A pension reform initiative proposed by San Jose Mayor Chuck Reed and others got a mixed cost analysis last week from the nonpartisan Legislative Analyst’s Office, quickly trumpeted by opponents.

The measure would give state and local governments the option of cutting retirement benefits current workers earn in the future, while preserving benefits already earned through past service.

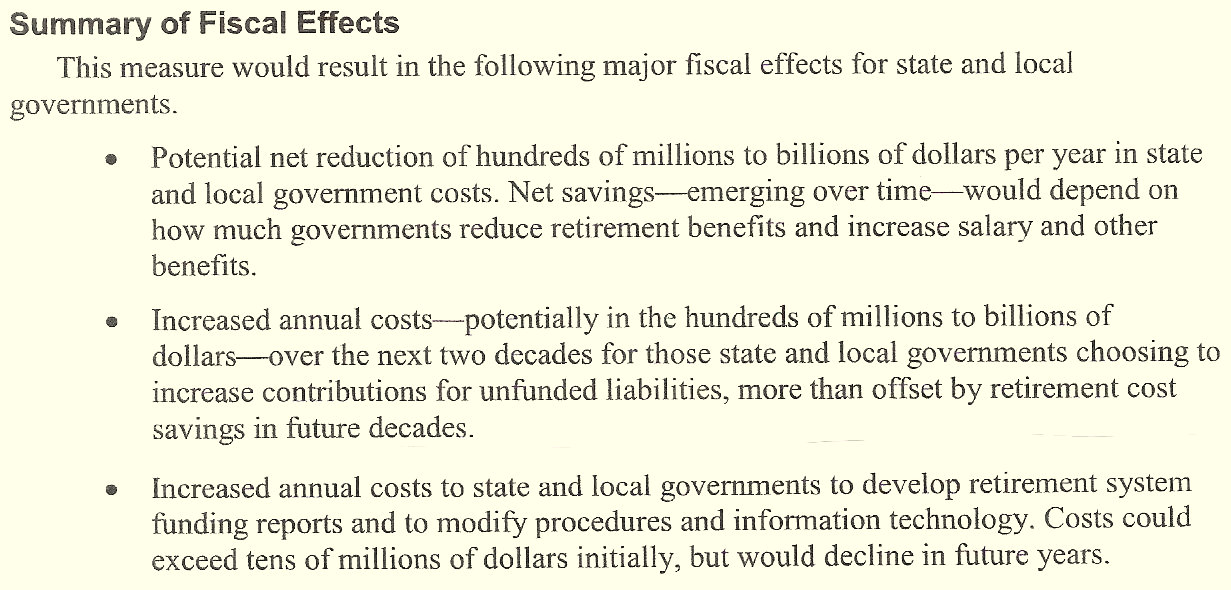

The analyst said this part of the initiative has the potential to reduce “hundreds of millions to billions of dollars per year in state and local government costs,” depending on how much retirement benefits are reduced and salary and other benefits are increased.

A lesser-known part of the initiative aims to strengthen retirement benefits by requiring governments to propose, but not enact, annual plans for fully funding pensions and retiree health care in an unusually short 15 years.

The analyst said annual costs could increase “hundreds of millions to billions” over the next two decades for governments “choosing to increase contributions for unfunded liabilities, more than offset by retirement cost savings in future decades.”

Ironically, the part of the initiative intended to strengthen not cut retirement benefits created an apparent weak spot attacked by the opposition, a coalition of public employee unions.

According to the analyst, said a coalition news release, “San Jose Mayor Chuck Reed’s proposed ballot measure to slash pension benefits for public employees could potentially cost state and local governments ‘billions of dollars.’”

Reed said in a news release that the opponents “fail to acknowledge that the LAO found that these potential increases would be more than offset by the potential savings from the initiative.”

The analysis co-signed by Gov. Brown’s Finance department was sent to state Attorney General Kamala Harris. Her office will write a brief title and summary for the initiative, which is all some voters are believed to read about a measure.

Last year, Dan Pellissier said California Pension Reform suspended an initiative drive “after determining the attorney general’s false and misleading title and summary makes it nearly impossible to pass.”

Reed has said he may poll on voter reaction to the initiative title and summary before deciding whether to proceed with a drive to gather the signatures needed to place the measure on the ballot.

