A California plan to give private-sector workers a state-run retirement savings plan is nearing $1 million in contributions, the goal set to pay for a market analysis to help design the program.

Although the California plan is still in the formative stage, last week the Illinois legislature approved a plan based on the California model, even using the same name, “Secure Choice.”

Legislation for similar programs named “Secure Choice” has been introduced in three other states: Maryland, Minnesota and Ohio. A variety of plans to aid workers without retirement plans has been introduced in 17 state legislatures.

Half of private-sector workers have no employer retirement plan beyond Social Security and may face a bleak financial future. Baby Boom retirements, dwindling private pensions and 401(k) investment losses during the recession are heating up the issue.

President Obama issued an executive order last January creating “MyRA,” a paycheck-deduction bond program. The U.S. Treasury department, reportedly preparing to begin the plan with a number of large employers, declined to comment last week.

Sen. Marco Rubio of Florida, a potential Republican candidate for president, advocated in May that the federal Thrift Savings Plan be opened to all Americans. The plan for civil servants and the military has several stock and bond investment options.

In California, Senate President Pro Tempore Kevin de Leon, D-Los Angeles, sworn in as the new Senate leader in October, tried for four years before obtaining legislation two years ago for the Secure Choice Retirement Savings Program.

Employees of firms with five or more workers that provide no retirement plan would be given the option of an automatic deduction from their paycheck, probably around 3 percent, that goes into a tax-deferred savings plan.

Saving is believed to be more likely with a deduction that removes the decision from daily spending pressure. Whether the plan guarantees a minimum return or seeks riskier higher returns is yet to be determined, but insurance would prevent losses.

The “automatic IRA” (SB 1234 in 2012) got little Republican support and was opposed by insurance, financial planner, employer and taxpayer groups. Among their concerns: competition, paperwork, state liability and doubt about the need for the plan.

The legislation created a nine-member board to oversee administration of the plan through the state treasurer’s office and also imposed tight controls. A board plan for the program developed after the market analysis must go to the Legislature for approval.

Employers and the state can have no liability for the plan. Approval must be obtained for an IRS tax deferral and an exemption from federal (ERISA) labor benefit rules. And the retirement savings plan must be self-funded.

Now a drive to raise $1 million for the market analysis is nearly complete. A $500,000 matching grant is coming from the Laura and John Arnold Foundation, financed by a Texas hedge fund billionaire vilified by labor for backing pension reform.

SEIU state labor council, California Teachers Association and Ford Foundation are each contributing $100,000; AARP $60,000; California Endowment and state Sen. Ted Lieu each $50,000; Steve Westly $1,000 and “not yet identified” $39,000.

The program staff is expected to recommend the hiring of a law firm, K&L Gates, at a board meeting Dec. 18. Proposals to do the marketing analysis are due early next month, and the two finalists may be interviewed by the board Jan. 26.

The marketing analysis is expected to be based on a combination of existing data and a sampling of eligible employers and employees. When delivered to the board, the study will include feasibility and program design.

“That will start the process of the board doing the heavy lifting of coming up with what recommendations they are going to make to the Legislature,” said Grant Boyken, Secure Choice acting executive director.

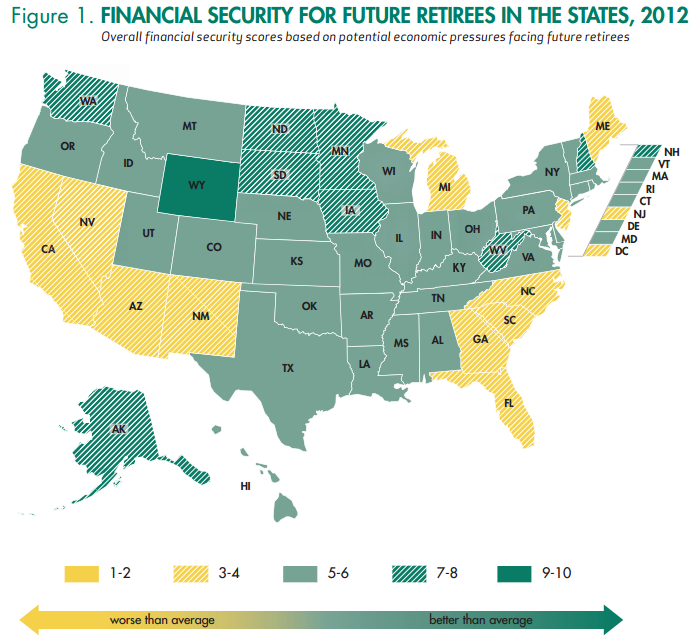

California ranks at the bottom among the 50 states in a “Financial Security Scorecard” for future retirees issued last March by the National Institute on Retirement Security.

