by the employer who administers the plans…

Additionally, almost every investment firm that handles DC plans has had a scandal over high fees, or bad advice to move beneficiaries into high cost funds with kickbacks… except for Vanguard, who is the cleanest of all.

DCs are horrible, fraud-and-waste plagued systems, and people’s contributions to them have consequently been meager.

There are quite a few well run public DB systems….

Click to access slp_50.pdf

North Carolina, Wisconsin, South Dakota… etc.

California’s DB systems all have been very poorly managed. However, that is not because they are DB plans, but because they were poorly managed.

September 7, 2016 at 2:40 am

There has never been one pensioner with a legal plan that has been stiffed in the State of CA–a system that is over 100 years old. So if you are going to accuse the CA DB plans of being poorly managed, you are going to have to put forth facts to prove what you say. (I have lived in CA for 60 years and I don’t know of any cohorts in this state who are in financially dire straights due to taxes they have had to pay to sustain pensions)

September 7, 2016 at 4:43 am

Unless Public Sector workers can definitively demonstrate that the SAME job (or one which has comparable risks and which requires equivalent experience, education, knowledge, and skills) and with the same measurable work-product output pays more in the Private Sector, there is ZERO (yes ZERO) justification for Taxpayers to contribute ANY more towards Public Sector pensions and benefits than what Private Sector workers get from their employers ….. generally no more than a 3%-of-pay “match:” into a Defined Contribution Plan and (for only some) a small annual contribution (of a few $100 per year) into a retiree Health Savings account.

It’s WAY PAST time for Private Sector workers to put an end to the VAST overcompensation of Public Sector workers.

September 7, 2016 at 2:18 pm

Here is an article I wrote on the recent court ruling in Marin that allows all sorts of pension changes throughout the state. Ed is correct thought that bringing about these changes will be very difficult and I think will probably require citizens initiatives to achieve reform because board of supervisors and city councils are too afraid of the unions to do anything.

I also worry that even when initiatives are passed the unions will hold up their enactment, which is really dumb when you think about it. Why don’t they want their pension to be secure and to lock in their earned benefits and make adjustments to the system to ensure it is able to pay promised benefits?

http://californiapolicycenter.org/mcera-california-court-ruling-allows-pension-changes/

Also, here is an article John Moore wrote about the pension scandals in Marin and Sonoma counties. It is very frustrating to have people running your government who break the law, steal our future and get away with it because the judges and district attorneys and county counsels will not hold them accountable because they are all part of the pension system and benefited from the crime.

http://unionwatch.org/the-pension-scandals-in-sonoma-and-marin-counties/

September 7, 2016 at 5:38 pm

How can a judge rule on this without having a bias?

They receive the same pensions,do they not?

September 8, 2016 at 11:14 pm

California public pensions were most definitely mismanaged… that is why, for example, current employer contributions for highway patrol are 50.038%. To me, proper management keeps employer contributions lower than 16% at all times. The 3% at 50 was a terrible mismanagement of California public pensions.

September 10, 2016 at 11:27 am

Checked my private defined benefit pension(no col escalator), flat amount. 103%.

We saved for the rest of retirement, minimal cable, used cars, bargain shoppers. I have no desire to pay any more tax for the entitled gov t workers class. No pension after the average age of death when they first enrolled in govt pension plan. Begin this 1/1/2017. Very fair. If they have nothing saved, not my problem. I saved a lot. End of story.

September 10, 2016 at 4:38 pm

The pensions are paid according to the laws ithat have been enacted–not according to your opinion about what is fair or not.

September 10, 2016 at 9:13 pm

SeeSaw,

Certainly MORE accurate with the inserted words …..

“The pensions are paid according to the laws ithat have been enacted – reflecting how hugely successful the Public Sector Union/workers have been via BUYING the favorable votes of Elected Officials (on pay, pensions, and benefits) with campaign contributions and election support – not according to your opinion about what is fair or not.”

September 11, 2016 at 1:52 am

TL–That’s your opinion. If unions are so guilty of buying the votes, of the legislators,how come, then, the beneficiaries of what you consider so decadent are former managers who were not members of unions?

September 11, 2016 at 2:55 am

SeeSaw,

Oh you must be correct. The WORST offenders, Police/Fire with 90%-of-pay (30-yr) pensions aren’t members of “Unions” …. just “Associations”.

AND they often can begin collecting these grossly excessive pensions in their mid-50’s …. vs typically age 65 as the youngest are one can begin collecting an unreduced Private Sector pension.

AND the get annual COLA increases …. that are never included in Private Sector pensions.

————————————————————

Taxpayer are eminently justified in reneging on 2/3-rds of these grossly excessive pensions (AND benefits).

September 11, 2016 at 5:46 am

There are many plans and some are better than others. The higher PS amounts go to the LE professionals in the larger cities. I personally get a modest pension and have no ill feeling toward the public-sector workers who get much more than I. Its much better that people are sustainable rather than clients of the Dept.of Social Services. You and I and everyone else are going to pay taxes, like it or not, and we will also be responsible for those who need help.

Public sector pension COLAs for CalPERS retirees are administered according to CA Retirement Law which is connected to the CPI. CalPERS COLAs are not automatic and you have been informed of that many times–but you still harp on it. I did not get a COLA this year and neither did the PS retirees in my category which is year of retirement. I have received many less than 2% COLAs since I became eligible for that “2%” which is actually “2% or less”.

September 11, 2016 at 3:44 pm

SeeSaw, Oh, so if Police/Fire (and the many others who now get these grossly excessive Public Sector) pensions capped out at $50,000 annually (just about double the SS max) and saved on their own ….. just like all Private Sector workers MUST do …… they would wind up as “clients of the Dept.of Social Services” ?

Really ? Really ?

Nothing you say makes sense.

Employer-sponsored Private Sector retiree pensions get the SAME COLA every year …… ZERO. And without material reduction in the calculated payout (of about 5% per-year-of-age), usually cannot start COLLECTING that annuity until age 65.

——————————————

As I stated above………… Taxpayer are eminently justified in reneging on 2/3-rds of these grossly excessive pensions (AND benefits).

September 12, 2016 at 3:03 am

And TL is going to spend the rest of his life whining about the injustices of public-sector pensions vs.private sector pensions–apples and oranges as far as the the pensions go–otherwise, both are the same–human beings doing the best they can in this world.

September 12, 2016 at 5:14 am

SeeSaw, Please tell us WHY the “injustices of public-sector pensions vs.private sector pensions” (meaning the gross overcompensation of Public Sector workers …… as a group) is “apples and oranges as far as the the pensions go–otherwise”

Public Sector workers are NOT “special” and deserving of a better deal (a FAR FAR better deal) …. on the Taxpayers’ dime.