A polling firm hired by the union coalition found that portraying the initiative as “eliminating” public employee pensions “fosters a visceral negative response from voters,” the Sacramento Bee reported last week.

Reed told the Bee the opponents have to “mischaracertize what we are doing.” He said the initiative does not propose “eliminating” public employee pensions. The poll-tested word was used in the coalition news release last week.

“It’s clear from this assessment that this poorly crafted measure will not only add to the retirement crisis in our state by eliminating vested retirement benefits for teachers, nurses, firefighters, school bus drivers and other public employees, but also cost our communities and state billions of dollars,” said Dave Low, chairman of Californians for Retirement Security. “This measure would be a financial disaster for taxpayers and retirees alike.”

LAO summary of pension initiative fiscal effects

Reed and the initiative advocates say if soaring retirement costs are eating up funds needed for basic services and programs, cutting pensions current workers earn in the future can quickly yield sizable savings.

That’s allowed in private-sector pensions and a dozen other states. But in California, courts are said to have ruled that the pension promised at hire becomes a “vested right,” which can’t be cut unless offset by a new benefit of comparable value.

Most attempts to cut retirement costs, including union bargaining and pension reform legislation last year (AB 340), increase employee pension contributions and give new hires lower pensions, yielding savings reformers say are too small and too slow.

In San Diego and San Jose, where retirement costs were taking 20 percent or more of city general funds, voters last year approved measures that, in different ways, attempt to cut pensions current workers earn in the future.

Vested rights were the key issue in a five-day trial last July for several union suits opposing the San Jose pension reform measure. A pending decision by Santa Clara County Superior Court Judge Patricia Lucas is expected to be appealed by the losing side.

If the initiative proposed by Reed and others is placed on the ballot and approved by voters, the California Public Employees Retirement System is likely to launch a legal battle to preserve the current view of pension vested rights.

The initiative, a state constitutional amendment, would give new and current employees vested rights to pensions and retiree health care only for work they have already performed.

If a government employer declares a fiscal emergency, or finds that an underfunded plan is at risk of not being able to pay retirees, the initiative would allow retirement benefits earned after that point to be cut in several ways.

The analyst said a government employer could cut pensions and retiree health care, cut annual inflation adjustments, increase the retirement age, and require employees to pay a larger share of costs.

If the benefits are normally subject to labor bargaining, the employer must try to bargain changes. If negotiations, mediation and fact-finding fail to produce an agreement, the employer can use existing procedure to impose the change.

“In cases where these changes are not within the scope of collective bargaining, the government employer could implement the changes directly,” said the analyst.

The initiative requires government employers with pensions or retiree health care less than 80 percent funded to prepare a plan to reach full funding in 15 years, and then hold public hearings on status reports each year until the plan is fully funded.

Many CalPERS pensions plans are less than 80 percent funded. Much of the retiree health care promised state and local government employees is zero percent funded, pay-as-you-go each year with no money invested to cover future costs.

Moreover, most of the payments being made to reduce the debt or “unfunded liability” for promised pensions and retiree health care are based on reaching full funding in 30 years. Getting there in 15 years would require much larger payments.

So why give initiative opponents an opening to claim the measure could cost governments “billions,” if they choose to try to get to full funding in 15 years?

Reed has said 15 years is an estimate of the time the average worker will remain on the job. Some think retirement benefits should be paid while the worker is on the job, avoiding unfairly passing debt to future generations that did not receive the services.

And though it may not be a strong selling point, there also is the analyst’s view that increased annual costs in the short term would be more than offset by retirement cost savings in future decades.

“To the extent that some government employers increase employer and/or employee contributions in the near term to accelerate payment of pension and retiree health liabilities, those government employers could increase their retirement funds’ assets and investment returns and dramatically reduce the amount of employer contributions needed over the long term,” said the analyst’s report.

Reporter Ed Mendel covered the Capitol in Sacramento for nearly three decades, most recently for the San Diego Union-Tribune. More stories are at Calpensions.com. Posted 23 Dec 13

December 23, 2013 at 2:19 pm

Of course, the Analyst is right, but what did he actually say? The problem with pension financing is that it must be, absolutely has to be viewed over the long haul. You really miss the mark if you try to design your pension system, or the reform of that system around its near-term budgetary costs.