The scorecard uses eight measures of three key financial security factors: anticipated income, major costs such as housing and health care, and labor market conditions for older workers.

On a scale of 1 to 10, California had an overall score of 3, tied at the bottom with South Carolina and Florida in 2012. In the data for 2000, California also had a score of 3 and was tied at the bottom with Mississippi, which moved up to score 5 in 2012.

In the eight measurements used for the score, California ranked 44 among the states for the share of private-sector workers in an employer retirement plan, 40.21 percent. Ranked 50 was Florida, 33.97 percent. Iowa ranked first, 54.08 percent.

In average defined contribution [401(k)-style individual investments] retirement account balances, California ranked 45 among the states, $23,381. Ranked 50 was South Carolina, $20,630. Wisconsin ranked first, $45,641.

For De Leon, the statistics have a personal meaning. He told National Public Radio last year that the inspiration for his automatic IRA bill is his aunt, Francisca, who is 74.

“She’s my second mother. She’s the woman who made me dinner and breakfast, and she’s still a housekeeper in one of the wealthiest enclaves in America,” said de Leon, who grew up in San Diego.

“I send her a check on a monthly basis, and she receives her Social Security check. But it’s simply not enough for her to pay the rent, to put the food on the table, to pay for her medication.”

The first version of de Leon’s automatic IRA bill in 2008 would have directed the California Public Employees Retirement System to offer the savings plan to private-sector workers who have no employer retirement plan.

In debates over pension reform, particularly switching to 401(k)-style plans, unions and other public pension supporters sometimes argue that the solution is retirement security for everyone, not taking it away from those who have it.

One of the 11 points in “Pension Beliefs” adopted by the CalPERS board last May: “Inadequate financial preparation for retirement is a growing national concern; therefore, all employees should have effective means to pursue retirement security.”

Another belief: “As a leader, CalPERS should advocate for retirement security for America’s workers and for the value of defined benefit (pension) plans.”

CalPERS had no position on the final version of de Leon’s bill. But if the Secure Choice plan is found to be workable and approved by the Legislature, would CalPERS become an advocate and administrator for the program?

“As you point out, retirement security is important to us and one of our fundamental beliefs,” Brad Pacheco, CalPERS spokesman, said via e-mail. “We have and look forward to continuing to provide technical assistance and expertise as the plan advances. That being said, it’s too early in the process to be more definitive until more details about the plan and feasibility are available.”

Reporter Ed Mendel covered the Capitol in Sacramento for nearly three decades, most recently for the San Diego Union-Tribune. More stories are at Calpensions.com. Posted 8 Dec 14

December 8, 2014 at 4:52 pm

Unless pensions are retroactively awarded to private sector employees with retirement at 55, those pensions are absolutely guaranteed, and public employee have to pay taxes to fund them, then it is nothing more than a fraud.

December 8, 2014 at 11:06 pm

Larry, there is no way private sector employees will ever receive pensions that even come close to what public employee unions currently receive, and retroactive increases aren’t even a consideration in this discussion. From this article:

“The legislation created a nine-member board to oversee administration of the plan through the state treasurer’s office and also imposed tight controls … Employers and the state can have no liability for the plan.”

That is much different from the CalPERS plans which emphasize that Employers and the state (TAXPAYERS), at least in the view of CalPERS, have guaranteed the pension payments of CalPERS members, for as long as they, or their spouse, live. And that includes COLA’s.

This plan is nothing more than a Red Herring. Pension Reform needs to work toward incorporating the same constraints which will be bestowed upon the private sector into the Public Sector/CalPERS pension plans, under this paln: “Employers and the state can have no liability for the plan.”

