President Obama signed a budget bill that cut cost-of-living adjustments in military veteran pensions last month, a few days after a judge overturned a voter-approved attempt to cut cost-of-living adjustments in San Jose city worker pensions.

Why can the pensions of veterans who put their lives on the line during military duty for the nation be cut, while the pensions of everyday state and local government workers in California are legally protected from cuts?

The answer is that case law developed by California judges over decades means the pension promised on the date of hire becomes a contract, a “vested right” that cannot be cut unless offset by a new benefit of comparable value.

Military pensions lack this court protection, and so does the general federal retirement plan, Social Security. Both can be cut. The protection California courts have given state and local government pensions is exceptional.

In what some call the “California Rule,” the pension promised on the date of hire becomes an uncuttable contract not only for service already provided, but also for service the worker will provide in the future.

The “California Rule” bars what some think is the solution for unaffordable government pension costs: cutting the pensions current workers earn in the future, while protecting pension amounts already earned by time on the job.

Lower pensions for new hires, as required by recent reform legislation, can take decades to yield significant savings. Bargaining to increase worker pension contributions can yield limited or temporary savings and require offsetting pay raises or benefits.

So, the bipartisan Little Hoover Commission called for legislation authorizing cuts in pensions current workers earn in the future. An initiative proposed by San Jose Mayor Chuck Reed and others would put a similar provision in the state constitution.

Private-sector pension plans can cut pensions earned by current workers for future service. Some states base pension protection in property law, not contract law, and in some states the pension becomes a contract on the last day on the job, not the first day.

A study cited by Reed and others looks at the origin of the “California Rule” and argues that it’s an error: “Statutes as Contracts? The ‘California Rule’ and Its Impact on Public Pension Reform” by Amy Monahan of the University of Minnesota Law School.

Monahan

The “California Rule” has only been adopted in a dozen states, Monahan said. Two of the states, Massachusetts and Oregon, later modified the rule to allow cuts without offsetting benefits or cuts in pensions current workers earn in the future.

California courts were among the first to hold that pensions are contracts. An early ruling, Kern v. City of Long Beach in 1947, allowed some flexibility, Monahan said, resulting in three appellate cutting pensions current workers earned in the future.

Then in a “bombshell” ruling in 1955, Allen v. City of Long Beach in 1955, the state Supreme Court allowed reasonable changes consistent with the theory of a pension system if cuts were offset by a new benefit of comparable value.

Monahan argued that by imposing a highly restrictive rule without ever finding clear evidence of legislative intent to create a contract, California courts broke with traditional contract clause analysis and infringed on the power of the legislative branch.

“California courts have held that even though the state can terminate a worker, lower her salary, or reduce her other benefits, the state cannot decrease the worker’s rate of pension accrual as long as she is employed,” Monahan said.

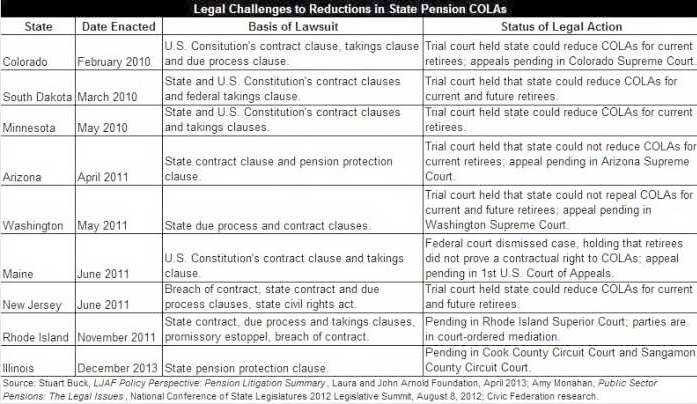

As in the federal budget deal that cut military pensions, the cost-of-living adjustment has been the main target as a number of states struggle to manage growing pension costs.

COLA cut legal challenges (Institute for Illinois Fiscal Sustainability)

Since 2010 nine states have enacted pension COLA cuts, all challenged in court, according to a summary issued this month by the Institute for Illinois Fiscal Sustainability, a non-partisan business group.

Illinois has the nation’s most troubled state pensions, only about 40 percent funded. A reform enacted in December expects to get most of its savings from eliminating automatic 3 percent COLAs, except for smaller pensions below a threshold.

Like several other states, Illinois has a provision in the state constitution that says pensions are an “enforceable” contract that “shall not be diminished or impaired.” The reform reduces employee contributions, but it’s not clear whether that offsets the cuts.

Two states paired by the legalization of recreational marijuana and having football teams in the Super Bowl next month, Washington and Colorado, also have enacted cuts in pension COLAS that are being challenged in the courts.

Deep cuts in COLAs can seriously erode the pensions of long-time retirees. The two big California state pension systems, CalPERS and CalSTRS, both have programs that keep pensions from falling too far below their original purchasing power.

The California State Teachers Retirement System provides an automatic annual increase of 2 percent of the initial monthly payment that is not tied to changes in the cost of living.

Teachers do not receive Social Security, which does keep pace with inflation. An important supplemental program, which gets about half of state CalSTRS funding, keeps pensions from falling below 85 percent of the original purchasing power.

In the giant California Public Employees Retirement System, most members receive Social Security in addition to pensions. State and non-teaching school members receive 2 percent COLAs, compounded unlike CalSTRS.

Local government employees can bargain for COLAs of 3 to 5 percent, limited to the national rate of inflation. State and school pensions can’t fall below 75 percent of original purchasing power, local government pensions below 80 percent.

In San Jose, one of the provisions of Measure B approved by 70 percent of the voters in June 2012 would have allowed the city council to declare a fiscal emergency and suspend retiree COLAs for up to five years.

A superior court judge, citing some of the same rulings as Monahan, said the COLA suspension was a violation of vested rights, along with a key provision intended to give the city the option of cutting pensions earned by current workers in the future.

The bipartisan federal budget deal cut the military pension COLA by one percentage point until age 62, when the pension would be recalculated as if the cut never happened.

The cut is expected to save about $6 billion on military pensions that cost $52 billion in 2012, nearly 50 percent more than in 2002, the Washington Post reported. A person retiring at the average age of 44 would lose about $30,000 over their lifetime.

Congress approved a bill last week exempting disabled military retirees from the COLA cut. Military and veterans groups are expected to push for a repeal of the COLA cut as the Senate works on an omnibus Veterans Affairs bill.

Reporter Ed Mendel covered the Capitol in Sacramento for nearly three decades, most recently for the San Diego Union-Tribune. More stories are at Calpensions.com. Posted 21 Jan 14

January 21, 2014 at 12:16 pm

Quoting…. “Why can the pensions of veterans who put their lives on the line during military duty for the nation be cut, while the pensions of everyday state and local government workers in California are legally protected from cuts? The answer is that case law developed by California judges over decades means the pension promised on the date of hire becomes a contract, a “vested right” that cannot be cut unless offset by a new benefit of comparable value.”

