On a split vote, the CalSTRS board last week gave members in two unusual retirement accounts, which have a guaranteed minimum return, a $300 million credit from a surplus.

To some board members it looked like bad timing and a policy out of step with the times. CalSTRS is seeking a multi-billion dollar rate increase for the main under-funded pension system.

A board member representing Gov. Brown’s finance department, Eraina Ortega, urged a delay until the policy adopted in 2006 during different economic conditions could be reconsidered at the next board meeting.

“I do think we have to be conscious as well of what those perceptions might be when we are seeking a funding solution to the defined benefit (pension) program,” Ortega said.

Others said they wanted to keep the promise made to members when the board adopted the policy, which gives members a credit when surpluses above the amount needed for the guaranteed return reach a certain level.

“I fully understand the angst that’s around it, and I fully support taking a look at the policy,” said board member Dana Dillon. “But I find it very problematic to tell our members now that we have butted up against it, we are going to do something else.”

The board approved the $300 million credit but, as suggested by several members, will revisit the policy during the next year. Dillon is the only current board member who served in 2006 when the policy was adopted.

Like most government employees, CalSTRS members have the option of voluntarily putting money into an employer-provided “defined contribution” retirement plan, a 401(k)-style individual investment plan that CalSTRS calls Pension2.

But CalSTRS is a “hybrid” plan with two individual investment plans that, unlike a typical 401(k), have a guaranteed minimum investment return based on 30-year treasury bonds, 3.75 percent last fiscal year.

The board was told last week that giving members an additional credit above the minimum during times of surplus should, in the long run, provide a yield close to the assumed rate of return for the CalSTRS investment portfolio, 7.5 percent a year.

The accounting is separate, but the money in the two individual investment plans is invested along with pension funds in the CalSTRS portfolio, valued at $181 billion at the end of February.

Awarding the credit, difficult with the current computer system, will cost $1 million or more, estimated Jack Ehnes, CalSTRS chief executive. He said the required staff time could slow work on the development of a new computer system.

A new actuarial report last week showed no major change in the main under-funded CalSTRS pension system. It still needs an additional $4 billion a year to project full funding over 30 years and, without a rate hike, could run out of money in 2046.

Unlike other public pension systems, the California State Teachers Retirement System cannot raise employer rates, needing legislation instead. After ignoring rate-hike pleas for nearly a decade, the Legislature is working on a funding solution.

Another CalSTRS difference is that members do not receive Social Security, in addition to their pensions, and most CalSTRS members do not receive employer-paid retiree health care.

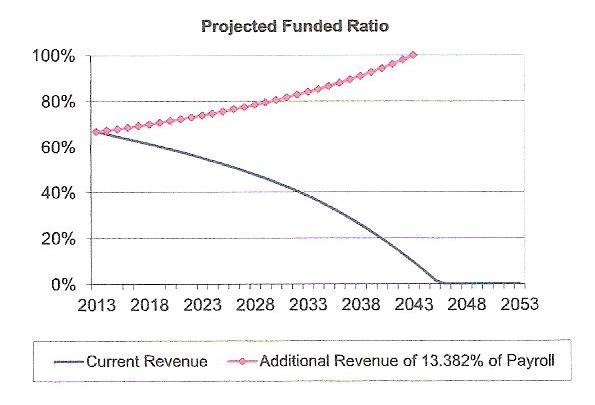

CalSTRS AT THE CROSSROADS: No rate hike, pension fund depleted by 2046. Full rate hike, 100 percent funded in 30 years. (Milliman actuaries)

The smaller of the two plans with surpluses, Cash Balance, was created in 1996 for part-time teachers, who work less than 50 percent of a full-time position for school districts, community colleges and county education offices.

Employers and employees each usually contribute 4 percent of pay. The normal payment at retirement is a lump sum, but annuity options are available for accounts of $3,500 or more.