Afterall, what’s good for the Goose is good for the Gander.

I can’t believe the arrogance of these people. Instead of reforming a very Corrupt CalPERS Pension Plan, first … you’d think they’d clean up their own act before providing a very weak promise. CalPERS, the Public Employee Unions, and their paid for politicians have no shame.

Again, from the article: “Employers and the state can have no liability for the plan.” – Why?

– Again, Why? Of course that above phrase excludes anything resembling the current California Pension Plans, which taxpayers owe hundreds of billions of dollars, from ever becoming the same ridiculously generous plan enjoyed by Public Employee Unions/CalPERS members. That tells me there is no “equitable” plan and there is no reason to abandon pension reform efforts. In fact, based on this Red Herring, Pension Reform efforts should be pursued with great vigor.

CalPERS & the Public Employee Unions have conspired to fleece the TAXPAYERS and they’re continuing to find new avenues to confuse the real issue: CalPERS PENSIONS are way to genourous, the cost to taxpayers are unfair, and CalPERS is CORRUPT as hell.

December 9, 2014 at 12:37 am

Captain, You’re correct when you stated that this is a way confuse the real issue…..a Public Relations ploy attributable to those who oppose pension reform.

And at least some of those who wind up with these State-sponsored Private Sector Plans (not materially different than many other avenues for the Private Sector to invest) will be hoodwinked into believing that protecting the PUBLIC Sector Plans will also protect THEIR new Plans …… ridiculous.

December 9, 2014 at 4:57 am

Sarcasm, bitterness, AND paranoia.

How ironic.

December 9, 2014 at 7:25 am

The public sector and public pension reform are for another article, TL. The proposed plan for the private sector was put forth by Senator DeLeon and has nothing to do with public pensions. I wish this program for the private-sector well–why don’t you do the same.

December 9, 2014 at 12:18 pm

Look at the title of the blog. He can comment on public pensions whenever he likes. Respect the right to free speech of others. It is covered in the 1st amendment.

December 9, 2014 at 3:09 pm

Because the motivation is “see, you have pensions, we have pensions, we’re all equal.”

Not so.

What would have been fair to say is people took jobs and chose careers on the assumption that they would get the pensions they had been promised. Would have been fair to say if there hadn’t been all those underfunded, retroactive increases at a time when most people — those forced to pay for them — were getting poorer.

Everyone wants to avoid tallying up who benefited from doing what in the past. We need a Truth and Reconciliation Commission.

December 9, 2014 at 4:59 pm

BS! I took a part-time job that payed less than $2 hr. There was no SS and no pension and I was looking for only one thing–food on the table! Things worked out for me, decades later, and I now have a pension that affords me funding to pay for the humongous medical insurance premiums that my spouse and I are saddled with. I’m a taxpayer myself. You and your cohorts are a bunch of whiners–I hope you have plenty of cheese in your fridge, because you need it!

December 9, 2014 at 6:30 pm

LL, the retroactive increases were funded at the time they were passed. Furthermore, enacting formula-enhancements retroactively was standard practice by the CA Legislature since the first DB pension was founded in CA, 100 years ago. The pensions became unfunded when the private sector, ie, Wall Street caused the biggest, world-wide financial collapse in our own lifetimes, since the great depression. It was greed on their parts, absolutely.

December 9, 2014 at 8:59 pm

Captain said: “Larry, there is no way private sector employees will ever receive pensions that even come close to what public employee unions currently receive”

Here is a list of 21 private sector employees in the US who got over $100 million each in post-employment payouts:

Click to access GMIRatings_GoldenParachutes_012012.pdf

Oh, I know, you are talking about:

1)Rank and file employees

2)California pensions (other states and nations give far less)

Yes, I’d agree with that, but it is also true that the private sector DB systems were trashed by the same executives who pull in $100 million per. By a Wall Street Journal reporter…

http://www.retirementheist.com

But the fact is, Captain, you support fraud by the private sector because you feel they deserve $100 million payouts per person.

My opinion is fraud is bad whether in the private sector of the public sector.

And I’m the only one on these boards who suggests the one truly practical mechanism to reduce California public pension payouts… the State of California should do sovereign default and reorganize its debts, including pension debt and bond debt.

