CalPERS is considering small increases in employer and employee rates over decades to reduce the risk of big investment losses, a policy that also would lower an earnings forecast critics say is too optimistic.

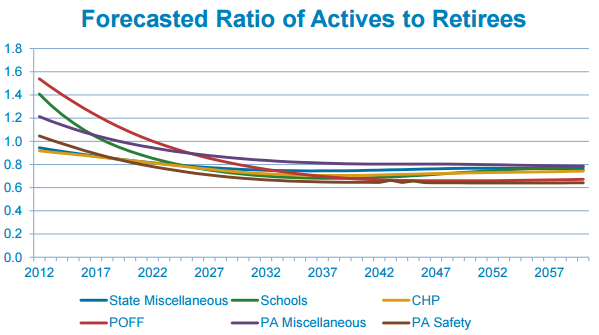

The proposal is a response to the “maturing” of a CalPERS system that soon will have more retirees than active workers. From two active workers for each retiree in 2002, the ratio fell to 1.45 to one by 2012 and is expected to be 0.8 to 0.6 to one in the next decades.

As a result, investment losses will trigger bigger California Public Employees Retirement System employer rate increases. It’s a kind of “leveraging” effect as the investment fund becomes increasingly larger than the payroll on which rates are based.

The risk of big investment losses is a threat for other reasons. Funding could drop below 50 percent of the projected assets needed to pay future pensions — a fuzzy red line said to make returning to full funding nearly impossible, requiring onerous rates and unlikely investment returns.

“The concern that I have is that the volatility we have built into the funding system is such that it may cause such severe strain on the employers that they may not be able to make the contributions,” Alan Milligan, CalPERS chief actuary, told a board workshop on risk last month.

The new risk reduction policy is advocated by top staff who took office after CalPERS had huge investment losses in 2008: Milligan, CEO Anne Stausboll, Chief Investment Officer Ted Eliopoulos, and Chief Financial Officer Cheryl Eason.

It’s a sea change from the late 1990s when CalPERS cut employer rates to near zero for two years and sponsored a large retroactive pension increase for state workers, setting a benchmark for local police and firefighter pensions critics say is unsustainable.

Awash in earnings from a booming stock market and a funding level that briefly reached about 135 percent, CalPERS told the Legislature that, due to “superior” investment returns, SB 400 in 1999 would not increase state rates for “at least a decade.”

A 17-page CalPERS brochure on SB400 distributed to the Legislature quoted former CalPERS President William Crist: “This is a special opportunity to restore equity among CalPERS members without it costing a dime of additional taxpayer money.”

But after a market plunge, soaring CalPERS state rates were cited by former Gov. Arnold Schwarzenegger in 2005 as he briefly backed a proposal to switch new state and local government hires from pensions to 401(k)-style individual investment plans.

In 2007 CalPERS was 100 percent funded with investments valued at $260 billion. Then a deep recession and stock market crash in 2008 dropped investments to $160 billion with a funding level of about 60 percent.

Now after an historic bull market, and a rate increase of roughly 50 percent that is still being phased in, the CalPERS investment fund was valued at $303 billion last week with a funding level last June estimated at 77 percent.

In each of the last three years, CalPERS made changes that raised employer rates: the earnings forecast dropped from 7.75 percent to 7.5 percent in March 2012, new actuarial methods in April 2013, and new longevity projections in February last year.

A staff report on risk last November said employer contribution rates for many CalPERS plans are at record highs, exceeding 30 percent of payroll for more than 100 miscellaneous plans and more than 40 percent of pay for 150 police and firefighter plans.

“Employers are reporting that these contribution levels are putting significant strain on their budgets and limiting their ability to provide services to the people in their jurisdictions,” said the report.

The proposal to reduce the risk of investment losses would gradually shift CalPERS to a less “volatile” mix of investments, narrowing up-and-down market swings but also lowering expected earnings.

A gradual increase in employer and employee contribution rates will be needed to offset the lower yield expected from a more conservative investment mix that reduces the risk of a big loss.

CalPERS can only raise employer rates. Employee rates would go up because Gov. Brown’s pension reform requires an equal employer-employee split of the pension normal cost, which excludes debt from previous years.

The risk reduction proposal is a broad concept lacking details that would be added by the CalPERS board. But some samples based on 5,000 simulations of 50-year projections (see below) show small rate increases over decades.

A key step would be slowly lowering the forecast of investment earnings expected to be available to pay or “discount” future pension debt. The current CalPERS earnings forecast or discount rate is 7.5 percent a year.

Critics say the earnings forecast is too optimistic and conceals massive pension debt. Corporate pensions had a discount rate of 4 percent last year. Unlike government employers, corporations can go out of business, so their pensions operate under tighter rules.