Yes, decisions by judges who themselves belong to the same DB Plans and PERSONALLY benefit greatly from THEIR OWN self-serving decisions.

Taxpayers RIGHTFULLY must renege on ALL such pension “promises” …to the extent they result in pensions of greater VALUE AT RETIREMENT (including BOTH the richer formulas AND the richer provisions …..very young retirement ages,COLAs, etc.) than the average of those granted PRIVATE sector Taxpayers.

And doing so would require reneging on AT LEAST 1/2 of all non-safety pensions and 2/3 to 3/4 of all safety worker pensions.

The financial “mugging” of Private Sector Taxpayers by the VERY greedy Public Sector Unions/workers must end.

January 21, 2014 at 3:31 pm

Why not just fire them all– that wouldn’t be discriminatory– and then force them to reapply. Voila. Contract broken.

January 21, 2014 at 4:11 pm

“Envy according to the aspect of its object is contrary to charity, whence the soul derives its spiritual life… Charity rejoices in our neighbor’s good, while envy grieves over it.”

Thomas Aquinas

January 21, 2014 at 4:57 pm

SDouglas47, Smart move, quoting the intelligent ,… especially since when you speak your own mind you say things as asinine as this (from your comment on an earlier discussion):

“If a pension system continues to pay out the required benefits over time, with marginal changes in the contribution rate, it is “funded”.”

January 21, 2014 at 5:31 pm

Oh, how easy it is to throw out figures without any backup. Let’s see a list of local governments whose retired employees bargained three to five percent COLAS. (I think that Stockton gave 5% and it is now in bankruptcy.) Most municipal and state retirees get maximum 2% COLAS, depending on the CPI. So, don’t mention what is the usual, because it would not make the enviers’ heads explode soon enough–and don’t mention that a retiree must be retired for a minimum of two calendar years before any COLA kicks in. I personally received CalPERS COLAS of 1.4% and 1.6% on my third and fourth retirement years–a long way from your head-exploding, quotes.

January 21, 2014 at 5:51 pm

Sure Seesaw, you (as a Public Sector retiree) complain that the author is perhaps a bit aggressive in stating the COLA percentages ,….. but I don’t see you mentioning that while YOU get the 2% or 3% (or whatever),COLAs, Private Sector Pensions have ZERO COLAs …. always.

That’s what Public Sector Plans should get …. zero COLAs …permanently.

You’re not “special” and deserving of a better deal on the Taxpayers’ dime.

January 21, 2014 at 6:09 pm

New study out from George Mason University on State Fiscal Conditions…………

The 5States in the worst condition are NJ, Ct, Ill, RI,and CA.

Quoting … “In terms of long-term solvency (the most critical issue), New Jersey and Illinois are at the bottom of the heap. Pension plans and union activism are to blame. All five states at the bottom of the list have one thing in common: they got that way via “progressive” extreme-liberal politics, fueled by union activism, and promises that cannot possibly be met.”

Surprise surprise …. Public Sector Unions are the driving force.

———————————————————————————-

Public Sector Unions are a CANCER inflicted upon Society and should be outlawed.

January 21, 2014 at 6:38 pm

I know, TL. I am married to a private-sector retiree whose DB pension amount is less each month than the premium cost for his secondary-to-Medicare, medical insurance premium. Do you think he is happy to have me for a backup? Your divide and conquer strategy is not going to work in the long run, TL. Be careful–your head might explode.

January 21, 2014 at 7:09 pm

” while YOU get the 2% or 3% (or whatever),COLAs, ”

……………

She just told you. It’s not “whatever”, it’s 2% …OR ….CPI, whichever is less.

The devil is in the details. I read one blogger recently who wrote that the Stockton 5% COLA SeeSaw referred to is “higher than the inflation rate the last few years. No wonder the city is broke.”

I did not check ALL the Stockton contracts, but the one I did check specified a MAXIMUM 5%.

January 21, 2014 at 7:38 pm

We should pass a law that removes any question of the ability to modify pensions, but only do modifications when they are in the service of justice, if those pensions are unfair relative to the rest of society, such as when pensioners are made to be some kind of a privileged class relative to and at the expense of others. I’d apply a Rawlsian test, the so-called “veil of ignorance” suggesting in “A Theory of Justice” to answer the fairness question. Rawls work was considered seminal in the development of liberalism. It’s ironic how far those identified as political liberals today have departed from its essential premise.

January 21, 2014 at 8:15 pm

Cost of living adjustments are not automatic and are capped at 2% for State employees. Further a 2% raise is paid for with dollars now worth 98 cents. Costing the taxpayers nothing.

January 21, 2014 at 8:57 pm

Charles, sounds like you’re one of the “best and brightest” we keep hearing about ??????

January 21, 2014 at 9:45 pm

There’s another new study out.

This study examines the long-term effects of pension reforms on employer costs and on state budgets for a sample of 32 plans in 15 states.

The results show:

for most plans, the reforms fully offset or more than offset the impact of the financial crisis on the sponsors’ costs.

for the sample as a whole, pension costs as a share of state-local budgets are projected to eventually fall below pre-crisis levels.

http://crr.bc.edu/briefs/state-and-local-pension-costs-pre-crisis-post-crisis-and-post-reform/

……………

Surprise surprise …. another study:

” Are City Fiscal Woes Widespread? Are Pensions the Cause?”

” the answer to both questions appears to be “no.”

Dang unions!

January 21, 2014 at 10:09 pm

Interesting article out today ………….

http://www.palisadeshudson.com/2014/01/burgling-the-future/

The following is the first comment …. should be required reading for elected officials EVERYWHERE…

Steve Bourg January 18, 2014 at 9:57 am

As a consulting pension actuary, I handle/administer 100 retmt plans — DB and DC — almost all are private sector companies, large and small. As such, I’ve seen pay & census data and bft packages for private sector companies — for 30 years, for ALL types of private sector companies — companies who pay the taxes to permit govt to exist.