Captain, you, and Tough Love don’t really want to solve any problems, you want to use the too-high California DB plans as a cudgel to whack the US public sector.

December 10, 2014 at 1:29 am

“LL, the retroactive increases were funded at the time they were passed.” SeeSaw, that’s a deceptive way to mention the temporarily decent funding ratios of the late ’90s. Real financial professionals would have mentioned that the ratios would most likely fall under 100% once an average-sized market correction took place, and therefore retroactive DB increases should not be attempted without the public agencies being charged a percentage increase akin to the percentage increase of the sweetened benefits. Instead the corrupt CalPERS “professionals” refused to inform the politicians of the long-term costs and potential (now actual) risk of massive funding shortfalls.

“Furthermore, enacting formula-enhancements retroactively was standard practice by the CA Legislature since the first DB pension was founded in CA, 100 years ago.” Which only tells us that the Golden State has had irresponsible politicians for a long time. Anybody familiar with Californian history knew that to be true!

December 10, 2014 at 2:42 am

Essentially, what is said, I got mine and will steal yours

too. It is legal and I don t c.are what you think. I only care about people who agree with me. Pity the spouse.

December 10, 2014 at 3:25 am

Quoting spension … “But the fact is, Captain, you support fraud by the private sector because you feel they deserve $100 million payouts per person.”

In another comment I called you a fool, an idiot, or a charlatan.

Given the above comment, … “idiot” fits far better than the others.

December 10, 2014 at 3:38 am

spension …. The article linked below is a great example of why Public Sector DB pensions (and there BUILT-ON ability to rip-off the Taxpayers) should end. ALL of them should be switched to DC Plans, and not just for NEW workers, but for the FUTURE Service of all CURRENT workers.

http://www.reviewjournal.com/columns-blogs/glenn-cook/sounding-alarm-pension-reform

This would never happen under a DC Plan.

December 10, 2014 at 6:05 am

Captain said: “Larry, there is no way private sector employees will ever receive pensions that even come close to what public employee unions currently receive”

Spension, you don’t need a list of million dollar plus CEOs. There are thousands of mid level employees across the country who make $100,000 plus in wages, plus benefits and bonuses. They are often more than capable of self funding a retirement as good or better than most public pensions, and still have more net pay than most public employees. The information is out there. It’s just not as accessible as public compensation.

December 10, 2014 at 6:34 am

I pity you too, Stuart so we are even.

December 10, 2014 at 6:38 am

I have lived in CA for over 50 years, BC, through both good and bad and I am still here and love my state. If you think it is so bad, why don’t you leave and live in a state that you like! I can think of nothing worse than living in a state where i would feel the need to wail and whine about it every day. I have better things to do with my time.

December 10, 2014 at 2:21 pm

Yes, Tough Love, you always lose on the facts and then resort to hissing and hysteria, and disgusting name calling, like calling me a he/she. When your IQ fails, you resort to bullying.

What happens in the private sector is $100 million+ payouts at retirement, as I document here:

Click to access GMIRatings_GoldenParachutes_012012.pdf

As well as a draining of the private DB system, as described by a Pulitzer winning Wall Street Journal reporter:

http://www.retirementheist.com

You have one link about $1-3 million in disgusting overpay to a firefighter. I condemn that, but that is not a consequence of DB plans, 100’s of which in the US don’t do what that one case indicates; that one case is a consequence of:

1)The fact that firefighters & law enforcement of copied the US DB military pension system, where full retirement at age 37 is allowed.

You never criticize or complain about the US military DB system, which is purely pay-as-you go… the debt, if they ever bothered to calculate it, is in the many trillions, but GASB don’t apply there, and you are totally happy with that, Tough Love; you never complain at all about that giant financial hole. If your friends get taxpayer assets, you are just fine with that.

2)The overpayment in of firefighters & law enforcement, which perhaps is better than the same workers getting paid by criminal bribes, as happens in most countries of the world.

I suggest you make a big sign, Tough Love, and go down to your local fire station (probably not even in California) and stage your own 1-person demonstration by marching around from 8am-5pm 7 days a week. You can post pictures of yourself to convince everyone you really care and aren’t just bloviating.