At the end of June last year, the 31,000 non-retired members of the Cash Balance plan had a total of $169 million in their accounts. Last week the board awarded $5.5 million in additional credits and another $61,000 for annuities.

The other plan, the Defined Benefit Supplement, was created in 2001 for all CalSTRS members. Contributions to the plan come from pay beyond the normal hours of the school year, such as summer school, coaching and bonuses.

The 521,241 non-retired CalSTRS members had DBS accounts totaling $7.4 billion at the end of June last year. The board awarded $266 million in additional credits last week and another $29.6 million for annuities.

Most of the money in the Defined Benefit Supplement came from a 10-year diversion of a quarter of the teacher contribution to the under-funded main CalSTRS pension fund, 2 percent of pay from the total of 8 percent of pay.

The creation of the Defined Benefit Supplement was part of a package of legislation around 2000 that also cut state contributions and increased retirement benefits in several ways, causing much of the current CalSTRS pension under-funding.

An actuarial report from Milliman last April said that if CalSTRS were still operating under the 1990 benefit structure, the pension plan would be 88 percent funded instead of 67 percent funded.

The new Milliman report last week for the fiscal year ending last June 30, when the CalSTRS portfolio earned 13.9 percent, dropped the pension funding level or ratio by a tiny amount: down from 67 percent to 66.9 percent of the assets needed to project full funding in 30 years.

The CalSTRS actuarial “smoothing” policy spreads asset gains and losses over three years (the California Public Employees Retirement System had 15-year smoothing until last year), so only a third of the big gain last fiscal year is counted in the new report.

The CalSTRS debt or “unfunded liability” in the new report is $73.7 billion, up $2.7 billion from the previous year but $2.2 billion less than the expected increase.

In what lawmakers trying to fund CalSTRS may hope is a trend, the new report said the rate hike needed to project full funding in 30 years is 13.4 percent of pay, down 1.2 percent of pay from the previous year.

That’s still roughly $4 billion a year and a big increase from the current total contribution to the CalSTRS main pension fund, 19.5 percent of pay (employers 8.25 percent, teachers 8 percent and the state 3.25 percent).

Some good news given the CalSTRS board last week is that increased longevity, which will cause a major CalPERS rate increase, has been incorporated into CalSTRS assumptions.

“We do that now,” said Ed Derman, CalSTRS deputy chief executive officer. “So we wouldn’t anticipate the same kind of change, if any, in the next round that CalPERS had.”

A joint legislative committee is scheduled to hold a hearing Wednesday (April 9) on the California vested rights doctrine, which is believed to limit an increase in the teacher contribution to CalSTRS to 2.83 percent of pay.

Reporter Ed Mendel covered the Capitol in Sacramento for nearly three decades, most recently for the San Diego Union-Tribune. More stories are at Calpensions.com. Posted 7 Apr 14

April 7, 2014 at 1:47 pm

It may surprise my fellow commenters on this site to learn that I think the board did the right thing here, even though I sympathize with the warning issued by the DOF representative. This issue is not about the DB plan. It is about ownership. I think that the most important rule for any nation is to respect private property. Like it or not, those who contribute to the DC plan own that money, even if its in a hybrid type plan.

That said, I also think the taxpayers own their money and it should not be taken from them by subterfuge, which is what DB plans that are not conservatively arranged do (i.e., with very conservative investment return and other actuarially pertinent assumptions). The idea of putting 100 % of the risk on future taxpayers is no different than taxation without representation and should have been stopped long ago. Now, we’ll see taxpayers (and hopefully teachers themselves) burdened with unavoidable “takings” due to our past mis-management of CalSTRS. This is why we need pension reform.

But, a DC account is private property and as long as it does not put ANY risk on future taxpayers, it should not be “taken”, and that includes taking its earnings.

April 7, 2014 at 2:08 pm

Taxpayers ….REMEMBER THIS when they are asking for more money .