Take CalSTRS, for example. There is no dispute that proper funding of that pension system would require an increase in annual contributions of at least $4.5 billion. So, if some were to propose doing the right thing and funding CalSTRS so that it does not impose horrendous costs on future generations, but instead provides adequate funding today (plus returns over time) to fully cover the retirement costs of today’s working teachers, that person would accurately be described as creating a $4.5 billion annual, additional budgetary cost.

Is that person, therefore, a fiscal spendthrift threatening to ruin the current budget? Or is that person proposing to do the right thing fiscally and prevent many more billions of dollars of harm to future budgets?

Of course, when that person also suggests including reductions in future costs by allowing the Legislature to make adjustments to pensions (maybe increasing retirement ages, slowing COLA’s or some other cost-saving tool), then there are two ways to demonize him. You can call him a budget buster and a teacher hater.

In reality, like it or not, systems like CalSTRS and many local pension plans that are facing massive unfunded liabilities will be experiencing massive budgetary problems no matter what we do. If the reformer seeks to make that process more rational by addressing it sooner and more comprehensively, he is actually doing future retirees, future public services and future tax payers a huge favor.

Back to the LAO’s fiscal summary. Is it wrong? Of course not. But, what does it really mean? It means, if we try to fix our broken pension systems, it’s going to hurt, but if we don’t try to fix them it’s going to hurt even more.

December 23, 2013 at 4:11 pm

Food for thought…………

Assuming we do not call the 401K Plans that Private Sector workers typically get from their employers to be “pensions” (but more accurately “savings Plans”), what is so wrong or bad about ELIMINATING “pensions” (of the Defined Benefit kind) for PUBLIC Sector workers?

Are PUBLIC Sector workers deserving of a MUCH MUCH MUCH better (AND HENCE much much much MORE COSTLY) deal than the Taxpayers that pay their way?

And would the current GROSSLY EXCESSIVE (by ANY reasonable metric) Public Sector “pensions” even exist were it not for the Public Sector Unions’ BUYING of the favorable votes of our (self-interested, voter-selling, contribution-soliciting,Taxpayer-betraying) elected officials with campaign contributions and election support ?

The masses clearly do not understand the MATH behind these pensions, and Reed’s initiative “may” be the last opportunity to save California……..and I say “may”,because to be effective the Future service reductions of all CURRENT workers need to be reduced by at least 50%……and that would STILL leave them considerably greater than the retirement benefits typically granted Private Sector workers by their employers.

December 23, 2013 at 4:20 pm

It is going to cost a lot of money in court costs if it is passed. The best thing to do is to give the Public Pension Reform Act of 2013 time to work, and forget this so-called pension protection act of 2014. With his initiative Reed is not saying, “You now have permission to cut pensions through collective bargaining, if you think you need to or want to”–what this initiative really says is, “You must negotiate the terms of your pensions through collective bargaining, and you do not choose to do take action that is different than the usual–you must develop a plan on how to be fully funded in 15 years or “my” terms will be imposed on you”. This initiative of Chuck Reed’s is pure folly–a wolf in sheep’s clothing, just like Reed himself.

December 23, 2013 at 4:30 pm

The initiative’s accelerated pension funding provisions would reduce overall pension costs to government while requiring that pension compensation be paid by government closer in time to when that compensation is earned, rather than allowing government to push those costs far into the future. A 30 year funding plans means that people not yet born can be made to pay for unpaid pension compensation obligations that exist now. The argument that restraining government’s propensity to steal from the future will cost the present more is both tautological and an attempt to appeal to people to act unethically.

December 23, 2013 at 5:23 pm

Tough Love, there is a good argument for why governmental entities might prefer DB pension plans. Since government does not go away (unlike private firms that come and go) and it is large, it can take a more aggressive approach to investment. That means, in theory (and it has been born out in practice) that they can provide a higher benefit at a lower cost.

The down side of that is what we’re seeing now. The risk is all on the tax payer. And, the decision makers seem to have an incentive to imagine that future costs will be less and returns more so that they can understate the present costs of pensions. You can’t do that with salary, so we’ve had pension benefits promised to ward off salary increases. The chickens then come home to roost.

