CalPERS took another step last week toward a gradual long-term rate hike, a move to lower the risk of big investment losses as the maturing pension system enters a new era.

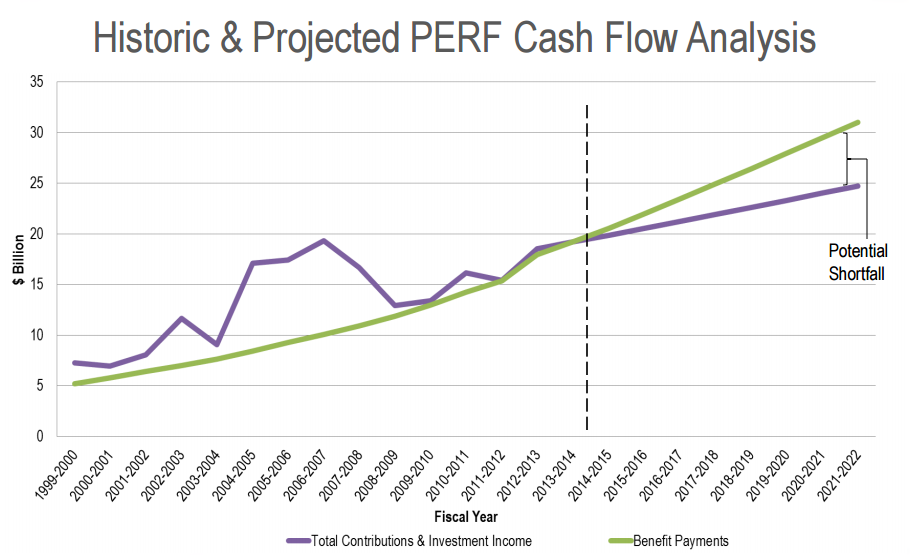

Retirees are beginning to outnumber active workers. Pension payments to retirees are no longer covered by employer-employee contributions and investment income. Now “negative cash flow” forces the sale of some investments to cover annual pension costs.

The new need to routinely sell some investments (see two charts at bottom) is one of the reasons the California Public Employees Retirement System is expected to have even more difficulty recovering from investment losses in the future.

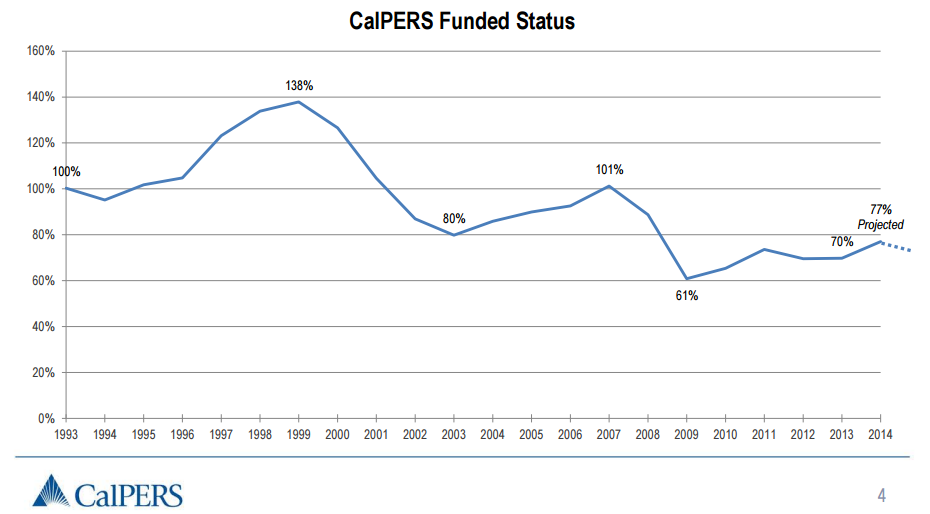

After a loss of $100 billion in the recent recession, the CalPERS funding level dropped from 100 percent in 2007 to 61 percent in 2009. It has not recovered, despite a major bull market in which the S&P 500 index of large stocks tripled.

“Even with the dramatic returns we have seen over the past six years, because the demographics of plans in general have changed and plans are now by and large cash-flow negative, it’s been very challenging to dig out of that hole,” Andrew Junkin, a Wilshire consultant, told the CalPERS board last week.

The funding level of CalPERS in fiscal 2013-14 was 77 percent of the projected assets needed to pay pensions promised in the future. But investment returns last fiscal year were below the forecast, 7.5 percent, causing the funding level to fall again.

“With the estimated 2014-15 investment returns of 2.4 percent, that funded status is expected to drop to a range of 73 to 75 percent,” said Cheryl Eason, the CalPERS chief financial officer.