December 10, 2014 at 5:37 pm

Fifty-percent of CalPERS retirees live on less than $18,000/yr. I suggest that TL and Captain take that into consideration. There are always going to be people who are being paid amounts you might consider outrageous–but you don’t have the details and who are you, or me to judge that one particular person is being paid too much or too little–wherever that person is, there are officials that have set down the particulars–let them do the explaining. I retired from a municipality where the CM, who retired two years after I did, gets 7-8 times more than I–I don’t plan to jump on a soapbox–I’m glad he is sustainable.

December 10, 2014 at 10:38 pm

Why everyone is in such a hurry to declare a fire chief “overpaid”. This is not the guy reeling out hoses and waxing the truck. He is a manager of a 700 man department, who worked his way up the ladder through years of training and progressively more responsible experience. MBA graduates with the ink still wet on their diplomas can make as much or more.

Maybe you’ve led a sheltered life. There is another version of the infamous “I know a policeman who retired at 52 with $85,000 a year…FOR LIFE”

It goes like this: A mid size company near me (100-130 employees and growing) has top three execs making over $200,000 a year, plus at least that much in benefits and bonuses. Managers, nothing more than a BA among them. Several other mid level managers and sales persons make well over $100,000, without even a BA. Bennys and bonuses probably bring them over $200,000.

I say, by maxing out their 401(k)s, most of these people could have a retirement as lucrative as the fire chief and still have larger take home pay.

He’s leaving a $140,000 job to take a $180,000 position. Somebody has determined his experience, personality, and skill sets are worth the higher pay. And I am sure Pasadena was well aware of the benefit costs when they recruited him. They might even have thrown in some sweeteners.

Please stop calling fireman a GED job. If, as is often said, there are hundreds of applications for every job announcement, do you really believe a GED will get you in the door? These are professionals. By the nature of their occupation, most of the training is on the job, not classroom credits. But a trained and experienced fireman or policeman is not the same thing as an experienced roofer or plumber.

Walk a mile in his shoes, if you can, before you criticize.

December 10, 2014 at 11:28 pm

Instead of crying in your beer about what someone else has, try this.

http://money.cnn.com/gallery/retirement/2013/11/11/401k-millionaires/2.html

If you complain that all your employer gives is a 3% match, you will surely retire poor.

Heritage Foundation says the average state worker earns 12% less than an equivalent private sector worker. If the private sector worker sticks that 12% in his 401(k), he will have no need for pension envy. On the high end, state workers make 38% less. Imagine that nest egg.

It’s actually more than 12%, but that’s another story.

December 11, 2014 at 2:21 am

Douglas, You don t know what you are talking about. Perhaps the salaries are true with multinational multibillion sales, but those are not representative of average private sector)companies…..Remember, what the arrangement is…when I come in for work, I know I will be paid that day,. The severance, not guaranteed is at most 5 months. I have moved seven times for jobs, at least 600 miles each time. Most companies don t allow you in to 401k plan right away, and if you leave within five years, you are not vested in the company match. Get away from the union hall, and do substantive research. If the fire chief has such great skills, why isn’t the interviewed to be a Ceo. Place him in a large CEO job, he would be trying to retire on disability in 60 days. Alas, his old job would be an asset.

December 11, 2014 at 2:48 am

How many people receive lifetime medical and HUGE pensions while retiring in their 50’s? We are talking about California Public Employee Pensions, aren’t we? Nobody has it better.

School District budgets are about to get hammered (in California) and the K-14 – Higher Education budgets will be severely impacted by rapidly escalating CalPERS, CalSTRS & University pension costs. Those rising costs are a direct result of increased benefit giveaways, of taxpayer dollars, to public employee union members.

It is the pension funds themselves, in coordination with union demands that are strangling funds once meant to go toward students. I think our University students are beginning to understand how California Politics are working against them. Also Infrastructure costs, for just about everything, now go toward rapidly accelerating wages which further increase pension costs, fees, parking etc … I see a perfect storm developing around the next recession. Hopefully the next election cycle will be the beginning of sanity.

Spin it however you like. We’ll just have to agree to disagree.