Your other point, whether government employees are overcompensated is really a separate point. But, the dynamics are similar. When it comes time to determine private sector compensation, the bottom line is considered and balanced against the need to attract and keep good employees. In the public sector the people making those trade offs owe their jobs to the public employee unions.

December 23, 2013 at 5:54 pm

Mike Genest, While you are correct that there are certain advantages to DB vs DC Plans, the investment duration you describe being minor compared to the DB benefits of mortality sharing.

But regardless, the Public Sector Union/Politician “moral hazard” has shown itself to be an overwhelming and insurmountable problem …….the consequences of which FAR outweigh

the benefits of DB Plans.

December 23, 2013 at 8:46 pm

Its all relative, MG. Many political office holders have the millionaires and billionaires to thank for their respective elections. Money is the milk of politics, of course, and it is going to come from somewhere–labor unions are certainly not the one and only source of political capital.

December 23, 2013 at 11:28 pm

Mike Genst:

“decision makers seem to have an incentive to imagine that future costs will be less and returns more so that they can understate the present costs of pensions.”

It is an inherent problem of democracies that politicians will give out what they are unwilling to make those in the present pay for. It doesn’t take the ability to use rosy forecasts for that to happen. Consider your own example of CalStrs: that “there’s no dispute” didn’t mean that the state made its interest payments on the existing unfunded actuarial obligations.

Forcing politicians pay all compensation in the present is the only effective barrier to those who would otherwise shift cost onto future taxpayers who can’t vote on it. You can still have the state manage defined contributions in large shared risk pension funds. People are generally ill-equipped or unwilling to expend the energy to properly manage their own retirements. But the money taxpayers contribute to the retirement of government employees needs to made in the year it’s earned so that there is needed political counter-force to excessive compensation that comes from having to take it from taxpayers in that same year.

December 24, 2013 at 2:04 am

Quoting jskdn Says: … “Forcing politicians pay all compensation in the present is the only effective barrier to those who would otherwise shift cost onto future taxpayers who can’t vote on it. ”

Very Well Sated….and the most direct and effective way to do that is by hard-freezing the DB Pension Plans of ALL CURRENT Public Sector workers (ZERO future growth),and replacing them with DC Plans with a Taxpayer %-of-pay “match” comparable to what Private Sector Taxpayers typically get from their employers … 3-5% of pay.

December 24, 2013 at 4:19 am

The LAO noted there would be excessive costs to reduce unfunded deficits. But it failed to note that reducing deficits will reduce annual contribution rates . It should be a one-for-one.

December 24, 2013 at 7:37 pm

The major flaw in this initiative is only the employer determines if there’s a financial emergency and pensions must be cut. There are no hard criteria, no controls and no 3rd party review. It’s a wide open door for employers to underfund pensions on purpose to trigger an ’emergency’ as a ruse to break pension contracts. At least with BK the employer has to convince a judge that they are really broke.

December 24, 2013 at 8:41 pm

The initiative requires the employers to set up certain reporting procedures that they have not done before–there will be the need for millions of dollars, just to do those reports. What do you mean, no 3rd party review? They cannot just say, “We’re fine” and that be the end of it. They are all going to be required to do these reports to the satisfaction of the new, “wannabe dictator”, Chuck Reed. If this initiative passes, you will see enough money being spent to make your head swim–look at his own City right now–his council budgeted five million dollars to defend its just-passed initiative–and he just lost a decision in court yesterday. So, the appeal will probably use the rest of that five million. A few years ago, Orange County spent eight million dollars trying to take back what it had already given its deputy sheriffs–it lost. Give the Public Pension Reform Act of 2013 time to work.

December 24, 2013 at 11:03 pm

SeeSaw, don’t you mean the BS ……….. “Make Believe We Actually Accomplished Something” ………. act?

December 25, 2013 at 1:29 am

No, I mean just what its title is. Pensions can only be reformed going forward for new hires, not for current employees and not for retirees–in the State of CA. Leave the Collective Bargaining process alone and let the Public Pension Reform Act of 2013 work.

December 25, 2013 at 1:41 am

SeeSaw, Without the new law applying to all CURRENT as well as new workers it’s guaranteed to fail.