Yes, both Public and Private Sector workers are human beings, but the insatiable GREED of the former is making life unnecessarily, unjustly, and unfairly difficult for the latter.

September 12, 2016 at 11:00 pm

And so the usual argument goes on. There is a legal way out of the pension debt… California can default on *all* of its debts and then there will be a dogpile to sort out who gets paid with the scraps. Default by states has happened a number of times in US history.

Pensions aren’t the only sweetheart deals handed out by paid-off politicians… there is a lot of bonded indebtedness held by hedge funds, investment banks, etc… and they are just as influential as the unions at getting the politicians to hand out the public $.

A sovereign default would just create a new dogpile as messy as the original one.

Of course, TL solely wants the pension debt to be erased. All sorts of other debt to his friends and allies… well, he wants the State of California to honor that.

Meanwhile, you can read this nice example of how the private sector corruptly tries to abscond with individuals retirement money…

http://www.latimes.com/business/la-fi-metlife-friedman-20160831-snap-story.html

And don’t forget to read about the private sector squandered many DB pensions, often drained to subsidize golden parachutes for the private sector execs…

http://www.retirementheist.com

September 13, 2016 at 1:12 am

Quoting spension …… “Of course, TL solely wants the pension debt to be erased.”

No I do not. What I WOULD like to see (given the grossly excessive Public Sector pensions in place today …. just about everywhere) is:

(a) for the FUTURE service of all CURRENT workers, for their DB pension to be hard-frozen (ZERO future growth) and replaced with DC (401K-style) Plans with a taxpayer-funded %-of-pay “match” EQUAL to that typically granted Private Sector workers by their employers. Yup, I’m STILL calling for “EQUAL, but NOT better”.

(b) given that PAST service accruals (also grossly excessive …. especially the retroactively applied increases) were essentially BOUGHT from our Elected Officials with Public Sector Union campaign contributions and election support, there is ample justification to reduce these as well. But I’m also pragmatic and realize how difficult doing so would be. Therefore, and (only IF (a) above is indeed implemented*) to the extent our cities/states can FULLY amortize existing unfunded liabilities (over no more than 25 years) WITHOUT material reductions in services or increases in taxes, we should try do do so. However, if the existing unfunded liability is so large, or future investment earnings on existing Plan assets so poor, that untenable service reductions or tax increases are necessary to amortize the existing unfunded liability, then YES, the pensions associated with PAST service accruals should be reduced in an amount sufficient to eliminate that burden otherwise foisted on the already betrayed and beleaguered taxpayers.

As for reductions in Bonded debt, etc., while that may also be necessary in a severe scenario (b) situation, I don’t see those who bought these bonds as having colluded with anyone to cheat the Taxpayers (as CLEARLY the Unions and our Elected Officials have done via the promising of these grossly excessive pensions in change for campaign contributions and election support), and as such, see FAR less justification for Bonded debt reductions than for a FUTURE service pension FREEZE and PAST service pension reductions should a dire financial situation make such reductions necessary.

* If (a) isn’t implemented Taxpayers should ….. by whatever means necessary ….. refuse to fund these Plans and simply let them implode. NJ is doing quite well with this approach …. and I support it wholeheartedly.

September 13, 2016 at 7:48 am

OTOH like in San Jose, where many cops decided to head for the exits after pension reform passed, public sector workers do have choices. Fire and police are tough positions and you would see lots of attrition in fire (which be well and good considering they are so few and far between these days, other than wildfire hotshots who are generally not working long enough to be vested) and police (for which there WOULD be a large exodus and/or significant pay increase to make up the difference). Professionals like engineers and attorneys will probably be contracted out, lowering transparency, and prosecutor salaries would probably go up in order to keep criminals behind bars. The DMV worker quality would probably continue to decline because of lack of motivation and high turnover. Also the rate of corruption might increase correspondingly, as happens in developing countries that don’t pay public employees well. Overall, moving to a FERS like system would be more forward thinking than PEPRA, but a too radical shift and you are looking at billions in retraining and fixing errors caused by retirees who head for the exits without secession planning.

September 13, 2016 at 5:03 pm

Are police officers overpaid? Why don’t we just cut their salaries and/or benefits/pensions?

http://www.modbee.com/news/local/news-columns-blogs/jeff-jardine/article101489732.html

September 13, 2016 at 6:14 pm

The model for efficient Government …. Sandy Springs Georgia.

Sick and tired of their Taxes being wasted on over-compensated Gov’t workers, they incorporated into a new City (about 10 years ago). In a city of over 90,000, only Police and a handful of workers are actually City “employees”, and almost all service are outsourced to Private firms.

And NOBODY gets DB pensions, including the Police.

———————————————————————

Taxpayers ….. we DON’T have to put up with with VASTLY over-compensated Public Sector “employees”.

September 13, 2016 at 7:02 pm

TL says “I don’t see those who bought these bonds as having colluded with anyone to cheat the Taxpayers”….

of course you don’t, simply because you intentionally close your eyes.

Cheating the taxpayer is the American way… in fact the Labor Unions in California just are following in the footsteps of developers (like Donald J Trump, who along with his father used political influence for tax breaks, federal payments, favorable loans, and all sorts of $ at the taxpayer trough), defense contractors, private contractors of all sorts, etc, who wield corrupt political influence to enrich themselves.

But TL, you only dislike malfeasance from a portion of the malfeasers who offend you. You don’t mind if your buddies do it.

September 13, 2016 at 7:08 pm

“we DON’T have to put up with with” personal freedom.

http://patch.com/georgia/sandysprings/sex-toy-ban-upheld-sandy-springs

September 13, 2016 at 7:52 pm

CA will never consider sovereign default–you can quote me on that. TL can daydream to his heart’s content.

September 13, 2016 at 8:23 pm

Sorry, Sandy Hills is not the model for efficient government. Nor is Lafayette, California.

http://www.ci.lafayette.ca.us/why-lafayette/lafayette-is-different

Both are enclaves where the household income is two to three times the national average. Sandy Hills didn’t like like paying for the infrastructure and social services of the county (even though that’s where many of them derived their income.)

Both might be examples of what some call the Tragedy of the Commons, the phenomenon where — in a given crowd, one person can stand up to see better, so that is a working strategy, but it becomes decreasingly effective as more people adopt the strategy.

September 13, 2016 at 8:44 pm

Quoting Spension ………..