I can definitively say, with no reservations and with 100% accuracy — that pay and bft packages in the govt sector are WAY out of proportion, are absolutely egregious, are maddeningly complex and completely unaffordable in the short and long-term. Paul Volcker and the NYTimes are outrageously clueless. Look at that first sentence in the NYT article you linked to. The article states right off the bat, that govt services have been drastically cut. Really? Not in CA, IL, NY, CT MD……and every other blue state with govt unions that guarantee exhorbitant pay and bft, particularly DB pension bfts. There’s been no cutting at all. And in CA and IL, the pension bfts are written in stone in the states’ constitutions. The amount of misinformation about govt pay and bfts is astounding. Has the NYT EVER investigated what a pay/bft package is worth for a 20-yr ‘career’ policeman? No. But in the 20yrs of working the pay avgs 100k, the healthcare 20k, and then in retmt starting at age 42, the 40 yrs of pension and health-care adds to another $4M….meaning $6M over 60 years by just working 20 yrs — that’s 300k/year for the 20 yrs — pretty sweet deal. But no one adds it up and

January 21, 2014 at 10:17 pm

last sentence (above) got cut off….. here it is again…

No. But in the 20yrs of working the pay avgs 100k, the healthcare 20k, and then in retmt starting at age 42, the 40 yrs of pension and health-care adds to another $4M….meaning $6M over 60 years by just working 20 yrs — that’s 300k/year for the 20 yrs — pretty sweet deal. But no one adds it up and shouts it to the private sector public who pay for it all. Has any of that been cut? No.

January 21, 2014 at 10:27 pm

jskdn, who is going to be the decider of what is in the service of justice? With Warren Buffet and the rich casino man each earning millions/day last year, it is really in the interest of justice to weed out those pesky public pensioners, 98% of who earn less than $100,000/yr. isn’t it.

January 21, 2014 at 10:29 pm

He didn’t construct the system, TL–he is just reporting on it. You get the trophy for being the biggest snark.

January 22, 2014 at 1:47 am

@SeeSaw People are constantly making justice arguments for policies, many which have little to do with actual justice. In this case it clearly does involve justice and should be done. Taking money from poorer people with horrible retirement prospects so that government employees can have fabulous retirements ought to be indefensible, although I have no doubt the pension privileged will find ways.

January 22, 2014 at 1:55 am

” The amount of misinformation about govt pay and bfts is astounding.”

Now there’s an understatement.

Can we verify that even ONE policeman who ” in the 20yrs of working the pay avgs 100k,”?

Your ” consulting pension actuary” is doing TL math.

January 22, 2014 at 2:14 am

Grow up seesaw ……….. “snark” is having to deal with Unions that thinks it’s fine, dandy, and OK to SUE to be able to continue “spiking” their pay & pensions.

You know what they say about wrestling with skunks……

January 22, 2014 at 3:39 am

Apparently this article actually has nothing to do with military pensions.

Mayor Reed alluded to it and Judge Lucas clearly ruled:

The city can’t reduce pension formulas, but they CAN ” cut employees’ salaries to offset its increasing pension costs.”

If San Jose, or any other government wants to reduce pension costs, all they have to do is cut pay. Lower immediate pension costs AND lower future pensions will automatically follow.

If an employee now earns $4,000 a month and the city contributes 10% of salary to the city retirement system, reduce the workers pay to $3,600. An immediate savings of $400 in salary AND $40 in pension costs. That’s $5,280 annual savings.

AND, when the employee retires three years from now, his pension will be calculated on $3,600 instead of $4,000. We’re saving money hand over fist, WITHOUT breaking anyone’s contract.

Win, win.

OR, you can do as the state, and many local governments did, and achieve the same effect by simply NOT passing any COLAs for the last five years.

The cup is at least half full.

January 22, 2014 at 3:43 am

I belong to CalPERS and CalPERS does not allow spiking of pay, TL. I am not connected with, and I have nothing to do with any groups or individuals who are involved in spiking. So I won’t put those shoes on, and I am nowhere near any skunks–but I can smell you all the way from New Jersey!

January 22, 2014 at 3:48 am

Well you talk a good talk jskdn but you have absolutely nothing to say. What fabulous retirements are you referring to? I already give 70% of my gross pension check over to taxes and medical insurance premiums–doesn’t leave much for, “fabulous”.

January 22, 2014 at 4:11 am

Oh Toughlove…”the mugging of the private sector”? Puuulease! You seem to have fallen off the turnip truck again yesterday.

Let’s see who got mugged:

Jim Cramer – Bail Out Wall Street now! Wake up Bernanke!!!

Hank Paulson – “by quickly enacting a program to stabilize our financial system”

Inside Job:

Michael Capuano – “I have some people in my constituency who have robbed some of your banks who say the same thing [you are] sorry, trust us, we won’t do it again. No one is forcing you to take the money”…

Dick Fuld’s Bonus as Lehman Brother’s Collapses

And the list goes on and on…

January 22, 2014 at 4:23 am

Oh but there is one more… the free market was abandoned and bailed out by the public sector, government, the people, the taxpayers.

January 22, 2014 at 4:49 am

Billie, Some, such as yourself, will deny the reality right until the end, and then amazingly say……

What happened?

January 22, 2014 at 6:31 am

I urged everyone I saw to see “Inside Job” in 2010, Billie. I got a lot of “rolled eyes”. The perfect pairing for that documentary was a fictional movie, “Margin Call”. I doubt that TL will go out to view, “The Wolf of Wall Street”–it would pain him too much to see how those brokers lived while they were scamming the gullible.

January 22, 2014 at 4:50 pm

Seesaw, I just saw the Wolf of Wall Street. While the move was only “pretty good”, DiCaprio’s performance was exceptional. While that may or may not accurately represent the brokerage operation it was based on (I don’t know), it’s a far cry from how brokerage firms operate today.

And I’d bet dollars-to-donuts that the activities in that move much closer represent the goings-on in Public Sector Union halls.

January 22, 2014 at 5:59 pm

Oh please, TL. The “union halls” as you refer to them don’t exist like they did in the private sector. All the employees get memos from their reps and go to a meeting and cast a vote–period. There are no “halls”. We can agree on one thing–DiCaprio was exceptional.

January 22, 2014 at 6:28 pm

Odd how no-one here comments on the sentence about `a person retiring at the average age of 44′ ….

That is right, the average age of retirement from the military is 44.

And one can retire as early as 37.

I think fewer than 1/5 of military service folds have been in battle. I would never deny COLAs for anyone who served more than 1 month in battle.

So for the 4/5 that have not been in battle, why guarantee such an early retirement? That is not the issue, though. Their pensions are still guaranteed, just the COLAs are not allowed for retirement through age 62.

Most non-battle retirees between age 44 and 62 take a second job.

The main thing done here is to eliminate COLAs in the military pension during the time when a second job is taken…

Nice debate http://www.pbs.org/newshour/bb/military/jan-june14/pensions_01-02.html . A Bush-era appointee argues for taking away the age 44-62 COLA.

Interesting that none of the pro-private sector folks who usually comment that COLAs are bad aren’t commenting on the military pension situation. They also usually comment that early retirement in the public sector (as early as age 50) is bad too.

But the military allows retirement as early as 37. No pro-private sector folks commenting on that.

And where exactly does the US keep track of the debt for future military pensions and health care? As far as I know, those are pay-as-you-go systems, with no pre funding at all. As pay-as-you-go systems, they are not subject to any accounting for future debt at all.