Everyone not a charlatan, or an idiot knows that.

Which are you?

December 25, 2013 at 7:22 am

I am a normal human being. CalPERS has existed for 80 years and has never stiffed any retiree who was qualified for benefits. I think there are some pretty smart people involved with CalPERS–investment managers and actuaries who are doing the work and advising the Board. I don’t think CalPERS needs you or your ilk to advise them on what needs to be done to keep the plan solvent. .

The new law could not apply to current workers, because the CA Constitution protects the vested benefits of such. What idiot doesn’t understand that!

December 25, 2013 at 5:18 pm

SeeSaw, The Michigan Constitution protected the pensions and past service pension accruals of active workers too.

How’s that working out for them?

This is a MATH problem from which CA’s cities, countys, “authorities” and likely the entire State cannot escape…..and while it couldn’t have happened w/o sign-off by our self-interested elected officials, a HUGH portion of the “blame” belongs to CalPERS via their outrageous push for the RETROACTIVE pension increases of SB400, and with the Public Sector unions for bribing our elected officials with campaign contributions and election support….and when not bribing them, threatening them if they don’t support their outrageous and unjust demands.

December 26, 2013 at 2:17 am

BS! The retroactivity of the increases was according to how the State Legislature has handled such-type issues for almost 100 years. CalPERS did not invent that practice–it only follows the orders of its members.

December 26, 2013 at 2:23 am

The decision by the judge in Detroit does not affect pensions in CA, TL. Unless you are afraid, you can go to the CalPERS Website, and read the section, CalPERS Responds, and you will be enlightened.

December 26, 2013 at 3:12 am

Quoting SeeSaw….” The retroactivity of the increases was according to how the State Legislature has handled such-type issues for almost 100 years. CalPERS did not invent that practice–it only follows the orders of its members.”

I can’t recall when I have last heard such BS.

And how/where/when exactly did the rights of the Taxpayers, who are told to pay for this enormous RIPOFF, get factored into the decision ?

________________________________________

And only a fool would give credence to a CalPERS opinion that the Detroit Bankruptcy judge’s findings will not apply to it.

December 26, 2013 at 4:26 am

The State Legislature has members who pass laws. The pension retroactivity was allowed by the State Legislature throughout the history of CalPERS. If, as a taxpayer, you don’t like the laws in your state, you work to change your legislators and you work to change the laws you don’t like. That’s what recently happened with the CA Public Pension Reform Act of 2013, The Act was passed due to pressure from the voters; one portion of the Act abolished the retroactivity of future pension upgrades for all public sector workers in CA–new hires and current workers alike.

I would give credence to an opinion put out by CalPERS before I would pay attention to one word you would utter, TL. CalPERS is my bread and butter. When my pension is cut you can laugh–don’t hold your breath waiting, because I predict you would suffocate first.

December 26, 2013 at 5:46 am

Quoting SeeSaw…”The pension retroactivity was allowed by the State Legislature throughout the history of CalPERS.”

Yes, allowed by self-interested vote-selling, contribution-soliciting, Taxpayer-betraying members of the State Legislature.

December 26, 2013 at 6:38 am

To quote a late Senator from New York, TL: “You might own your own opinions, but you don’t own your own facts”.

December 26, 2013 at 7:22 pm

” self-interested vote-selling, contribution-soliciting, Taxpayer-betraying members of the State Legislature”????

The good/or bad thing about politicians is they just don’t stay “bought”. Big Daddy Unruh said

“If you can’t eat their food, drink their booze, screw their women and then vote against them, you have no business being up here.”

AND, if they COULD be bought, public employee unions couldn’t even rent a seat at the table.

” The broadest classification of political donors separates them into business, labor, or ideological interests. Whatever slice you look at, business interests dominate, with an overall advantage over organized labor of about 15-to-1.”

http://www.opensecrets.org/overview/blio.php

“Powerful Public Employee Unions” is an oxymoron.

December 26, 2013 at 8:27 pm

What jskdn calls “stealing from the future” could also be called spreading investment risk over time. Which is one of the major advantages that public sector pension systems have over private.

As M Genest implied, since government “does not go away”, private DB systems necessarily require more stringent controls than do public ones.