“TL says “I don’t see those who bought these bonds as having colluded with anyone to cheat the Taxpayers”….

of course you don’t, simply because you intentionally close your eyes.

Cheating the taxpayer is the American way… in fact the Labor Unions in California just are following in the footsteps of developers (like Donald J Trump, who along with his father used political influence for tax breaks, federal payments, favorable loans, and all sorts of $ at the taxpayer trough), defense contractors, private contractors of all sorts, etc, who wield corrupt political influence to enrich themselves.”

———————————————-

That a meaty last paragraph, but none of it has ANYTHING to do with those who bought these bonds. The BUYERS are ultimately families across America. They didn’t collude with anyone to cheat the Taxpayers…… whereas Public Sector Unions/workers CERTAINLY did so in BUYING the favorable votes of our Elected Official (to get these grossly excessive approved) with campaign contributions and election support.

As the beneficiaries of that COLLUSION (in the form of these grossly excessive pensions …. AND benefits), THAT’s where the Taxpayers must look to right this wrong …. by materially reducing these overstuffed pensions.

September 13, 2016 at 8:51 pm

Quoting S.Moderation Douglas …….

“….but it becomes decreasingly effective as more people adopt the strategy.”

Yes, as will the current Police “strategy” of quitting for employment in another town … as MORE AND MORE towns RECOGNIZE and REACT to the massive pension-driven financial ripoff of it’s citizens, by materially reducing future service pensions.

The CA Courts (Marin County vs Public Sector “spikers”) recently cracked-open the door to such reductions. Arguably small now, but sure to expand.

September 13, 2016 at 9:21 pm

Sandy Springs, Georgia

“If sex toys are outlawed, only outlaws will have sex toys.”

September 14, 2016 at 12:14 am

TL… “The BUYERS are ultimately families across America. They didn’t collude with anyone to cheat the Taxpayers……”…

Yes, little families like Goldman-Sachs. Horsedoodles, the big bankers own trillions in California debt, and you are seeking to divert attention from their corrupt political influence by diverting attention away from corruption by your buddies, and focusing it on people you perceive as enemies…. like, my grammar school teachers, who (according to the Transparent California sight) earn a few thousand a month from the pensions for their 40+ years of service to public schools.

How dare you equate Goldman-Sachs with my grammar school teachers… Goldman-Sachs and your other buddies take corruption to a level that is epic and hidden by you.

I freely grant… there are a lot of pension situations in California that are outrageous and the result of influence by unions like the safety unions.

But you will never admit that you are just shilling for the extremely corrupt Defined Contribution industry, a portion of the incredibly corrupt American financial industry, which wants to charge exorbitant fees and skim regular people’s retirement money.

You and that industry rage against the DB pension systems for one reason only: you want to skim its riches yourself.

September 14, 2016 at 1:22 am

Always need to look forward to the tax avoidance so this household pays it fair share and nothing more. Renting a truck to go shopping in Nevada this weekend. Have 20 gallons of gas purchased in Nevada to top off the tank. It is a great family event. The Cal govt is evil and the pensioners are thiefs. They break natural law for greed. We track the little sales tax paid in Cal. on a blackboard in the kitchen. My 9 year old son says it best we would rather steal it than pay Cal taxes on it.

September 14, 2016 at 1:48 am

Quoting spension …………….

“TL… “The BUYERS are ultimately families across America. They didn’t collude with anyone to cheat the Taxpayers……”…

Yes, little families like Goldman-Sachs….”

spension, Goldman-Sachs (and similar Wall Street firms) are the “underwrites” of these Bonds issues. They hold (i.e. “own”) little (if anything) in their own portfolios. They ultimately get bought (i.e., owned) by American (and International) families throughout the world.

Sure, SOME buyers are the Trust funds of wealthy individuals & Families looking to invest conservatively in tax-preferenced products, but none of these buyers cheated the Taxpayers as have Public Sector Unions/workers.

—————————————————-

Quoting spension again ………

“How dare you equate Goldman-Sachs with my grammar school teachers… Goldman-Sachs and your other buddies take corruption to a level that is epic and hidden by you.”

OMG …… read my reply above ….. and take some economic/finance classes.

——————————————————–

Quoting spension ………….

“But you will never admit that you are just shilling for the extremely corrupt Defined Contribution industry”

You and your ilk are all alike. When logic can’t counter reasoned argument, all you have left is to call us “shills”. Grow up. ….. and I have not, do not, and will not earn even one dime from DC products (in any way, shape, or form).

September 14, 2016 at 4:35 pm

From Tough Love “but none of these buyers cheated the Taxpayers as have Public Sector Unions/workers.”

As you say, you don’t have a reasoned argument, and so you assert without evidence that holders of California Debt *have not* cheated through political influence. Balderdash… the entire financial industry and other wealthy interest groups has a fleets of lobbyists that is every bit as powerful as Public Unions, and you are denying that entirely.

And you deny the epic corruption present in the DC industry… the reasoned argument is…. Penn Specialty Chemical, among many others, who charge outrageous fees to drain 401ks and IRAs. You do exactly what you accuse me of doing.. all you have left is to point fingers at cases where the public unions do exactly what they were taught to do by the US private sector… influence the political process.

In the end, you completely tolerate influence and corruption by your own buddies, but only point fingers at your enemies. Everyone here gets that.

September 14, 2016 at 6:22 pm

Spension,

The focus of your above (and your prior) comment is that MY POSITION ….. that the buyers (i.e., owners) of Public Sector bonds have not cheated Taxpayers as have Public Sector workers via their grossly excessive pensions granted AS A RESULT OF their Union’s BUYING of the favorable votes of our Elected Officials with campaign contributions and election support … is negated by the misdeeds of “the entire financial industry and other wealthy interest groups has a fleets of lobbyists that is every bit as powerful as Public Unions”.

I am not arguing that the financial industry and other wealthy interest groups don’t exert influence similar to Public Sector Unions. but that these entities are NOT the buyers/owners of Public Sector Bonds. When you call for default on these Bonds you are calling for financial punishment of the OWNERS of these bonds, not the Private Sector entities you so detest.

The Bonds owners haven’t cheated the Taxpayers, so why punish them (outside of bankruptcy, which changes to whole picture)?

———————————-

And ……….. I have ZERO financial interests in DC products and agree that 401K fees have been excessive in numerous examples.

However, NOTHING can overcome the Politician’s willingness to lie, cheat, steal and collude to be re-elected, and those “issues” have manifested themselves as grossly excessive, unnecessary, unjust, unfair (to Taxpayers) and clearly unaffordable DB pensions.