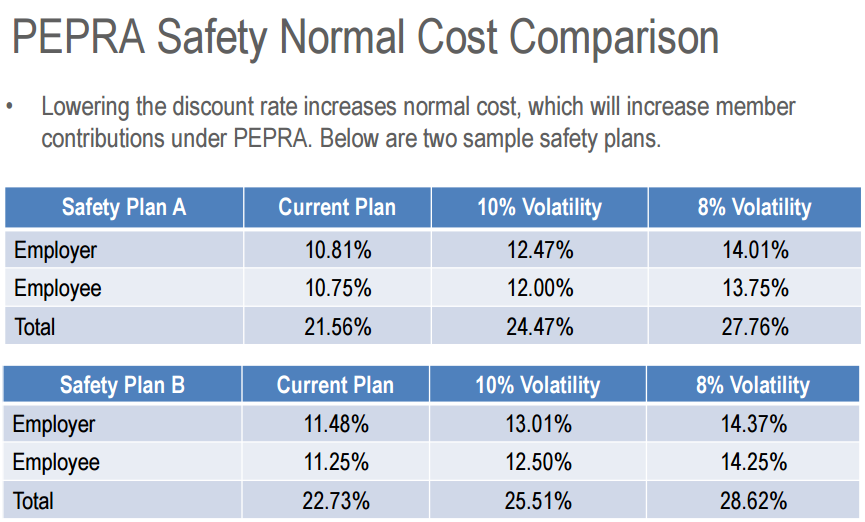

The CalPERS proposal has samples of reduced risk and investment volatility that would lower the discount rate to 7 percent or 6.5 percent. In one of the samples, getting to an investment volatility with a discount rate of 6.5 percent takes more than 20 years.

An issue before the CalPERS board last month was whether small cuts in the discount rate would be “flexible,” occurring only in good investment years, or “blended” with a small scheduled cut perhaps every four years.

Two board members said they were concerned about the negative “optics” of a lower discount rate that would increase the pension debt or “unfunded liability.” Theresa Taylor said pension opponents would have more to “latch on to.”

Stausboll said the positive message would be that CalPERS is addressing the discount rate, “the thing I think we get most of the criticism for,” and has a clear plan for “ensuring sustainability” of the pension system.

Several board members said they preferred the blended plan. Its certainty also was favorably mentioned by representatives of the largest state worker union, SEIU, and a statewide firefighter association, who said their groups had not taken a position on the issue.

A decision on the method of lowering the discount rate was delayed to hear from employers and employees. A stakeholder panel has been scheduled Aug. 19, and two employer webinars are scheduled this week.

As part of its risk reduction, CalPERS is developing a “message and communication” plan to show employers that, if they have the means, making additional pension contributions to reduce their unfunded liability makes good business sense.

CalPERS also is getting a legal analysis of offering employers, who currently have no choice of investment mix, the “ability to choose from one or two additional asset allocations” to select their own level of risk.

Reporter Ed Mendel covered the Capitol in Sacramento for nearly three decades, most recently for the San Diego Union-Tribune. More stories are at Calpensions.com. Posted 1 Jun 15

June 1, 2015 at 5:24 pm

Reblogged this on Transparent California and commented:

CalPERS recognizing their discount rate is inappropriately high; yet political pressure is used as a counter argument against adopting a fiscally sound rate!

June 2, 2015 at 12:57 pm

“The proposal is a response to the “maturing” of a CalPERS system that soon will have more retirees than active workers.”

When the system is mature, the ratio of years worked to years retired for an individual under benefit levels is reflected in the total number working and retired.

This means that in California, public employees are paid to be retired for more years than they are required to work.

The same is true elsewhere. Is that really fair? Is that really retirement? Were not slaveowners just people who got to be retired from day one? At some point it isn’t retirement anymore.

June 2, 2015 at 9:26 pm

CalPERS currently has approximately 1.6 million members, and approximately 500,000 retirees. How are those numbers going to transpose to the retiree group overtaking the active group–soon? The system is over 80 years old now–when will it be “mature”?

June 3, 2015 at 10:42 am

For all pension plans in California, the ratio of active workers to beneficiaries was 2.22 in 1992, 2.05 in 2002, and 1.48 in 2012, according to Census Bureau data.

Unit recently, California was a rapid population growth state. You had areas that had been rural, with relatively few public employees in the past, and thus few retired public employees in the present. But were now urban/suburban, with lots of taxpayers/current public employees.

That kind of growth allows the sleazy, apparently everyone with regard to public employee pensions, to cover up underfunding.

But then the larger number of public employees associated with that larger population retires. When population growth comes to a near halt for 20 or 30 years, both the number of current employees and retired employees reflect the same population. So the ratio of current to retired equals the years worked to years retired under the benefit level and longevity.

But it gets worse. The retroactive pension increases and underfunding means public services are being gutted. That means fewer active employees providing fewer services.