That and the mortality risk sharing constitute a big advantage over DC systems.

IF (big “IF”) the DB systems are managed prudently, on both the investment and distribution sides.

That’s what SeeSaw is talking about with Brown’s pension reform and other reforms that have been and are now still being dealt with in collective bargaining. Proper management.

……………………

Does anyone recall President Bush (junior) and company proposing to “privatize” Social Security?

At the time, Rush Limbaugh and others scoffed at the “liberals” opposing the idea.

“They think we American citizens are too dumb to manage our own investments”

“They” may have a good point. I shamelessly cut and paste this from another blog:

“Oh and I love the collective advice that everyone get a personal investment account and try their hand swimming with the sharks, er, managing their own money. The USA has such a can-do attitude! Why don’t we all fix our own cars, cut our own hair, grow our own food, develop our own drugs, teach our own children, and study law to represent our selves in legal cases. It is a ridiculous argument that there will be less risk when individuals are “free” (read: forced) to pursue their own amateur dreams in a world of professionals.”

December 26, 2013 at 11:34 pm

SDouglas47 Says: …..

Hogwash. Want a good example of the outrageous Union tactics,…..watch the 3-rd video down on the right side (at the link below) to hear a Union official threaten a legislator.

http://unionwatch.org/

December 26, 2013 at 11:53 pm

Quoting SDouglas47 Says: … “What jskdn calls “stealing from the future” could also be called spreading investment risk over time. Which is one of the major advantages that public sector pension systems have over private. ”

Baloney. Promised Public Sector pensions should be FULLY (100%) funded (using reasonably conservative assumptions) over the working careers of the covered employees. This prevents FUTURE taxpayers who received no benefits from the services of these employees from having to pay for their pensions.

However, everyone with a self-interested finger in the pot (and a hand in the Taxpayers’ pockets) ….the Unions and our elected officials… collude to materially understate the true cost of the absurdly generous pensions and benefits that have been promised Public Sector workers EVERYWHERE.

The decades-long financial “mugging” of the Taxpayers by the insatiably greedy Public Sector Unions/workers and their bought-off elected officials must end….and for CURRENT, not just new workers.

December 27, 2013 at 1:21 am

TL has OCD Complex–hating unions!

December 27, 2013 at 2:14 am

Someone sounds incredibly naive.

An unnamed “spokesperson”? THINKS she has more power than she does and makes emotional threats. Which are politely and tactfully ignored by the committee.

This is evidence of what?

“Fully funded over the working career” is a specious goal. Much like trying to drive with your gas tank 100% full at all times. Not practical, unless you go to a defined contribution system, and who in his right mind would want that?

December 27, 2013 at 2:16 am

Merry Christmas, SeeSaw.

Keep up the good work.

December 27, 2013 at 3:12 am

Quoting SDouglas47 Says: …“Fully funded over the working career” is a specious goal.”

No, it is the appropriate goal so that the users of an employee’s services pay for those services (INCLUDING the full cost of pensions and benefit promises made to that worker) and not FUTURE taxpayers who did not benefit from that worker’s services.

And doing so has nothing to do with being 100% funded at all times.

December 27, 2013 at 4:29 am

Toughlove, just finish each comment with Bah-HumBug! You’ve given me a good laugh the last couple of days with all you errors and insults. Where’s your buddy? He would chastise you for all your copy-pasting.

December 27, 2013 at 6:12 am

Bah-HumBug Bille……..

Ii will soon be a new year…..may it be filled with much happiness, good health, good fortune,and a hard freeze to Public Sector pensions everywhere.

December 27, 2013 at 4:43 pm

“Much happiness” and “a hard freeze to Public Sector pensions everywhere,” would not be synonymous events! I wonder if you wore your Grinch mask everywhere on the holidays.