Combine that with the lack of transparency, complexity, and need to make many forward-looking “assumptions” in DB Plans, and we have a recipe for ripping off the Taxpayers ….. as HAS BEEN, as IS NOW, and as WILL CONTINUE until DB Plans are eliminated from the Public Sector arena.

September 14, 2016 at 9:58 pm

TL says “but that these entities are NOT the buyers/owners of Public Sector Bonds.”

And there is Suze Ormand with the bulk of her fortune invested in California Munis.

And all the investment banks like Goldman who are middleman who buy & sell munis with outrageous techniques, often parking them and backdating sales to “earn” profits that aren’t taxed highly because they fall under carried interest. A corrupt middleman who does that stuff is just as bad as a corrupt owner, and for sure Goldman and others own a huge amount themselves through various shell structures that make the ownership very hard to trace.

I agree that “Politician’s willingness to lie, cheat, steal and collude to be re-elected, and those “issues” have manifested themselves as grossly excessive, unnecessary, unjust, unfair (to Taxpayers) and “…. give incredible profits to the holders of California debt through never closing all the loopholes that the Politicians give the rich entities who hold California debt.

So well hidden you wouldn’t begin to hear about it until the Sovereign debt got serious… wait… it is the Hedge funds who surround Puerto Rico already like vultures. Would be the same in California, only worse.

DB plans got out of control in California, but all over the US there are perfectly fine DB plans. Just about every DC plan (only exceptions I know are Vanguard & American Funds) has had vast corruption that out-does the DB situations in places like California, Illinois, Rhode Island etc. It is just that the DC industry is far better at owning politicians and those politicians protect them even better than the politicians that spiked some DB plans got protected.

And that doesn’t begin to cover what happened to the Private Sector DB plans, whose demise was well covered in:

http://www.retirementheist.com .

Corruption is endemic in the US, but worst in the Private Sector.

September 14, 2016 at 11:08 pm

Quoting spension ……….

“And there is Suze Ormand with the bulk of her fortune invested in California Munis.”

So what ? She’s a wealthy woman who evidently has chosen to invest conservatively in tax-preferenced Bonds. She didn’t CHEAT the Taxpayers by buying these Bonds …. as have our Public Sector Unions/workers via their collusion with Elected Officials to grant pensions far greater than necessary, fair (to taxpayers) or affordable, in exchange for Public Sector Union campaign contributions and election support.

——————————————————-

Quoting spension ….

“And all the investment banks like Goldman who are middleman who buy & sell munis with outrageous techniques, often parking them and backdating sales to “earn” profits that aren’t taxed highly because they fall under carried interest.”

All BS. A Bond buyer knows the date of purchase ……. period. If GS “owned” the Bonds over a short window for issue date to final sale (which may be true) they will earn the coupon rate over the period held and pay normal corporate rate taxes…. such earnings are NOT “carried interest”.

———————————————————–

Quoting spension ……….

“… wait… it is the Hedge funds who surround Puerto Rico already like vultures……”

The PR situation is unique in the extreme insolvency. Here the “owners” of these Bonds are indeed hedge funds GAMBLING that default will be avoided (likely via some form of American Taxpayer bailout) and that they will make a tidy profit based on the low prices that they have paid to buy them.

Understandably objectionable to many, but they ARE operating in a transparent environment and any individual can buy these heavily discounted bonds if that suits their appetite for risk and their own evaluation of potential reward. I still see no COLLUSION as takes place between the Public Sector Unions and the Elected Officials they BUY with Union campaign contributions.

Quoting spension ……..

“DB plans got out of control in California, but all over the US there are perfectly fine DB plans.”

Please identify these Plans in “fine” shape ….. but “fine” NOT when measured under the phony GASB accounting standards that only Gov’t entities are allowed to use, but “fine” if valued on the SAME basis that the US gov’t requires of Private Sector Plans. Under the latter there are VERY VERY VERY few Public Sector Plans that are in “fine” shape…… meaning without material unfunded liabilities.

September 15, 2016 at 12:39 pm

TL says.. “Please identify these Plans in “fine” shape ….. “… portions of the New York, Wisconsin, Delaware, North Carolina, Washington State, South Dakota, Tennesee, Idaho. There are many more when broken down by localities. I’ve posted links to reports here many times.

Amazing, TL, that you deny the existence of influence just as corrupt by the private sector, particularly the private finance sector, on the US political system. You live in an ignorant bubble. The thought that *any* major private sector in the US operates in a transparent environment is a BIG LIE. When you get Trump’s tax returns, come lecture about transparency. Or if you ever get the list of companies and lobbyists that Dick Cheney invited into the Oval Office during the GW Bush administration, or if you ever get GHW Bush prosecuted for perjury because he denied the existence of his diaries to Republican (and heroic) Lawrence Walsh, lecture about transparency. I could list the Democratic versions too.

The simple fact is: the private sector is every bit as corrupt as public unions.

You also extol the need to make public pensions as awful as the current private pensions system, without ever addressing the simple fact that corrupt private companies lobbied and bribed their way to draining their pension funds of resources, as documented by the Wall Street Journal reporter who wrote

http://www.retirementheist.com .

And don’t forget… the ability of public pension funds to invest outside of conservative bonds was extolled as a virtue by the private sector back in the day! George W. Bush wanted people to invest their social security money in stocks! And when the Social Security system invests in treasuries, the right goes wild and accuses the US Government of a Ponzi scheme! I guess people like you only want China and Japan purchasing US debt, and not the good old little guy here in the US.

But when Hedge funds invest in munis, that is because they are totally honest, penny-pinching New Englanders. Hahahaha. Hedge funds and Wall Street are really far more corrupt than any public union in California: Congress and the State Legislators live in their pockets.

Amazing that you view Suze Ormand as a “little family” but my kindergarten teacher (pushing 98) and my sixth grade teacher (pushing 95) who each taught in California schools for 40+ years as criminal colluders.

September 15, 2016 at 10:02 pm

spension,

You keep repeating in how fine shape many DB Plans are…… but only when valued under phony definitions of “fine”. The American Academy of Actuaries has debunked the MYTH that 80% funding ratios are ok and that the goal should ALWAYS be 100%. That’s the target for Private Sector Plans valued under FAR more strict standards. In fact under these FAR more strict standards REQUIRED BY THE US GOV’T of Private Sector Pans, if the funding ratio drops below 80% Plan restrictions kick in, and if it drops below 60% no further pension accruals are allowed*.