December 11, 2014 at 5:05 am

There are more things in heaven and earth, Stuart, than are dreamt of in your philosophy.

I’m hurt. I never said these were average. But they are real. My wife was the bookkeeper. She wrote the payroll checks. She got a 3% match with a 6% contribution. I believe she was vested immediately, and also purchased a good deal of the company stock at a discount. (Alas, she was not one of the $100,000 plus group.)

If you don’t think 401s can, and do, make a viable retirement, search “401(k) millionaires”. You will find many articles similar to this:

“In fact, of the 5,500 millionaires Fidelity studied closely, 1,000 – or about 18% – earn less than $150,000 annually.”

http://blogs.marketwatch.com/encore/2013/11/12/secrets-of-the-401k-millionaires/

……………………..

$200,000 managers are not typical. Neither is the Las Vegas fire chief. He is literally one in 700. One in a thousand, if you count the volunteer firemen he also managed.

“If the fire chief has such great skills, why isn’t the interviewed to be a Ceo.”

You crack me up, Stuart! Because he’s …….a fireman! A very good one, apparently.

I don’t know why you had to move seven times for jobs. I hope your not implying that is typical private sector practice.

For the record, I have never been to a union hall. I wasn’t even on their mailing list.

December 11, 2014 at 6:32 am

“The latest CalPERS valuation reports show police and firefighters retired less than five years have an average pension of $95,127 in Vallejo, compared to $85,501 in Stockton and $78,673 in San Bernardino.” (they can retire at 50)

These aren’t even 30 year working numbers, nor do they include retiree healthcare. The average pension for Vallejo safety members working 30 years, and retiring in the last five years, is 100K – 200K. It is interesting to note that these numbers come from our poorest cities and don’t include retiree healthcare. Vallejo will soon contribute 72% of payroll toward their employees pensions. For Police Captains & Battalion Chiefs that will amount to about 140,000 dollars per year, per person, in pension costs alone.

Vallejo also pays their Miscellaneous employees 2.7@55 plus another 6.2% toward social security – an outlier to be sure, which increases their employee retirement cost even further above the norm.

“California copied as states seek retirement plans” – a Red Herring. Until we can reform the current corrupt CalPERS/ACT 37 pension plans there is no reason to start another corrupt plan.

December 11, 2014 at 12:48 pm

A multibillion multinational with a position called bookkeeper making $100k? a position called bookkeeper in a large company?Oh, ok, you got it nailed. Sure, you can have a decent amount with 401k. Of course, the at will employment arrangement might halt that at times. Move seven times, mergers, closures, politics, yes it happens, especially to grow the paycheck. I am glad to hear your endorsement of 401k for public sector employees.

December 11, 2014 at 7:44 pm

“Say, by maxing out their 401(k)s, most of these people could have a retirement as lucrative as the fire chief and still have larger take home pay.”

Sorry, for $100,000 pension (accounting for inflation) you need $2.5 to $3.3 million in your 401(k), with current safe withdrawal rates. Google Wade Pfau.

Maxing out one’s 401(k) can get you to maybe $1-$2 million, when age 65, and certainly not at age 50.

December 11, 2014 at 11:21 pm

No rank and file worker would ever save enough money in a 401K-style plan, to retire on. I saved diligently in my own 457 government plan–when I retired at the age of 72, I had enough money in the 457 to buy my groceries, and other incidentals–nothing else. That is why DB plans are the best thing for all workers–public or private.

December 12, 2014 at 1:58 am

And that is what social security is. Can we leave it at that?

December 12, 2014 at 4:15 am

No–SS is not enough to live on–I know because my spouse is on SS. People need enough to be sustainable and that is what DB public pensions do. Take a different view of this and work to make things better for everyone, like the Senator is trying to do for his Aunt. You should not be resentful of those that have something you don’t.

December 12, 2014 at 9:01 pm

The plan long ago (1970’s or so) was: SS + modest DB + DC (by nature modest) = comfortable.

December 13, 2014 at 4:26 am

Captain and spension-envy, why are you so focused on police and firefighters? Because they have the best retirement formulas? You completely ignore City Manager of Vallejo earning over $300,000 year plus benefits, plus employer paid member contributions, plus a housing allowance, plus a car allowance, plus a loan who will retire on 2.5% or 2.7% formula for risking a paper-cut and all the Water District Employees who get a similar formula and earn over $100,000 for never promoting but just staying in the same job and getting COLAs of 3% + each year.