December 27, 2013 at 10:58 pm

@SD47:

Your 12/27 2:14 AM comment indicates that you might not understand the actuarial basis for defined benefits. The fueled car is a poor metaphor to understand the financing of a DB pension fund. A more appropriate metaphor would be a credit card account– and we have a balance that we cannot conceivably pay off in any reasonable amount of time under the present circumstances. While 100% funding would be well-nigh impossible every year, a properly-managed fund would bounce above and below that number each year based on investment performance. 100% would be the ideal mean. Instead with Calpers and Calsters what we have are funds that have a mean in the 70s, which means they are systematically underfunded by the participating governments. And why are they systematically underfunded? Because the SB400 retroactive levels of retirement (and the copycats at the local levels trying to compete with the foolhardy state government) were much too high, a known fact that only recently have the two pension funds brought to the attention of our venal politicians. That the senior management of Calpers and Calsters weren’t sacked for this debacle I consider a scandal. Kudos to Chuck Reed to trying to fix this problem outside of bankruptcy court.

@TL:

Thanks to you and the Captain for trying to inject some sense into this blog of just how big these pension debts are.

And thanks to the blog proprietor for running this blog. I would like to think that every newspaper editor and TV/radio news director in the state would be a reader, but I somehow doubt it. They’re apparently too busy keeping up with the Kardashians and other such nonsense instead of noticing the financial tsunami offshore.

December 27, 2013 at 11:42 pm

SeeSAaw, They certainly are synonymous if you are one of the 85% of all workers who are PRIVATE Sector Taxpayers who are now called upon to pay for 80-90% of the total cost of the pensions of PUBLIC Sector workers that are ALWAYS at least 2x greater than theirs, and most often 3x-4x greater in value at retirement.

December 28, 2013 at 7:08 am

Analogies are never complete. A pension system is neither a car nor a credit card. And it doesn’t need to be balanced EVERY YEAR. One of its strengths is that it can spread risk and rewards over economic cycles which can last a half dozen years or more.

Like past years when the state and many local governments took a pension contribution holiday.

As MG said, governments don’t go away. If the next generation pays more for a few years, it could result in reduced costs further out.

“Stealing from our grandchildren” is really a tired postulation.

December 28, 2013 at 7:43 am

My spouse is a private sector taxpayer, TL. And, as his spouse, I share the same taxes. If my spouse and I do not equate our financial responsibilities, for which we are responsible and always pay, as being caused by public pensions, why are pension taxes so hard on you and not on us? No complainer on these blogs has ever given us an actual percentage amount of their own personal taxes that go to pay for public pensions. Why is that? Could it be that when they find our their actual personal cost is so tiny, they are embarrassed to admit such? (It must be just like the Study that was once conducted in response to a taxpayer who complained about his personal responsibility for funding NASA. The results of the Study were that each American’s yearly liability for funding NASA was one-half of one cent.) Since my public pension is larger than my spouses private pension, it looks like I am the one being called upon, since our tax liability is going to take a bigger chunk of my pension than of his.

December 28, 2013 at 12:41 pm

Thank you “Berryessa Chillin’ Says”: for your support……it’s most often a lonely (but necessary) road I travel.

By training and work history I am quite knowledgeable on this subject and am truly only looking for Compensation fairness across both the Public and Private Sectors (NOT to hurt Public Sector workers) and I understand that “fixing” the problem MUST mean that (at least prospectively, for FUTURE Service) Public Sector must accept MUCH smaller pension accruals (as well as MUCH smaller retiree healthcare subsidies).

And I accept that (with their Unions’ approval and encouragement) the legions of Public Sector employee-commentators will continue with the misinformation, distortions, half-truths, omissions, and outright lies to stop and/or delay these VERY MUCH needed Public Sector Pension/Healthcare reforms.

As you seem to know… it’s a MATH problem that will not go away by itself.

December 28, 2013 at 12:53 pm

QuotingSeeSaw…” No complainer on these blogs has ever given us an actual percentage amount of their own personal taxes that go to pay for public pensions. Why is that? ”

Because that’s not the real issue,,.. which is, that with VERY few Public Sector workers earning less in “cash pay” than their Private Sector counterparts, there is ZERO justification for Taxpayer funding of Public Sector pensions and benefits ANY greater than those of their Private Sector counterparts, let alone ones that are MULTIPLES greater in value at retirement, as is ROUTINELY the situation today.

There are FAR FAR better uses for Taxpayer funds than unnecessarily overcompensating Public Sector workers.

December 28, 2013 at 6:53 pm

So, in other words–You would prefer not to have to pay one penny from your own pocket, than to contribute one penny to help thousands of people remain sustainable throughout their non-working elder-lives. You are quite the altruist, TL.