While there are other differences, the primary difference between Public and Private Sector Plan valuations is that while Public Sector Plans ALWAYS calculate Plan liabilities by discounting future expected payouts using the same interest rate as that assumed for earnings on Plan assets (in the 7% to 8% range), Private Sector Plans MUST discount expected future payouts using long term high quality Corporate bond rates (now in the 3 to 4% range).

A pension valuation using long term high quality Corporate bond rates will (on average) result in a funding ratio roughly 1/3 lower than a pension valuation using the investment return assumption. Therefore, for a Public Sector pension Plan to REALLY be in “fine” shape (meaning having a 100% funding ratio if valued the way Private Sector Plans MUST be valued), the Public Sector Plan should have a published funding ratio of 150% ……… because 150%-(150%/3) =100%

So please spension …….give us a list of Public Sector DB Plans with published funding ratios of 150% or greater.

——————————————————————-

* The 60% funding ratio cutoff under which Private Sector Plans are barred (by US Treasury regulation) from crediting further pension accruals, being developed using Corporate bond rates for discounting expected future payouts, corresponds to a 90% funding ratio if the liability calculation uses current PUBLIC Sector methodology (i.e., using the investment return rate assumption for discounting expected future payouts)…. because 90%-(90%/3)=60%.

How many Public Sector Plans publish funding ratios BELOW 90%, CalPERS now being about 65%? I don’t know, but I’d guess that it’s CERTAINLY over 3/4 of all Public Sector Plans, and perhaps even 95% of all Public Sector plans. If these 70% (perhaps 95%) of all PUBLIC Sector Plans had to follow the IDENTICAL regulations that the U.S. Gov’t REQUIRES of Private Sector Plans, none of them would be allowed to credit any further pension accruals.

THAT’s how bad it is when is Public Sector Plan lying, cheating, collusion, and extreme dishonesty is stripped away.

September 16, 2016 at 12:11 am

spension,

I already responded above to your continuing BS that many Public Sector DB Plans are in “fine” shape. Now, as to the rest of your above comment……..

First, I couldn’t agree more with your very negative comments about Donald Trump and Dick Cheney. God help us if Trump is elected ….. not that Clinton is a good alternative. But as I pointed out before, NONE of their misdeeds (or those of Private Sector companies & wealthy individuals you so despise) translates into the buyers of bonds CHEATING the taxpayers, as have Public Sector Unions/workers via their grossly excessive pensions having been BOUGHT from our taxpayer-betraying Elected Officials.

Continued discussion of this with you is pointless, as if I’m playing whack-a-mole ….. knock down one irrelevant response and another equally irrelevant response pops up.

September 16, 2016 at 2:27 am

Well, TL, not once have you responded to http://www.retirementheist.com, which totally blows up any claim you make about the private sector pension system… it is governed not by any government regulation, but by corrupt influence of the private sector over regulators.

And written by a Wall Street Journal reporter.

And you absolutely haven’t responded to the simple fact… many of the best DB systems in the country did stay mostly in public bonds, and assume an even lower return than the corporate bond rate…. blows up your false claims about DB system. Finally, you miss entirely the point that the transition of many public systems to risky stocks and other volatile securities was the result of lobbying *by the private financial sector itself*.

And still… your cronies moan about the US Social Security system and say its purchases of treasuries are a Ponzi scheme. Where do you stand on that? Not even US treasuries are conservative enough for you… because you just want DC plans at any cost, so your cronies can get the fees.

September 16, 2016 at 6:16 am

Quoting spension ……

“many of the best DB systems in the country did stay mostly in public bonds, and assume an even lower return than the corporate bond rate”

Identify them…very specifically

September 18, 2016 at 7:46 pm

I’ve identified them and provided links already.

Naturally there is Social Security itself… a combination of Pay-As-You-Go and investment exclusively in public US treasury bonds. Naturally, people like Tough Love howl and wail about investing in public US treasury bonds… calling it a Ponzi scheme.

The public system that is *even more* pay-as-you go… military pensions… not a peep from Tough Love or others about the incredible debt run up in that system, or how it fares with GASB, which is very badly. And you can retire in your 30’s with a military pension, far younger than the California systems allow. Never hear a peep from TL about that atrocious pension giveaway.

Again and again I whack your false moles down, and again and again you post false information about the US private sector retirement system…. we ended up with a pathetic private retirement system in the US because the captains of the private sector CHEAT the taxpayers (by dumping liability on the PBGT), just as the captains of the private sector have cheated their employees by funding their own grossly excessive pensions by lifting assets, and by having BOUGHT our taxpayer-betraying Elected Officials to short circuit effective regulation. It is documented in the Pulitzer-winning WSJ reporter’s book:

http://www.retirementheist.com

Never, never will TL respond to the facts of that book, because he wants to maintain the myth that only the public unions influence policy and pension benefits.

The public unions most certainly have influenced their pension system by donated to politicians and calling in the promises. Great article in the LA Times today on the bipartisan effort to pass SB 400 (bipartisan, Republicans had a big majority in favor).

The only group in the US that has *exceeded* the public unions’ influence has been the private sector. In fact the public unions learned their lessons in influence from the private sector… the private sector has donated to evade liability for the PGBT, workman’s comp, tobacco, environmental devastation, etc… for a century or more.

All sorts of malfeasance by the private sector is just fine with Tough Love. Because that is the America he loves. If an elderly school teacher like my California kindergarten teacher and my 6th grade teacher get a modest pension ($50,000 a year or so, after 40+ years of service in each case) he can’t stand it.

Not sure TL even has a kindergarten teacher in California who has a pension. Probably TL opposes all public education and probably wants repeal of every amendment to the constitution after the 12th.

That way he could just own slaves and not have to pay anything for their salaries, health care, or pensions!

September 19, 2016 at 2:09 am

Spension, To be honest with you, I have more than enough on my plate fighting the grossly excessive, unnecessary, unjust, unfair (to Taxpayers), and CLEARLY unaffordable State & Local DB Public Sector Plans to worry about Federal level promises …. while a questionable long–term solution,THEY do have a printing press.

I have also not disagreed that there are bad elements in the Private Sector pension world, although FAR FAR FAR FAR FAR fewer than in the Public Sector where the “bad elements” are near 100% of the actors.

None of that stuff ….. which you continually add to the discussion to distract the readers’ attention from the issue at hand (grossly excessive PUBLIC Sector Pension and their impact on State/City budgets) …. has, does now, or will EVER justify the gross excess in PUBLIC Sector DB Plans.

——————————-

And to repeat the UNANSWERED:

Quoting spension ……

“many of the best DB systems in the country did stay mostly in public bonds, and assume an even lower return than the corporate bond rate”

Many ? if measured in terms of Plan Liabilities or Plan Assets, how big is that “many” as a % of the total …….. perhaps 1/1000 of 1% ?