You are looking at trees and missing the forest. Or are you one of those city/county/water district employees suffering from pension envy?

December 13, 2014 at 6:22 am

Bille, every employee group in Vallejo is a chart-topper. While I don’t disagree with you regarding the City Manager compensation package, or Assistant City Manager COMP for that matter, there are only a few of them. There are two hundred or so public safety employees, several of which cost as much, or more, than the CM.

At this point, and considering the unions have had complete control of the public purse for almost two decades, the City Managers compensation might be worth it – if he can right this ship.

The Public Safety employee unions have run the city for at least the last 15 years and bankruptcy is the outcome. If things don’t change Vallejo will be the first city in California history to file twice – they have both Public Safety grant funding and temporary taxes sustaining the current budget, and that won’t last.

I agree with you that water districts have flown under the radar. That’s because they aren’t a part of the General Fund and they have the ability to raise rates to cover their pension problem, without proper scrutiny. I hope that changes.

Vallejo is a perfect example of what happens when the unions control a city council/governing board that controls the purse strings, while also negotiating with city management that receives/wants the same perks. It’s very disturbing.

December 13, 2014 at 7:27 am

I think it’s very important that our legislatures work on fixing the current dysfunctional pension plans before working on something new. If they can’t clean up the current mess why should anyone believe they aren’t about to create the next mess?

December 14, 2014 at 2:35 am

PEPRA 2012

It really is a major step.

December 15, 2014 at 7:12 pm

Nope, Bille, I’m a DC victim. My judgement is that huge private sector post-employment payouts (golden parachutes) had driven up city manager, prison dentist, etc, pensions. If it were up to me, all public pensions would would have a cap at maybe 2X the median salary in the state.

December 16, 2014 at 12:35 am

Done.

Twice the state median salary is about what the new PEPRA law designates.

But you don’t have to go to millionaire CEOs to see private wages higher than public.

http://www.bls.gov/oes/current/oes_ca.htm#00-0000

Keep in mind that these management, marketing, engineering, and computer salaries are medians. Some make much more, and, in the private sector, salaries are about 67% of compensation, benefits are 33%. So you can add about 50% of salary to estimate total compensation.

“Management occupations” are about 6% of the state workforce, and their mean wage is about $124,000 a year, or total compensation of over $180,000 each.

December 16, 2014 at 11:49 pm

Not really. I’d include SS, so, I’d cap state pensions at 106,000-33,000=$73,000 for those in SS. The PEPRA cap is $117,000 for those in SS, about $44,000 more than I’d suggest.

And I’d do it for everyone currently getting pensions too, through a settlement in State Sovereign Default. I’d not touch anyone with a pension per service year exceeding about $1,200. I’d then have a sliding scale to fit everyone under the $73,000 cap.

December 17, 2014 at 9:19 pm

Spension,

Leaving the controversy of safety pensions aside momentarily, there is a very strong consensus in the major studies that those public employees in the highest wage percentiles are the most underpaid, compared to the private sector, both in cash wages and in total compensation. Capping their pensions, for new or existing workers would require substantial salary increases to compensate. Reducing pensions for current retirees is a non-starter. There is no way to reimburse them for already inferior total compensation.

I have no problem with a cap of $106,000, or $73,000 for those in SS, for new employees. But salaries will need to be increased….considerably, to compensate.

…………..

On safety pensions, Joshuah Raugh says “Attempting to benchmark the compensation of, say, public safety officials to private sector employees is obviously problematic. In such a case, the appropriate level of pay is simply whatever the employers and employees can agree upon – but that only leads to efficient outcomes if there is transparency about the public sector compensation packages that allows all parties, including taxpayers, to understand the value of the benefits. That transparency is currently lacking.”

There are two separate and distinct questions:

Are they overpaid?

Can we afford them?

Very different questions, if you think about it.

December 28, 2014 at 10:31 am

It is that level of twisted thought that has created the current catastrophe of which is not yet completely understood by the masses.