January 22, 2014 at 7:12 pm

Ed,

It’s not only the vested rights principle based on the California Constitution, but the federal constitution as well. As the California Supreme Court wrote 20 years ago, in Legislature v. Eu, in overturning a ballot initiative that amended the Constitution and removed then exisiting legislators from continuing in the retirement system:

“We agree with Lyon v. Flournoy, supra, 271 Cal.App.2d 774, that, in light of prior California decisions consistently extending federal contract clause protection to state public officers, it is simply “too late” to retreat from the clear implication of those holdings. We conclude that the pension restrictions of Proposition 140 are unconstitutional under the federal contract clause as applied to incumbent legislators because they infringe on the vested pension rights of those persons.”

January 23, 2014 at 4:06 pm

Oh, where art though, Tough Love, Captain, and all, to comment on the one portion of the public sector that allows retirement at age 37?

As I said, anyone with real battle experience deserves it (and lifetime health care).

But it is unusual that military folks who have never been close to battle can retire at 37, and that there is so much resistance to COLAS being cut back for double-dippers who work between age 37 and 62.

And no-one seems to call for pre-funding of those public sector pensions.

January 23, 2014 at 6:17 pm

Spension, as a military vet myself I would like to weigh in here. This blog is “Calpensions.” There are other blogs (I also follow Pension Tsunami) that have a broader focus than this one. The retirement system for the military is pay-as-you-go and it’s a mess, along with the military disability system. The VA’s problems are also extensive. The entire system is in need of serious overhaul but the veterans’ organizations have the same blinkered outlook as Calpers, Calsters, and the public employee unions of the Golden State.

But let Calpensions be Calpensions, and let other blogs do their thing. The beauty of blogs is that they allow focused attention on specific areas that in the past would have escaped sustained oversight.

January 23, 2014 at 6:33 pm

spension, And WHEN have I done that?

——————————-

You’re an idiot

January 23, 2014 at 9:11 pm

An aside from this post’s article, but I noticed from Pension Tsunami that CalPERS has recently put out updated actuarial reports. I went through them and failed to find one important number: the funding ratios for 6/30/13, which would have been expected from previous years’ experience. Was anybody able to find them tucked away inside one of the larger reports somewhere?

January 23, 2014 at 10:59 pm

Well… all sorts of off topic issues are brought up in this blog, like: the influence of public unions on elected officials, private pensions, name calling (`You’re an idiot’ says Tough Love above, which of course is a wonderful compliment coming from the disorderly cerebral cortex of Tough Love).

And the first paragraph of this post is indeed about: military pensions. There is a transition to the California rule, noting the more protected nature of California pensions, but the balancing advantages of the military system are omitted.

A primary argument I’ve heard for the age 50, 55 etc early retirements in the public sector is: The Military allows retirement at 37.

So if the Military pension age were 62 (for non-battle service), perhaps a big portion of the California public pension debt would never have arisen.

January 24, 2014 at 12:30 am

Quoting spension… “A primary argument I’ve heard for the age 50, 55 etc early retirements in the public sector is: The Military allows retirement at 37.”

You’ve heard ?

From whom …. Public Sector workers trying to justify their absurdly young, full (unreduced) retirement ages?

And oh yeah, it makes a lot of sense,…… giving the routine CA career cop the pension of a military General.

—————–

You’re an idiot.

January 24, 2014 at 2:39 am

Berryessa Chillin’, there’s a two year lag for county & local government actuarial reports, and a one year lag for the State plans and School Districts. For the County and Local government plans the actuarial reports are as of June 30, 2012. Those are the just released and most current reports.

For Vallejo the contribution rate for safety will increase from 47.4 of payroll to 50.8%. Even though Vallejo is paying almost 3X the cost of the pension plan their year over year unfunded liability, for just the safety plan, grew by 27 million dollars to an unfunded liability of 152 million dollars. Their funding ratio dropped from 66.4% to 60.9% (page 21).

According to CalPERS, and these numbers/projections already reflect the 12.1% gross gains of 2012-13, the Vallejo contribution rate increases dramatically going forward (as do all CalPERS plans). The Normal employer cost for a 3@50 plan is about 17% of payroll.

CalPERS has a new feature in their actuarial reports which projects contribution rates beyond two years which was the norm for CalPERS (Thank You Chief Actuary Alan Milligan). The latest report extends projected contribution rates to the Fiscal Year 2019-20, which should help cities better anticipate future budget busting expenses.

The current cost for Vallejo is 47.4% of payroll. Beginning July1, 2014 the cost increases to 50.8%. CalPERS projects the 2015-16 contribution rates to increase to 53.8%.For FY 20116-17 the Vallejo contribution rate is projected to grow to 56.7% of payroll. 2017-18 projects cost to grow to 59.6% of payroll. 2018-19 projections are 62.6%, and FY 2019-20 costs, as percentage of payroll, are projected at 65.5% (page 26).

CalPERS makes a note that, “Consequently, these projections do not take into account potential rate increases from likely future assumption changes. Nor do they take into account the positive impact PEPRA is expected to gradually have on the normal cost.”

According to a recent Ed Mendel blog, “CalPERS plans rate hike, third in last two years” ( https://calpensions.com/2014/01/06/calpers-plans-rate-hike-third-in-last-two-years/ ) the additional cost that can be added to the numbers I’ve mentioned above, for safety, ranges from 5.3 – 9.3 percent of payroll to cover the cost of increasing longevity. That would increase Vallejo’s contribution rate to somewhere between 70.8% – 74.8% of payroll by FY 2018-19. There is no way Vallejo can afford those increased costs and it may put them back into bankruptcy. All of those numbers CalPERS can continue to earn 7.5% returns of the funds they do have and their customers can continue to pay 7.5% interest on the funds CalPERS/Cities do not have.

It’s important to note that, in the case of Vallejo and many other cities with dismal funding ratios, the 7.5% ROI CalPERS projects is based on 100% funding. If you only have 60% of required funding to invest the 7.5% rate of return means the city is only earning based on the 60% of assets, while being charged 7.5% interest on the 40% unfunded liability.

If you care to look at Vallejo’s CalPERS actuarial report and the pages I’ve referenced, here is the link: http://www.calpers.ca.gov/eip-docs/about/pubs/public-agency-reports/cities-towns/2012/vallejo-city-safety-2012.pdf

It takes a 100% gain to recover from a 50% loss. If your achieve a 7.5% return on investment every year it takes 9.5 years just to get back to 100%.

January 24, 2014 at 4:22 am

One more point of fact you left out about the George Mason University Study…it is in fact he Mercatus Center that published the study. Not sure why you would neglect to leave out that little fact but then again, facts are not your strong point. The Mercatus Center was founded by Richard Fink the executive vice president of Koch Industries. Not sure why you neglected that fact. The Mercatus Center moved to George Mason Univeristy after a $30 million grant from the Koch Family in the mid-1980s before assuming its current name in 1999.