I’d love to look at a few of these Plans that ………”assume an even lower return than the corporate bond rate” …. for their overall investment returmn assumption. Personally, I doubt you can find more than I could count on one hand, from the thousands of Public Sector Plans, and if any do exist, they are likely tiny LONG-CLOSED significantly over-funded Plans consisting of ONLY retirees.

The readers are STILL WAITING for full and complete SPECIFIC identification of any such Plans ………….. and naming a State, doesn’t cut it.

————————————————–

And as to books, the readers would be FAR better advised to read Steven GreenHut’s ………… Plunder: How Public Employee Unions are Raiding Treasuries, Controlling Our Lives and Bankrupting the Nation.

September 19, 2016 at 9:46 pm

As you know TL, I’ve posted lists of the well-managed DB systems many times, including remaining private sector ones. Indeed the private sector ones won’t use public bond rates, they use corporate bond rates, which are often much higher…. nonetheless, the DB-haters only whomp on public sector DB plans as faulty for using an excess amortization rate.

And for the third or fourth time: Social Security, a DB plan, invests exclusively in Treasury Bonds, but nevertheless, the DB haters don’t give it credit for its conservative allocation… quite the contrary, they call it a “Ponzi Scheme”.

As for the private sector pension business, it is thick with fraud and corruption through influence by money over legislators and regulators:

http://www.retirementheist.com

Read it. Much more credible than you, that is for sure…

Not to mention just about every DCP in the country (with the exception of Vanguard, American Funds, and maybe Dimensional).

Yes, public DB benefits got way to high. Why? All the private sector investment banking lobbyists had a hand in it. George W Bush wanted Social Security to get partially out of Treasury Bonds, for example.

September 19, 2016 at 10:47 pm

Quoting …..

“As you know TL, I’ve posted lists of the well-managed DB systems many times,”

No, you make vague mentions of States/Cities with no specifics as the the exacts Plans. The readers are STILL waiting for 2 specific lists (per your claims in the above comments):

(1) Public Sector Plans in “fine” shape, “fine” meaning a 100% funding ratio when funded using the assumptions/methodology required by the US Goiv’t of PRIVATE Sector Plans, which translates into roughly a 150% funding ratio under the phony ultra-liberal valuation assumptions/methodology used by PUBLIC Sector Plans.

So please give the readers that list of (“fine” shape) Public Sector Plans reporting 150% funding ratios.

(2) That SPECIFIC list of “many” PUBLIC Sector DB Pension Plans that (for the overall investment return assumption) …………. “assume an even lower return than the corporate bond rate”.

You’re but a bag of hot air ….. and assuredly can provide neither.

—————————————–

And there you go AGAIN (repeating Private Sector misdeeds), attempting to divert the readers attention from the issue at hand …. the grossly excessive, unnecessary, unjust, unfair (to Taxpayers), and clearly unaffordable Public Sector DB pensions.

September 20, 2016 at 8:15 pm

And readers are waiting for you, TL, to post the specific, quantitative basis for your claim that the unjustness and unfairness of the pubic sector post-retirement costs exceeds that performed by the private sector and documented in, for examples:

http://www.retirementheist.com

In your world, the private sector is lily-white and never drains its employees pensions while buying off regulators who don’t enforce GASB and other regulation, and who never foist the remains on the PBGC, but in the real world, those happenings are frequent.

And you just call the carefully documented private sector malfeasance “hot air”.

Me… I say both sectors are roughly equal in malfeasance, but with the private sector being the winner by a nose or maybe a length.

Click to access statepensions.pdf

Enjoy reading about the systems in there… like the New Jersey Prison Officers Pension fund, 167.6% funded, or the North Carolina Registers of Deeds Pension fund, 192.1% funded, or the Maine Legislative Retirement Fund, 157.9% funded.

I’ve posted that link many times.

September 21, 2016 at 12:46 am

Spension,

As I expected,

YOU made claims that you cannot support. We’re STILL waiting for 2 SUBSTANTIVE lists !

I made NO claims about the Private Sector’s misdeeds and therefore have noting to justify.

——————————————-

P.S., I was aware of the fully-funded NJ Prison Officers Pension fund (POPF), and was hoping you would idiotically reference this as PROOF of your claim … of Public Sector Plans in “fine” shape.

Of NJ’s 700,000+ active and retire pension Pan participants, the NJ POPF plan you noted had EXACTLY ZERO actives and 135 retirees (as of 6/30/2012).

Similarly the North Carolina Registers of Deeds Pension fund is SO TINY, it represents 1/20 of 1% of the assets in all of NC’s Public Sector pension Plans.

Similarly, pasting from a Google search of the Maine Legislative Retirement Fund ………….. “The Legislative Program is funded at 157.9% as of June 30,2011, primarily because few legislators qualify for a retirement benefit under the terms of the program.”

This is your LIST and Proof of Public Sector Plans in “fine” shape. ?

—————————————————–

Really? You’re either a fool, or a charlatan

September 21, 2016 at 3:21 pm

TL “So please spension …….give us a list of Public Sector DB Plans with published funding ratios of 150% or greater.”

Check, did that, TL, you just can’t admit that I did. You are now dissembling and trying to fib your way out of the simple fact: I provide information, and YOU DON’T.

Oh, let’s also add to your embarassing behavior: name calling, like, “you’re either a fool, or a charlatan”.

You purposefully exaggerate my claims into “proof of Public Sector Plans in “fine” shape”. I’ve always said that there are many, many public sector plans that are in fine shape, but never, ever have I said or implied that every public sector DB plan is in fine shape.

I’ve been relentless in criticizing California’s public DB plans.

Huge long list in of terrific public DB plans in:

Click to access statepensions.pdf

I’ve been relentless in criticizing California’s public DB plans.

As to the private sector, you are the one who brings it up *all the time*:

TL says: “I made NO claims about the Private Sector’s misdeeds..”

Of course you don’t, because you worship the Private Sector like it is infallible God. You overlook the reason that DB plans disappeared from the Private Sector: private companies drained the DB pension funds and gave the proceeds to their executives, as carefully documented by the Wall Street Journal Pulitzer-Prize winning reporter in:

http://www.retirementheist.com

You are the one who constantly raises the issue that public sector post-retirement benefits should not exceed private sector benefits (well, not really, you believe that the executives of the private sector, particularly those private sector industries that survive on taxpayer subsidies, like healthcare and defense, should have golden-parachutes that exceed the post-retirement benefits of equivalent public sector executives like, say, Paul Volcker).