GIVEBACKS of such nonsense, and Pensions REDUCTIONS) to a level no greater than those of the average Taxpayer footing the bill must come FIRST.

April 7, 2014 at 2:33 pm

“Unlike other public pension systems, the California State Teachers Retirement System cannot raise employer rates, needing legislation instead. After ignoring rate-hike pleas for nearly a decade, the Legislature is working on a funding solution. Another CalSTRS difference is that members do not receive Social Security, in addition to their pensions, and most CalSTRS members do not receive employer-paid retiree health care.”

It seems to be that whoever is the most guilty of pension pillaging in the past, the employees with retroactive pension increases or taxpayers with underfunding, is making the least sacrifice today.

The contrast between NYC teachers and California teachers is instructive. In NYC, the teachers have gotten one pension increase after another, and the result has been higher taxes and cuts in services. They get Social Security and retiree health care, and their pensions are free of state and local taxes. And they are demanding more.

California teachers, on the other hand, are getting screwed.

April 7, 2014 at 3:13 pm

Larry, The teachers are only “getting screwed” when (a) compared to other PUBLIC sector workers, (b) when you only look at funding of their promised pensions WITHOUT comparing the generosity of their pensions to comparable PRIVATE Sector workers.

When the latter comparison is made … and THAT is the proper comparison because it is PRIVATE Sector Taxpayer who are being called upon to pay for their pensions ….. they are NOT “getting screwed” because their pensions (considering both the richness of the formulas AND the provisions) are ALWAYS multiples greater in value at retirement.

Rather is the Taxpayers who are getting screwed Time & Again by being told that they have to pay for it. BS …they should REFUSE to do so.

April 7, 2014 at 5:40 pm

Refusal to pay your taxes is a crime punishable by fine and/or imprisonment. Be my guest, if you want to be a guest TL. The greater good is important, and in the long run, the greater good is served when a group of people make small individual sacrifices, like paying their taxes. That said, I don’t think there is any excuse for the CA Legislature to keep dragging its feet on this issue. If it can pass a thousand new bills every year, it should be able to pass a bill funding CalSTRS.

April 7, 2014 at 5:54 pm

“CalSTRS members get $300 million from surplus”

– Surplus? And I thought they needed money because of a HUGE deficit …

April 7, 2014 at 6:30 pm

“CalSTRS members get $300 million from surplus”

Doesn’t this article state the unfunded liability grew by 2.7 billion in FY 2012-13, despite a 13.9 percent investment gain? How much does the unfunded liability grow when CalSTR’s meets their target ROI of 7.5 percent?

Now that CalSTR’s has approved yet another giveaway of our tax dollars (300 million – and that doesn’t include the guaranteed 3.75% rate of return funding for future years, which will most likely adjust upward), I guess the unfunded liability for last year grows from 2.7 Billion to 3 Billion – despite the 13.9 percent gain.

@Mike Genest, the real issue is that our school district budgets are going to get hammered due to CalSTRS poor judgment, bad management, and a Board of Directors this is more than happy to burden the educational system and tax payers as long as they believe they can CONTINUE to get away with it.

Surplus? Disgusting!

April 7, 2014 at 6:36 pm

SeeSaw, Yes, “small sacrifices”. That’s what Public Sector workers offer (VERY small sacrifices) ….. when justifiably (and to be “fair” to Taxpayers), they need to be 10+ times greater.

April 7, 2014 at 7:02 pm

Surplus my ass.

This nonsense only proves: “You can justify anything.”

April 7, 2014 at 7:44 pm

None of the commenters ever document their own individual liabilities required, via taxation, to sustain respective pension plans, TL. That is because they have nothing in the way of large sacrifices to report.