Wow, $30 million in the mid 80’s is like $200 million today. I hope you weren’t trying to hide the Koch Family name from the flawed research and reports they put out.

January 24, 2014 at 2:38 pm

Not a peep opposing retirement at 37 years old from Tough Love or Captain. Nor any criticism of 100% pay-as-you-go public pension funding.

Guess those things are just fine with Tough Love and Captain. Kind of puts things in perspective….

January 24, 2014 at 5:32 pm

Required reading for anyone who TRULY believes in in Public/Private Sector compensation equality and “fairness”……… and who ISN’T looking for ways to distract from it by highlighting the perks and benefits rarely given to anyone OTHER THAN Private Sector CEOs, CFOs and other very high level executives:

http://unionwatch.org/how-public-employees-have-superior-rights-and-entitlements/

January 24, 2014 at 5:58 pm

Captain, thanks for your getting into the numbers and explanation of the delayed funding ratio number.

Spension, once again, mission creep. The military retirement mess deserves its own blog and dedicated experts. California is big enough of a problem to tackle here. Now if only reporters from the big dailies and TV news stations were paying attention to this blog, we might get something better than the Bay Area Group’s insipid Professor Budget or whatever that cartoon character’s name is.

January 24, 2014 at 6:39 pm

And comparing with the private sector is not mission creep?

In any case, it is Ed Mendel who introduced the comparison with the military pension system

So I assume Berryessa Chillin’, Tough Love, and Captain (maybe even they are one person) have no opposition to retirement at 37 years, and pay-as-you go funding. Certainly they’ve expressed no opposition.

January 24, 2014 at 9:04 pm

Josh Rauh (Stanford) has been giving a free web class on public sector pensions for the last few months. Today they are webcasting a symposium where several groups of students will present “innovative ideas” for the future.

https://www.gsb.stanford.edu/events/innovative-ideas-future-us-public-sector-pensions-symposium

January 24, 2014 at 9:38 pm

spension…….so, you not only despise the Private Sector that pays all of the Public Sector’s bills…..but you ALSO despise the military ….. sweet gal, aren’t you

P.S., other than for the not-working materially disabled, no, military pensions should not “start” (w/o appropriate actuarial reduction) before say age 55, and then only after 30+ years of service.

January 24, 2014 at 9:45 pm

Spension, I have a big problem with most military personnel retiring in their late 30s and 40s when they have many years of good service left. Young retirement is appropriate for certain MOS (Military Occupational Specialties) like infantry, which is a young man’s game. But most MOS have civilian counterparts (granted the military work conditions are often far more strenuous than civilians in the same field) that would allow servicemembers to work in various capacities to their late 40s or 50s in a deployed location. I know because I did deploy in my 40s to Afghanistan. I couldn’t hang for very long with the grunts in the Hindu Kush, but most combat support service jobs (such as I was in) did not require the stamina and strength of a twenty-something male. In my opinion the military squanders a very productive last decade from the average retiree’s career. There actually have been papers done on military retirement reform by the DOD and think tanks, that point out this phenomenon. Unfortunately, the retired military associations, even though of generally conservative politics, are as obstructionist toward retirement reforms as the far-left SEIU and their ilk are in this state.

My ideal military pension would be a defined contribution, paid into an individualized account, that would be designed to give the combat arms guys enough to create an annuity of 50% of base pay after 20 years. Non-combat arms could be a DC structured along the lines of 60% at 30 years. When guys get out, that could be put into a civilian retirement vessel or used tax-fee by retirees to set up businesses, education (although the GI Bill is excellent!), etc. Of course, that would force the military to pre-fund retirements, which is anathema to the status quo.

January 25, 2014 at 12:06 am

Well, thank you, Berryessa Chillin’. I think DB pensions reduce the longevity risk, although annuities can do that too. The problem with purchase of an annuity with a lump-sum purchase from an individualized account is if you pass away a few years into the payout period you see a big loss. That was originally a major reason for employer-paid DB pensions…. you could not identify the balance as individualized, so conceptually it was more like insurance that kept paying you until you perhaps survived to 95, but you didn’t perceive a personal loss if you died at 70.

Additionally, private sector annuities are remarkably expensive. Every time I look at them I keep everything in my DC accounts.

Even Vanguard’s seem to function below my own DC estimates.

Otherwise quite a rational response, Berryessa Chllin’.

Tough Love, you embarrass yourself once again. As for my attitudes, my grandfather was routed in Washington DC by MacArthur, who was never appreciated in my family. We admire Smedley Butler.

January 25, 2014 at 4:33 am

spension…What no comment, not even an irrelevant insult?

Lets try again:

—————————–

Required reading for anyone who TRULY believes in in Public/Private Sector compensation equality and “fairness”……… and who ISN’T looking for ways to distract from it by highlighting the perks and benefits rarely given to anyone OTHER THAN Private Sector CEOs, CFOs and other very high level executives:

http://unionwatch.org/how-public-employees-have-superior-rights-and-entitlements/

January 25, 2014 at 4:46 am

Spension, what’s with all the personal attacks? I think Berryessa Chillin’ makes excellent points regarding both another abused pension system/plan while pointing out that taxpayers only have enough time, energy, and influence to tackle the unsustainable pension plans at the local level.

Your arguments seem to have degenerated from deflection to personal attacks. Now you’re calling me out to comment on this article. From the limited Info I have on this topic it sounds like our military leaders are in the same predicament as our local governments; how do you fund pensions when you need those financial recourses to maintain/improve your core mission.

Spension, I agree with some of your comments on this topic. What you haven’t mentioned is how much military retirements cost. What is the formula and how much are they paid? Do they pay the same wages as California, provide the same pension formulas, and have all the additional add-ons that inflate pension payouts in the golden state? If you want to compare military pensions to California public employee pensions, especially safety pensions, it would help to understand the numbers.

The article I’ve read on this topic was very good. I’ll have to try and find it and then maybe I’ll have more to say. In the meantime maybe you can comment on this post – and also my post above regarding Vallejo pension contributions increasing to 75% of payroll.

I’m staying focused on California pension & financial issues. Between State, County, Local, and School District pension and budget issues it’s about all I can stomach. IMO, we’re in big trouble at every level of government.

January 25, 2014 at 6:49 am

Tough Love, your linked article is as disturbing as it is interesting. Just when I thought I’ve seen it all these types of activities leave me shaking my head in disgust. I agree with the author that the present form of collective bargaining needs to end.

January 25, 2014 at 7:25 pm

The Bill White article at Union Watch is a hoot.

I can’t wait for contractor A in a public bidding process, who lost the bid, suing over the contract given to contractor B, who got the contract.