The current private sector DB benefits were slashed to very little by fraud and corruption in the private sector. Ergo, you are completely in favor of fraud and corruption, as long as it benefits your corrupt Gods, the private sector executives.

And you are in favor of the unbelievably corrupt DC industry, where essentially every DC provider except Vanguard, Dimensional, and American Funds has been been shown to corruptly guide their customers to super-high-fee investment products! In fact my experience in the DC industry (where I had an IRA that grew 3% in 15 years… all the rest was skimmed for 4% fees per year) is the whole reason I post here.

Thank goodness I found Vanguard. But anyone who argues for DC plans exclusively, like you, is in favor of corruption. See the case of Penn Specialty Chemical… the laws simply don’t protect DC plan subscribers at all. The company can take every penny back (including employee contributions) any time they please. Penn Specialty proves it.

So DC plans are just another vehicle for the private sector to steal everyone’s retirements and give them to TL’s friends, the executives, like TL’s friends the executives did with most of the private DB plans:

http://www.retirementheist.com

Oh..BTW, there are some good private sector DB plans out there still in operation… not every private sector company is corrupt. But TL will never mention them, because the existence of those plans contradicts his thesis that “All DB plans are bad”.

The fact is: DB plans, when managed well, are far superior to DC plans. Period.

September 21, 2016 at 5:37 pm

Quoting spension …..

“TL “So please spension …….give us a list of Public Sector DB Plans with published funding ratios of 150% or greater.” Check, did that, TL, you just can’t admit that I did. You are now dissembling and trying to fib your way out of the simple fact: I provide information, and YOU DON’T.”

What a farce of a response. My call for a list of Public Sector Plans REALLY in “fine” shape (i.e., those with a 150% funding ratio under the ultra-liberal Public Sector valuation methodology) arose from YOUR statement ………….

““DB plans got out of control in California, but all over the US there are perfectly fine DB plans.””

And you think identifying a few obsolete Plans with assets or liabilities less than 1/10,000 of 1% of those of all Public Sector Plans proves your claim?

Really?

And then you task it even further by stating ….

“You purposefully exaggerate my claims into “proof of Public Sector Plans in “fine” shape”. I’ve always said that there are many, many public sector plans that are in fine shape, but never, ever have I said or implied that every public sector DB plan is in fine shape.”

Where did I EVER say “every” ?

To repeat ….”you’re either a fool, or a charlatan” … or just ignorant.

September 21, 2016 at 6:00 pm

Spension, I should have included this in my above comment …..

Single-employer DB (but NOT multi-employer Union Plans*) Plans in the PRIVATE Sector are generally OK BECAUSE the promised benefits are generally reasonable (rarely more than 1/3 the TRUE value of PUBLIC Sector Plans), are offered by (or negotiated with) financially astute management that WILL NOT grant more than is affordable, and can for FUTURE service be reduced or ended completely …. and with extreme care because it’s the Company’s money at stake if something (i.e, lower than expected investment earnings, longer than expected life expectancy, etc.) goes wrong.

DB Plan cannot and do not belong in the PUBLIC Sector. The inability of universally self-interested Politicians to vastly over-promise (and AS A RESULT, under-fund) FAR exceeds the beneficial effects of the mortality-sharing nature of DB plans.

————————————-

* Multi-employer Plans, wherein the employer contribution is “negotiated” and completely unrelated to the contribution amount necessary to actually pay the promised benefits calls into question WHY such Plans are actually called DB Plans. They fail the most basic actuarial tenants of true DB Plans …. BY DESIGN.

The mess that many Multi-employer Plans are in today represents a HUGE failure of our Government in ever ALLOWING such Plan arrangements.

September 21, 2016 at 9:18 pm

Here we go again… the standard TL gutter-game name calling.

Because TL does not have the facts, or bother to look at the facts, he argues only from prejudice.

The scorecard is:

1)Long list of many public DB plans that are just fine (not just the 3 I mentioned in http://corporate.morningstar.com/us/documents/reports/statepensions.pdf)… TL ignores that list. And in fact he now says “DB Plan cannot and do not belong in the PUBLIC Sector. “. Ignoring BTW, one DB plan that is *solely* invested in public bonds, and is currently 350% funded… OASI… Chart E of https://www.ssa.gov/oact/trsum/ .

Projections do look bad, but, hey, that is because income above $118,500 pays absolutely 0 into that system. TL denies all of this.

2)Constant calls by TL for debasing public benefits down to the level of the private sector, where benefits were destroyed by years of corruption, fraud, dirty influence over politicians, and the foisting of problems onto the PBGC, s documented by Pulitzer-winning Wall Street Journal reporter in http://www.retirementheist.com . TL never addresses this issue.

3)Constant lauding of the DC sector, where worker’s savings have no protections from predatory behavior by the private sector, both through high fees and out-and-out grabs by the entities that oversee the DC plans… like Penn Specialty Chemical http://www.nytimes.com/2014/02/02/business/a-long-fight-to-get-what-was-theirs-in-a-401-k.html .

4)Incredibly rich private sector benefits, >$100 million, at the taxpayers’ expense (in industries that depend on taxpayer handouts, like Healthcare and Defense, Energy (grabbing taxpayer assets from resources on public lands))… http://moneymorning.com/2013/03/18/top-10-ceo-severance-packages/). Comparable payouts to public sector execs of similar talent, like Paul Volcker, are nothing like that level. But TL wants public moneys to go into $100 million private sector payouts.

September 21, 2016 at 11:13 pm

Responding to spension’s comment by point:

(1) clicking your link shows just a summary from Morningside WITHOUT any “LIST”, and says …..”To obtain a copy of the full report, please contact the municipal research team at MuniSupport@morningstar.com“.

Are you serious ? And I REALLY doubt that any such “list” would include more than a handful (if ANY) of SUBSTANTIVE SIZE Plans with funding ratios of at least 150% (indicative of being in “fine shape) when using the PUBLIC Sector’s ultra-liberal (i.e., phony) valuation methodology.

So WHAT list…. PROVIDE that list.

And more idiotic commentary, calling OASI 350% funded. No, ask ANY economist …. it’s really 0% funded. …. the hole in the bucket problem.

(2) When SOME bad dealings took place in the 1980s, that ceased decades ago when laws were enacted instituting a 50% excise tax on Private Pension Plan withdraws for anything but legitimate Plan purposes.