April 7, 2014 at 8:28 pm

We try to pay as little tax as possible. Garage sales, consignment stores, old cars….oh yes me an spouse are in top 8 percent of wages. We saw a recently retired school administrator won lotto, retired with a $137k yearly pension. As long as we see that, we will do our part to pay as little state and local tax as possible. Oh, it is all legal, just a bit of discipline, actually quite fun. Rasing kids the same way. They are cheaper then we are. Hee, hee, Leave the new cars to the retired public safety tribe. We buy their tradeins cheap, and pay the reduced DMV fees.

April 8, 2014 at 10:29 am

I’m really glad that it’s easy to make cuts to education when the state has cash problems. It won’t be long before UCLA costs more than USC.

April 10, 2014 at 8:21 am

Another fix that could make things worse: Teacher pension proposal would guarantee new benefits

By Steven Greenhut: http://www.utsandiego.com/news/2014/apr/09/another-fix-that-could-make-things-worse/

“Enter the latest CalSTRS plan. At a Capitol hearing on Wednesday, CalSTRS officials are floating a “hypothetical” plan that would allow them to increase the amount of money they collect from teachers to reduce the pension debt. In exchange for that give-back from teachers, CalSTRS would guarantee a 2 percent cost-of-living adjustment every year. Currently, retirees receive that annual boost – but it is not a “vested” right. The Legislature can take it away any time that it chooses.”

– Mr. Greenhut, there is nothing “Hypothetical” about what CalSTRS is proposing. The CTA floated this weather balloon about a year ago and CaLSTRS is doing what’s expected of their good soldiers. When CalSTRS and the CTA offer to pay an additional 2.83 percent of salary for a guaranteed 2 percent increase in cost-of-living adjustments you can bet it won’t benefit taxpayers, school district budgets, or our children.

CalSTRS has been giving away money in the form of increased benefits for over a decade. And, despite the pension system being severly under funded the State Legislature has been approving COLA’s for years, even though CaLSTRS has over 7 billion in diverted funds that provide retiree’s an 85% buying power protection (the money in this account is barely touched because the COLA’s keep getting approved – why?).

**”An annual actuarial report from Milliman last April said that if CalSTRS were still operating under the 1990 benefit structure, the plan would be 88 percent funded instead of 67 percent funded.”**

This is nothing more, and nothing less, than a RETROACTIVE PENSION BENEFIT. It is an additional cost that guarantee’s additional payments based on actuarial assumptions which include but aren’t limited to: the 7.5% rate of return and current longevity assumptions. The fact these groups are even proposing this scheme in the wake of the limited pension reform, which includes the elimination of RETROACTIVE PENSION BENEFITS, is disturbing and demonstrative of great ARROGANCE on the part of both CaLSTRS & The TEACHERS UNIONS – whom are asking for an additional 4.5 billion per year for thirty years (until they need more).

CalSTRS needs a serious overhaul of their Board and Management. The more I understand about their operation the scarier it gets. They have a great deal of complicity in the not too distant destruction of our school district budgets, as does CalPERS.

April 11, 2014 at 1:02 am

Guaranteeing ANYTHING (not now guaranteed) would be NUTS and a further betrayal of Taxpayers.

Remember, that no matter how bad (or costly) it gets, in Crazyfornia, what goes UP can NEVER come down.

April 17, 2014 at 6:32 am

First, thank you Mike for injecting reason, logic, law, and policy into this section before the illogical, uneducated, rants began.

Second, TL, my insurance company makes guarantees to me all the time. In fact, some of my new policies and a new annuity just arrived in the mail today. Signed, sealed delivered. Should I give them a call and just scream “FRAUD”?

Third, Captain, the rest of your comment should have included the fact that in exchange for make the 2 percent a guarantee instead of a “may have”, the contribution rates will be increased, thereby reducing the cost to the employers for the projected unfunded liability. But why include that?

April 17, 2014 at 6:34 am

Ps. My insurance company was one of the many private industry recipients of the bailout. Although, they claimed they did not need it, they took it and more. They also paid bonuses to the execs after taking the bailout. How is that possible? But we all know that doesn’t count.