`Failure of equal protection!’ would scream contractor A. `You gave contractor B a contract and not to me! You must treat us equally, and give us both contracts!’

Contracts with public workers are not a failure of equal protection. If they are, I’ll demand the same contract given to General Dynamics or to Lockheed-Martin.

The pension contracts with public workers were bad moves by our elected officials. The buck, unfortunately, stops with us who elected them.

And the way out of the contracts is bankruptcy at the local level and Sovereign Default a the State level.

Never any point to comparing with private sector pensions… the private sector fraud dwarfs the public sector greed. Just read in http://www.retirementheist.com about how Cigna, IBM, etc, etc, manipulate discount rates, sell portions of their companies in complicated fashions to dump pension responsibilities, and dump pensioners on the PBGC at taxpayer expense.

If you compare to private sector pensions, you condone really disgusting fraud, well documented by Wall Street Journal reporter Ellen E. Schultz in http://www.retirementheist.com .

Sorry, delicate little boys Captain and Tough Love, if you perceive the hard facts as an attack on your sensitive natures.

Oh, Tough Love, `Pay the Bonus’. Still have the Bonus Bond (cancelled by payment) of my WW1 Marine grandfather.

And Captain, looks to me like retirement at 37 is just fine with you. Also pay-as-you-go.

The current yearly pension payments for the US military are something like 52 billion $. Had it been pre-funded, there should have been $1 trillion or so saved. So there is about $1 trillion debt from failure to save for military pensions.

As far as I know, the military multiplier is 2.5%. So the military plan is `2.5% @ 37′.

http://militarypay.defense.gov/retirement/

January 25, 2014 at 8:38 pm

Spension, my preference for DC over DB for military personnel is based on the highly-transient nature of military personnel. A majority of enlisted get out after the first hitch, so DC would let them take something away from their 3-6 years. To utilize the cost-saving nature of DB, perhaps career-identified servicemembers could be given the option of converting their funds over to a DB plan. My personal observation is that older military personnel are cautious financially and most would jump at the chance of a pension backed by the government rather than trying to invest the money themselves.

January 25, 2014 at 9:45 pm

Captain, You’re wasting your time expecting a directed response to a reasonable question asked of spension,

Because she CANNOT answer such a question in a way that supports her agenda (delaying/stopping material Public Sector pension reform and a continuation of the incredibly unfair treatment of Private Sector Taxpayers), she simply goes back to the Union tactic of distraction by throwing the “kitchen sink” into the discussion … which ALWAYS seems to include the misdeeds of the Private Sector and the demand for “Sovereign Default” as a pre-condition to material pension reform, knowing full well that States cannot declare Bankruptcy, and many cities (while on an unstoppable path towards Bankruptcy) cannot YET meet the legal requirements.

We need to stop digging the financial hole we are in even deeper …… NOW.

spension is a charlatan with an agenda.

January 25, 2014 at 11:38 pm

The sensitive, fragile man `Tough Love’, who signs off posts to me with `You’re an Idiot’ wants me to answer Captain’s question,

`Spension, what’s with all the personal attacks?’… my answer, I don’t make personal attacks.

Or was it,

`What is the formula and how much are they paid?’… my answer, 2.5% @ 37, which Tough Love says `Captain, You’re wasting your time expecting a directed response to a reasonable question asked of spension’.

Well, 2.5% @ 37 is in my opinion a directed response.

Or was it,

`maybe you can comment on this post – and also my post above regarding Vallejo pension contributions increasing to 75% of payroll.”

I’ve answered this many times, I don’t think the employer portion should exceed an average of 10%, with bulges no greater than 15%, balanced by declines to 5%. 75% is a travesty.

Sensitive man Tough Love *never* give any solution whatsoever to implement any kind of public pension reform in California at all. Just rants at any serious recommendation to really roll up our sleeves and fix things.

January 26, 2014 at 12:10 am

spension….the SUBJECT is non-military Public Sector pensions…. NOT military pensions (because unlike the States, the Federal Gov’t can print money … still a problem, but a MUCH different problem).

You’ve shifted it to “military” pensions as just another one of your MANY distracting tactics.

You’re a charlatan with an agenda.

January 26, 2014 at 12:36 am

spension…. Follow-up…

You wanted a specific recommendation. Ok, widespread support for Mayor Reed’s proposed Constitutional change to allow a reduction in the pension accrual rate for the FUTURE Service of CURRENT workers. It won’t address the huge liability owed for PAST Service Service accruals (a harder problem), but it will help stop digging the hole deeper.

That’s future service reductions WITHOUT your idiotic per-condition of Sovereign Default.

You Claim to support employer contribution levels FAR LESS than those necessary to support CURRENT pension promises, so are you FOR Reed’s Constitutional Change … or just full of SH** ?

January 26, 2014 at 2:38 am

Dear sensitive fragile man Tough Love, the title of this post is `Veterans lack ‘California rule’ pension protection’, and the first paragraph starts with `President Obama signed a budget bill that cut cost-of-living adjustments in military veteran pensions last month…’

please, please, don’t break down and cry because I point out those FACTS, which contradict your assertion that `.the SUBJECT is non-military Public Sector pensions..”

Delicate tear-prone Tough Love, sure, I support a constitutional amendment to reduce the accrual rate for future service of current workers. That will take a few years to get passed, and then will be litigated, which will then take another decade, and who knows what the outcome will be… 50-50 chance of sticking.

Now don’t whimper Tough Love, Sovereign Default could happen TOMORROW with a vote of the Legislature. What ever a `per-condition’ is (maybe you meant pre-condition)…. I have NEVER argued for a pre-condition of Sovereign Default.

Sovereign Default GETS THE JOB DONE ASAP. Quit your delicate, sensitive, crybaby fantasy that there is some kind of delaying tactic in your mind. You are the delayer.

And BTW, the subject of this blog is NEVER the PRIVATE SECTOR. Go to Pension Tsunami and take up that matter. Don’t break out in tears, Tough Love. This is a blog about California public pensions, but Ed Mendel happened to address military pensions in this post, so that topic is UTTERLY GERMANE here.

PRIVATE SECTOR pensions are not Germane, but I’m not a stickler. Ellen E. Schultz has debunked any argument that private sector pensions are anything but sleazy frauds, in

http://www.retirementheist.com

You never do your homework, but if I point that out, you burst into tears and cry for Mommy, Tough Love.

January 26, 2014 at 5:10 am

spension…..Baloney, you have used the same BS distraction-riddled comments on the 99% of articles that have not mentioned one word about military pensions.

And quoting… “Tough Love, sure, I support a constitutional amendment to reduce the accrual rate for future service of current workers. ”

THANK YOU ….you’ve finally taken you head out of your ass.