In a loss equaling the state general fund budget at the time, the CalPERS investment fund dropped from about $260 billion in the fall of 2007 to $160 billion in March 2009, before climbing a little above $300 billion early this month.

CalPERS won’t soon run out of money. Its main fund paid $18 billion last year to 594,842 persons, up from $11 billion to 462,370 in 2007. Employers contributed $8.8 billion and members $3.8 billion, up from $7.2 billion and $3.5 billion in 2007.

Critics say the CalPERS earnings forecast, an average of 7.5 percent a year, is too optimistic and conceals an even larger funding gap. The board is working on a “risk mitigation” strategy that could slowly lower the forecast to 6.5 percent over 20 years.

When the earnings forecast goes down, some of the pension fund can be shifted to less risky bond-like investments. The yield is likely to be lower, but so is the chance of big losses in an economic downturn.

A lower earnings forecast also means that contribution rates are likely to go up, offsetting the lower earnings assumed in the future. That’s what happened when the CalPERS board in 2012 lowered the earnings forecast from 7.75 percent to 7.5 percent.

The CalPERS chief actuary, Alan Milligan, recommended lowering the forecast to 7.25 percent to provide a cushion or “margin for adverse deviation” as in the past. The board phased in the rate increase over two years to ease the impact on employer budgets.

Two more rate increases followed: a change in actuarial method in 2013 and a projection of longer life spans last year. Now a total employer rate increase averaging roughly 50 percent will be phased in by the end of the decade.

Under the proposed “risk mitigation” strategy CalPERS would consider lowering the earnings forecast in good years when the annual investment return is well above the current earnings target of 7.5 percent.

For example, a return of 11.5 percent might cause the board to consider lowering the earnings forecast by 0.05 percent. After a larger return of 17.5 percent, the board might consider lowering the earnings forecast 0.15 percent.

Brown aides urged the CalPERS board to consider using its existing policy to speed up the lowering of the earnings forecast. The rate increase resulting from a lower forecast would be phased in over five years and amortized or paid off over 20 years.

“If the current investment assumption of 7.5 percent is an unacceptable risk today — by the nature of this conversation it seems everyone is more or less in agreement that it is too high — the board should consider lowering it sooner rather than later,” Eric Stern of Brown’s finance department told the board.

Richard Gillihan, a CalPERS board member and director of Brown’s human resources department, said he agreed with the administration position and asked for an explanation of why the existing policy for lowering the forecast is not being used.

“It just seems like it’s too easy to pat ourselves on the back and say, ‘We came up with this plan,’ and then we are not doing anything with it for a few years and then a future board might change it.”

The CalPERS chief actuary, Milligan, said the proposed strategy balances the need to lower investment risk with concern about the impact on the budgets of 3,000 local governments, some in better financial condition than others.

“I would be concerned about the amount of strain we would put on some of our public agency (local government) employers,” Milligan said of dropping the earnings forecast too quickly. “Apparently, it’s not such a concern for the state.”

In the past, CalPERS rate increases only hit employers. But now many employees are included. A pension reform calls for employees to pay half of the pension “normal cost,” which excludes the debt or “unfunded liability” from previous years.

Milligan said the 50-50 split of the normal cost is required for local government, CSU, judicial and legislative employees. But the reform did not require a normal cost split for most state workers. Their rate is set by legislation resulting from bargaining.

In an example, over two or three decades miscellaneous employee rates could increase by a half to 1½ percent of pay and safety rates by 1½ to 3½ percent of pay. The timing would vary among plans, depending on the reform and demographics.

The CalPERS staff recommended a “blended” path with check points, perhaps every four years, when a lower earnings forecast would be considered. Rate increases would be more certain and predictable.

Union representatives argued for a “flexible” path when a lower earnings forecast would only be considered after a year with great investment returns. Rate increases would not be on “autopilot” and would be less likely to happen after a year of bad returns.

A spokeswoman for the League of California Cities told the board cities surveyed split on blended vs. flexible but were in favor of taking action to lower investment risk. A spokesman for special districts said they favored a blended plan.

The CalPERS board, in an 8-to-4 straw vote, directed the staff to prepare a flexible plan for a first reading in October. The final vote on a risk mitigation strategy may be in November.

Reporter Ed Mendel covered the Capitol in Sacramento for nearly three decades, most recently for the San Diego Union-Tribune. More stories are at Calpensions.com. Posted 24 Aug 15

August 24, 2015 at 2:16 pm

Interesting: Raise rates, cut the discount rate, cut services, etc; everything except cut the benefit rate. Ho Hum.

August 24, 2015 at 3:21 pm

“Retirees are beginning to outnumber active workers.”