And YES, with EQUAL “Total Compensation” (pay + pensions + benefits) in comparable Public/Private Sector jobs being the APPROPRIATE (and FAIR) goal, unless there is demonstrably lower cash pay in the Public Sector worker’s job, there is ZERO (yes ZERO) justification for Taxpayers to contribute more towards Public Sector workers’ pensions & benefits than what they get from their employers. Public Sector workers are NOT “special” and deserving of greater compensation …. on the Taxpayers’ dime.

While some (no actually many …. including me) might agree that Safety workers (Police/Fire) are deserving of pensions “somewhat” greater than Private Sector workers in jobs with comparable risks and requiring similar education, experience, skills, and knowledge, I’d bet that MOST would (if asked) suggest pensions perhaps 25% (or perhaps even 50%) greater in value upon retirement than a Private Sector worker retiring at the SAME age, with the SAME pay, and the SAME years of service. But absolute NONE (ZERO, NADA) would suggest SAFETY worker pensions with a value 4 to 6 times greater …. as is ROUTINE today. Few Taxpayers understand the true magnitude of the financial ripoff in place RIGHT NOW.

(3) Employer-sponsored DC Plans have historically included higher than necessary fees, and too often do not include investment options (of comparable merit) with lower fees. This is now being addressed (via new laws and regulations) both with lower fees, more options, and the ramping up those subject to Fiduciary standards who MUST put the customer/participant’s interests before those of the investment advisor or Plan sponsor. \

As I have stated many times before, the involvement of self-interested Politicians in DB Pensions make such pensions an UNWORKABLE option for Public Sector pensions.

(4) Whatever you are talking about ….. I’m sure you threw it in to again attempt to distract the reader’s attention form the HUGH problem at hand …. the immediate need to address (i.e., materially REDUCE) the Grossly Excessive pension/benefit promises made to PUBLIC Sector workers throughout America.

Every day we delay doing such digs the financial hole we are in even deeper.

September 22, 2016 at 6:57 am

Definitely required reading …………..

http://spectator.org/suddenly-a-shifting-pension-paradigm/

September 22, 2016 at 4:40 pm

(1) One of the most serious assessments of public pensions in existence.. the Morningstar one… I’ve posted links to it many times… and you’ve never even read it, TL? Too hard to request it? Shows how truly ignorant you are. Quite a few fine public systems in that document. Your comments about computation of funded ratio are now totally ruined by everyone’s realization that you do no homework before you spout off. And yes, the OASI will face problems, because there is 0 contribution made for income above $118,500… a regressive system which you, of course, you support.

(2) + (4) post-retirement compensation is >$100 million at retirement for many leaders of the private sector, but not for comparable leaders of the public sector (like Paul Volcker). Totally blows up any comparison you make. As for lower-paid workers, the private sector redistributed their DB pensions to the top leaders as described in http://www.retirementheist.com, but we all now realize, you don’t do your homework and read that.

(3) As you say, DC plans are not ready for prime time. The many successful DB plans at least have had less fraud than the DC sector… the main DB problems have been overpromising of benefits, which of course has often been due to greed (in California, in particular). Other contributing factors… in other states (like Illinois) the legislature never made anything like the required contributions…. also, you totally neglect the fact that the private sector long ago lobbied for moving public pension funds out of safer bonds… there is also culpability in the private sector.

September 22, 2016 at 5:13 pm

quoting spension ….

“Quite a few fine public systems in that document.”

Really, in “fine” shape (with 150% reported funding ratios under the ultra-liberal, phony PUBLIC Sector reporting methodology) ?

Really ?

Then LIST THEM !

————————————————————

Quoting spension ….

“And yes, the OASI will face problems, because there is 0 contribution made for income above $118,500… a regressive system which you, of course, you support.”

No, SS will face problems because is has ZERO “real’ assets ….. assets it can sell (to someone OTHER than itself by raising taxes or cutting service to pay for it) to generate cash to pay it’s obligations.

Educate yourself.

—————————————————

Who care if Private Corporations are stupid enough to overcompensate their executives. That money comes from shareholders or the company’s customers who can choose to invest elsewhere or choose to shop elsewhere if that compensation makes the price of their products or service uncompetitive.

What alternatives do Taxpayers have when States/Cities VASTLY overcompensate their workers (primarily via their grossly excessive pensions & benefits) ? Can they shop elsewhere for Police or DPW services ?

—————————————————

Quoting spension ……

” The many successful DB plans at least have had less fraud than the DC sector”

Really? Are the Grossly Excessive PUBLIC Sector pensions now in place almost everywhere NOT the result of collusion between the Public Sector unions and our Elected Officials, with the former BUYING the favorable votes of the latter (on Pay, pensions, and benefits) with Union campaign contributions and election support?

While such actions may not meet the LEGAL threshold of fraud (because the Elected Officials that are a party to and benefiting from that fraud also make the laws determining what constitutes fraud) it is fraud no less. Such DB Plan FRAUD exceeds (as to the financial consequences inflicted upon Taxpayers) any DC fraud by orders of magnitude.

September 22, 2016 at 5:57 pm

(1) I’ve provided you a list, you just won’t go and get it, due to your lassitude. The OASI trust fund owns Treasury Bonds, you just don’t educate yourself about it. And there is no contribution for income above $118,500, or for carried interest (who you and other investment professionals evade contributions), etc.

(2) I don’t think taxpayer funds through Medicare, Defense, NIH, Medicaid should subsidize vast private sector pensions, but you do.

(3) DC plans… the companies that oversee them can just liquidate them.. as Penn Specialty Chemical has proven. Not ready for prime time. Meanwhile, my 90+ year old elementary school teachers get their very modest DB pensions regularly. Obviously a much better deal than the corrupt and fraud-ridden DC system.

September 23, 2016 at 1:15 am

spension,

(1) Well, I’m trying to get that mysterious “list” that you refuse to post directly. Might it be that there ARE NO substantive size Public Sector Plans on it that report funding ratios of 150% or greater (meaning in “fine” shape)? I’m guessing that that’s the case. We’ll see.

Yes OASI “owns” Treasury Bonds. If they held say Apple stock. they could sell it, and the cash would COME FROM the BUYER of that stock. When OASI needs to “sell” it’s Treasury Bonds (to be able to make SS payments) it can ONLY sell them back to the US Treasury. And where will the US Treasury get the funds to “pay” for them (i.e., buy them back)? By either raising taxes or issuing new debt (likely the latter until the USA is so strung-out debt-wise that we will no longer to be able to find any buyers of newly issued debt). Bottom line …… the OASI “assets” are effectively worth ZERO in being able to actually PAY SS benefits. Like I stated earlier ….educate yourself.