January 26, 2014 at 7:55 am

Baloney right back in your delicate little sensitive face, Tough Love. Ed Mendel specifically compared to Military Pensions here. Go cry to Mommy Tough Love.

January 26, 2014 at 5:21 pm

Interesting……

http://www.wnd.com/2014/01/national-epidemic-public-employees-spiking-pensions/

And don’t miss the comments !

January 26, 2014 at 10:40 pm

So–that’s all it takes for those with differing political views to come together and feel smug? Taking something away from someone, because they have something you don’t have? Constitutional protections, no less? Wow!!!!!!!! Guess Forrest Gump had it right when he quoted his mother, “Stupid Is as Stupid Does”.

January 26, 2014 at 11:33 pm

Seesaw, perhaps, instead of saying…” Taking something away from someone, because they have something you don’t have? ”

It should say…” Taking something away from someone, because they have something unjustifiably too great that I do not get, while I am being forced to pay for theirs”? “

January 27, 2014 at 7:48 am

A CalPERS average retirement of $26,000/yr. is something unjustifiably too great? You are not paying for those pensions, TL! You are paying a price for receiving public services, just like you pay for the cost of a shirt at the department store–after all the person running the sewing machine in the sweat shop in China has to make something.

January 27, 2014 at 9:39 am

seesaw, The average pension for very recent full-career Public Sector retirees is close to three times the figure you stated (and far more for safety workers), starts 5-15 years earlier than comparable Private Sector retirees, and includes COLA increases that Private Sector Plans do not get.

With all these differences appropriately factored in, that results in Public Sector pensions with a value at retirement always AT LEAST 2x, MOST OFTEN 3x-4x,and SOMETIMES (for safety workers) 4x-6x greater than those of comparable Private Sector workers retiring at the SAME age with the SAME years of service and the SAME pay.

Your “selected statistic” average in

(1) part timers,

(2) short career workers,

(3) those who retired long ago on much smaller salaries,and

(4) survivorship beneficiaries with 50%-share pensions.

which makes it irrelevant, and I’m sure intentionally misleading … because this has been pointed out to you numerous times before …. yet you continue to repeat it.

So, are you senile, a charlatan, a Public Sector Union mouthpiece, or what ?

January 27, 2014 at 1:35 pm

Stretch it out a little more each time.

The average pension is not “three times” her figure. That’s a little stretch. And its part of the “apples to oranges” public to private comparison. I had a decent state job, and with 37 years service, at age 63, my pension is about HALF the “average full career” retirement. A typical Caltrans maintenance worker would get around $2,600 a month after 30 years. To get the “average” full term pension you refer to, one would have to be in the highest management positions in CalTRANS.

The “average full career” pension is mostly engineers, professionals, upper management, and, perhaps, safety.

The “average” public sector worker does NOT retire “5 -15 years earlier” than the average private sector worker.

AND, the pensions for public sector workers are higher BECAUSE a greater portion of their TOTAL COMPENSATION goes toward benefits than your “comparable private sector worker”.

“Cash pay” is NOT the same, which makes you irrelevant, and I’m sure intentionally misleading … because this has been pointed out to you numerous times before …. yet you continue to repeat it.

January 27, 2014 at 2:09 pm

Josh Rauh:

” Presenters reviewed existing research and provided their own evidence. Essentially everyone who looked at the data found that public sector workers on average have slightly lower salaries. ”

” Even going with our lower number, 15% of pay is larger than the public-private salary differential that are found in the data. That suggests to me that total compensation for an average public sector employee might be somewhat higher than that for a private sector employee whom these studies characterize as having comparable individual and job characteristics. I am, however, skeptical that comparability of individual and job characteristics in the public and private sector has been or really can ever be achieved.”

Key words: “total compensation”

“might” be

“somewhat” higher

“skeptical” that comparability can be achieved

January 27, 2014 at 2:19 pm

Law of logical argument:

Anything is possible if you don’t know what you’re talking about.

January 27, 2014 at 4:19 pm

S Moderation Douglas,

Looks like you’re doing double-time protecting your Public Sector “turf” today.

BS and lies won’t change anything. It’s all going to collapse around you…. just WHEN is not yet clear.

January 27, 2014 at 6:43 pm

Just checking in to make sure you’re paying attention, TL.

Any particular “lie” you’d like to point out?

Is it me or Josh Rauh you disagree with?

January 28, 2014 at 5:17 am

SDouglas, your link is about as significant as your attitude.

January 28, 2014 at 5:18 am

…especially regarding California pensions.

January 28, 2014 at 8:39 pm

SDouglas47 Says,

Lies (or so hard to believe as factually correct that they are likely lies):

(1) You said…”I had a decent state job, and with 37 years service, at age 63, my pension is about HALF the “average full career” retirement.”

Well, with 37 years of service, the ONLY way that could be true is if your pensionable compensation is very low due to being either a part-tme worker or have a VERY VERY low paid job (hard to believe that you would be stuck in such a low-paid position after 37 years of service)

(2) Quoting…”A typical Caltrans maintenance worker would get around $2,600 a month after 30 years.”

A monthly pension of $2,600×12=$31,200 annually. Assuming that after 30 years the pension is 75% of pay, that suggests a final pensionable pay of $41,600….. I don’t believe it (with 30 years seniority).

(3) Quoting…”The “average” public sector worker does NOT retire “5 -15 years earlier” than the average private sector worker. ”

They sure do…. under what rock are you living?

(4) Quoting…. “AND, the pensions for public sector workers are higher BECAUSE a greater portion of their TOTAL COMPENSATION goes toward benefits than your “comparable private sector worker”. ”

Baloney. CASH PAY in the Public and Private Sectors are near equal in most jobs (and Public Sector pay is considerably higher in blue collar jobs such as maintenance). The FAR FAR better pensions and benefits are just layered on top of that.

January 29, 2014 at 12:32 am

“A monthly pension of $2,600×12=$31,200 annually. Assuming that after 30 years the pension is 75% of pay, that suggests a final pensionable pay of $41,600….. I don’t believe it (with 30 years seniority”

…………………

That’s because you’re only willing to believe what fits your own preconceptions. “Seniority” for California maintenance workers means when they hire on, they start at fifteen percent below full pay, they receive five percent after passing a years probation, then two more five percent raises the next two years, if they meet standards. That’s it, no more”seniority” pay.

http://blogs.sacbee.com/the_state_worker/2013/07/what-california-state-workers-earn-operating-engineers.html

Bargaining unit 12 is CalTRANS maintenance.

A CalTRANS Maintenance area superintendent makes about about $70,000 a year, with no overtime. That’s the guy responsible for an area with three to four dozen men and a multimillion dollar budget. He…..MIGHT…. end up with what you call the “average pension for a full career worker”

I made more than a maintenance worker, but (much) less than an area superintendent.