Which means that California government workers get more than one year in retirement for each year they work. One has to ask the question whether or not that is fair to everyone else. The U.S. certainly couldn’t have that ratio economy-wide. You only get that many years of permanent vacation at someone else’s expense.

August 25, 2015 at 3:56 pm

@John Moore “everything except cut the benefit rate.”

That’s exactly what Brown’s PEPRA did. Raised retirement age, put a hard ceiling on pensionable income, increased employee contributions, prohibits spiking. With time the number of people under the old rules will slowly decline and the pension systems will get better.

August 25, 2015 at 5:37 pm

Pension payments are no longer being paid out of investment income?? Mr. Mendel, give yourself 50 lashes and come back with a direct quote from whoever on the CalPERS Board or staff made such a statement!

August 25, 2015 at 6:44 pm

larrylittlefield,

Which means?

Most state or city employees don’t work 40 years for the state, then retire. If SeeSaw is still reading, I hope she can get “more than one year in retirement for each year” she worked, but in typical circumstances, the position would have been filled by three different people, each serially working five to fifteen years.

SeeSaw = one career, one pension

Typical position = three partial careers, three partial pensions.

So, yes. There will be more retirees than workers. Nothing nefarious happening here.

If I manage to get more years in retirement than I worked, I will live to be just over 99. Don’t hold your breath. Or do, whatever floats your boat.

August 25, 2015 at 8:39 pm

CalPERSon,

In case your response didn’t make it perfectly clear to John Moore, PEPRA did also “cut the benefit rate.” ( Ho Hum.)

Safety from 3%@50 went to 2%@50 and miscellaneous went from (various, mine was 2%@55) to 2%@62, a lower formula than before SB400.

A smaller pension, and, as you said, at a higher cost to the employee. I would call that significant.

In the CalPERS policymaker report, the example is a worker with a starting salary of $46,000 who retires after 20 years at age 62. The pension for the pre-reform or “classic” worker is $2,140 a month, compared to $1,705 for the new hire — $435 less.

Although I suspect John Moore knew this already.

August 25, 2015 at 11:47 pm

@SMD – My former job, one position with multiple duties for 40 years, does not even exist any more. Those duties are dispersed separately among several part-timers who are not covered by CalPERS. Then there is the department with employees in the “hybrid” category–salary with benefits and no CalPERS. The complainers have no idea what they are talking about!

August 26, 2015 at 2:46 am

Remember Hawkeye, from “Mash”? When he got caught, he said “Sheesh, peek into ONE shower, and you’re labeled for life!”

If some public workers are able to spike their pension with last year OT, they’re probably all doing it. “Some” $100,000 pensions means that’s what most are getting. Public workers “can” retire at 50 is the same as “public workers retire 10 to 15 years younger than the private sector.”

See that example two posts up about the worker retiring with a $46,000 salary? It’s a copy/paste from a Calpensions article (May 5, 2014). I pasted it some time ago in response to someone who claimed PEPRA didn’t do anything. I immediately got a response calling “BS” on my post because “NO California state worker makes only $46,000 a year.”

Labeled for life.

And I just realized, John Moore probably meant that no CURRENT worker got a reduced formula for future service. Apparently that is the brass ring of pension “reform”.

August 26, 2015 at 9:51 pm

“And I just realized, John Moore probably meant that no CURRENT worker got a reduced formula for future service. Apparently that is the brass ring of pension ‘reform’.”

With a funding shortfall of tens of billions of dollars, yes, a reduced formula for future service of current workers is a rational goal. Why take the sacrifice solely out of the hides of citizens paying taxes for reduced services and more-recently hired employees for insane pension enhancements from the SB400 era?

August 27, 2015 at 12:16 am

@BC–Because you can’t change what is already contracted and vested. And FYI: All of the public employees are among the same citizens whose hides will be sacrificed. This is the greatest country in the world! So–let’s keep it that way. Pay your damn taxes!!!

August 27, 2015 at 7:17 pm

B Chillin’

“In the CalPERS policymaker report, the example is a worker with a starting salary of $46,000 who retires after 20 years at age 62. The pension for the pre-reform or “classic” worker is $2,140 a month, compared to $1,705 for the new hire — $435 less.”

$46,000, that’s about what a CalTRANS maintenance worker earns.

Pre-PEPRA, He would contribute 5% of salary and receive $2,140 a month. Holding inflation constant, that would be total contributions of $46,000.

Post-PEPRA, He will contribute 10% of salary, or $92,000. Technically, his “formula” hasn’t changed, but in reality, for each dollar contributed, he will receive HALF the pension.

Of course, it is worse for the new worker, because he contributes the same, and will receive even less.