I’m not complaining, just pointing out that those $100,000+ pensions are the exception, not the norm.

Last time I checked, CalPERS listed the average retirement age for non safety workers as 60. As I mentioned before, I believe that average may be skewed downward by part-career workers who might be working now in the private sector but can begin drawing their pension at age 50. (They would not be eligible for retiree health care)

Guess what Gallup says is the average U.S. retirement age?

61. Up from 57 in the early 90s. NOT a five to fifteen year difference.

Cash pay? See the above quote from J Raugh: ” Essentially everyone who looked at the data found that public sector workers on average have slightly lower salaries. ”

According to Biggs and Richwine, I believe “slightly lower” means about 10.1% lower, in the case of California state workers.

….…

Frankly, TL, you’re not worth lying to. But there might be some other readers interested on more balanced information. It’s easy enough to verify most of this stuff.

January 29, 2014 at 7:44 pm

SDouglas47 Says…………..

From a 5/11/11 OCRegister article ….

The full retirement age for workers in the Social Security system is 67, for those born after 1959. And today’s workers expect to retire at age 66, according to a new Gallup poll.

For public workers in California, however, the average retirement age is about 60, according to a recent Legislative Anaylst report. It drops as low as 50, and varies greatly by job.

January 29, 2014 at 9:54 pm

Because a govt employee “can” retire at 50, or 60, doesn’t mean he will. He makes real life decisions almost like regular people. I repeat, in 37 years experience, I have seen very few retire before early to mid sixties. The “average” age (60) listed by CalPERS includes many partial career workers who terminated govt employment years ago and left their pensions vested. They then can begin to draw a pension as early as age 50. This should be evident from the CalPERS statistic that the average length of service for retirees is twenty years. MOST govt employees are NOT full career employees.

http://ing.us/rri/ing-studies/public-employees-in-focus

Expected retirement age for govt employees:

50-59……….………13%. (Safety?)

60-69……………….44%

70+ or “never”……19%

undecided…………25%

mean age………….63.4 (and rising, 41% of public employees have increased their expected retirement age as a result of the financial market decline)

“PUBLIC EMPLOYEES RETIRE FIVE TO FIFTEEN YEARS EARLIER THAN PRIVATE SECTOR EMPLOYEES”

is gross misrepresentation.

In other words, a lie.

January 29, 2014 at 10:50 pm

QuotingSDouglas37…”I repeat, in 37 years experience, I have seen very few retire before early to mid sixties. ”

Who cares what “you’ve seen” ?

January 30, 2014 at 12:30 am

Just trying to help with my personal observations, which seem to be corroborated by empirical evidence.

Except for police and fire, public employees don’t retire much, if any, earlier than private sector,

Public employees CAN begin to draw a pension at 50. The pension usually will be much reduced from “normal” retirement age pension.

SOME public safety workers actually do retire at 50 with a “full” (90%) pension. About as rare as a blue moon.

On average, public workers do NOT retire “5-15 years earlier than comparable Private Sector retirees”

If I’ve told you once, I’ve told you a million times: Don’t exaggerate!!!

January 30, 2014 at 2:11 am

Overall average retirement age of all us workers is now about 64…

http://www.soa.org/News-and-Publications/Newsletters/Pension-Section-News/2012/february/What-Is-The-Average-Retirement-Age-.aspx

That is about the same as the California public sector average retirement age.

January 30, 2014 at 3:24 am

spension… Do you have a credible source for your statement that age 64 ………………. “That is about the same as the California public sector average retirement age.”

January 30, 2014 at 7:30 pm

I’m wrong. A table showing the retirement ages for public retirees in California is in Figure 3 on page 21 of this report:

Click to access pension_proposal_110811.pdf

The average retirement age ranges from 53 (for CHP) to 63 (for UC faculty). State miscellaneous is 60-61.

January 31, 2014 at 5:30 pm

It’s basic deduction. CalPERS says the average age of retirees is 60, and the average length of service is 20 years.

Its not likely that all these people stay home with their parents till age 40, then go get a government job, work 20 years, and retire.

Many of these “retirees” are actually private sector workers who, at some point in their career, worked for some government agency long enough to vest (usually 5 year minimum). They then go BACK into a private sector job and leave their pension invested in CalPERS.

They have the option of withdrawing all their accumulated pension contributions, plus interest, when they terminate, but doing so would mean they lose the “matching” state contributions.

Now, you have a private sector worker turning 50. They have to do the same calculation as in Social Security : Do I start withdrawing a lesser amount now, and lock in lower payments for a longer period, or do I wait for “full retirement age” and draw a larger pension, but give up five or ten years of immediate payments?

Keep in mind two things; this pension will be based on final salary, so, due to inflation, might be much less than the equivalent worker retiring today. And, these “retirees” are not eligible for health benefits.

If you were a public sector miscellaneous employee in the 2% @ 60 formula and you terminated in 1998 with ten years service and a final salary of $2,500 a month, at age 50 you could begin to draw about $270 a month. If you wait till age 55, you would draw about $360, at age 60, $500, and at age 63, the maximum of $600 a month.

(Because the “2% @ 60” formula graduates from 1.092% @ 50 up to a maximum of 2.43% @ 63 and over)

To the extent that these people who terminated before eligible retirement age decide to begin drawing their pensions at 50 or 55, this brings down the “average retirement age” (60) listed by CalPERS. The average retirement age listed by CalPERS might more properly be referred to as the average “pension” age. Except for safety workers, most government employees going directly into retirement do so at about the same age as average private sector workers, basically, mid sixties, and rising.

This brings up another point, for those who like to exploit the dichotomy between “public sector” and “private sector” workers. If the average length of service for public retirees is twenty years, this means MOST retirees spent more time working in the private sector than the public. And this is only for “retirees”. Statistics are hard to find, but if California follows the pattern of other states, more than half the total state workers don’t stay long enough to vest, so they never become retirees.

Ergo, except for “full career” workers with 30 years or more service (this is fewer than 20% of retirees) most government workers are actually not “public sector” at all. They are private sector workers who spent PART of their career in a government job.

“We have met the enemy, and he is us.”

January 31, 2014 at 5:42 pm

Which brings up another ironic concept: the hypothetical retiree in the above example spent ten years earning a government pension, and another thirty five years in the private sector paying taxes………for his own pension, among other things.

“Can’t we all just get along?”……..with ourselves

January 31, 2014 at 11:08 pm

So I guess that hypothetical employee now receives a pension, social security, and lifetime healthcare.

February 1, 2014 at 2:30 am

That particular hypothetical employee receives no healthcare from the state. To qualify for retiree healthcare, a state employee must begin his retirement within 90 days of termination. If he worked for the state from age 20 to 30, he can begin to draw a pension at age 50, but no healthcare. Ever.