December 28, 2013 at 7:50 pm

Everyone should remember that Tough Love works in the private investment industry. The private investment industry profits greatly from the high fees they charge for managing DC plans like 401(k)’s, IRAs (where all my retirement money is). Of course everyone should do their best to get their DC plans to Vanguard, where fees are low, but I can’t do that until I finally retire. Until then I’m subject to arbitrary and capricious DC plan fees…. in some cases (I’ve documented them in early CalPensions posts) retirees’ DC plan money has been withheld by the private company that holds them, while at the same time huge fees are charged.

DC plans are a den of corruption.

According the Wall Street Journal reporter Ellen Schultz, the US Private sector has been astonishingly corrupt at managing most employees retirement $.

I can’t agree with Tough Love that comparison to the US Private Sector is worth a damn.

I totally agree that the promised benefits by the California public sector pension system are way too high. However, many, many other public sector pension systems in the US are doing ***JUST FINE***.

Never hear Tough Love or the public pension haters address the well-run US public DB plans.

In general those systems promised fewer benefits than California. But any argument that there is a fundamental, systemic flaw in all public DB plans is at odds with the real data and mathematics of the real world; such arguments are what private investment folks like Tough Love make to try to get corrupt and obscene profits off of confused people.

There is no case whatsoever for eliminating all Defined Benefit programs. They work fantastically well in many public cases in the US, and in general, for a given $ contribution, more retirement benefits than the same $ contributed to DC plans.

Many, many panels have verified that take-home pay is somewhat lower in the public sector than in the private sector, when one properly compares equivalent positions. Guys like Tough Love specialize in comparing inequivalent positions, like, public sector prison psychiatrists with advanced degrees to private sector custodians.

What roils guys like Tough Love is that at the low end of the pay scale, like custodians, the public sector overpays compared to the private sector. Then at the high end, like, say, the Governor of California, the pay is way, way, way lower than the equivalent private sector position. Guys like Tough Love believe that the people at the top deserve unlimited compensation.

However, pension benefits are better in the private sector, even outside of California (California is a mess). The total compensation, excluding retirement health, is roughly the same outside of California public versus private.

Retirement health is way, way better in the public sector. However, the real culprit is the crappy US health care system….read the `Bitter Pill’ by Steve Brill. I think we should just let Canada or France or Germany open up shop in California, and expand their sensible health care systems for those who choose to enroll in it. Give the Canadian or France or German health care centers on US soil that country’s legal system. Let single-payer compete here, buttressed by those countries populations…

December 28, 2013 at 8:04 pm

Checkout the Wisconsin, Washington, or North Carolina public pension systems… nearly 100% funded.

December 28, 2013 at 8:09 pm

SeeSaw, It’s quite amazing how you “twisted” my objection to OVER-COMPENSATING Public Sector workers to …”You would prefer not to have to pay one penny from your own pocket, than to contribute one penny to help thousands of people remain sustainable throughout their non-working elder-lives..”

But THAT’s what Publlc Sector pension supports are expert at …”twisting” the facts to support their agenda of maintaining (even for FUTURE service not yet provided) the decades-long ripoff of the Taxpayers.via their grossly excessive, unnecessary and unsustainable pension promises.

December 28, 2013 at 8:14 pm

Spension, For a “factual” discussion of the Public Sector pension ripoff, serious students of the subject should read:

“Plunder: How Public Employee Unions are Raiding Treasuries, Controlling Our Lives and Bankrupting the Nation”

Here is a Published summary of this book:

“Public employees have become the new American elite. In the past, Government workers earned less money but had slightly better job security and benefits than Americans working in the private sector. These days, government workers not only earn more than other Americans, but they have vastly superior benefits, including pension plans that often allow them to retire as early as age 50 with 100 percent or more of their final year’s salary. These pensions often to $100,000 a year and come with cost of living adjustments and free lifetime medical care. Getting a government job and sticking with it is like winning the lottery. This plundering of treasuries, made possible by aggressive union tactics and spineless politicians, results in higher taxes and massive debts that ultimately will be borne by our grandchildren. The current situation is “unsustainable.” The problem goes beyond finances. Government unions protect even the worst public employees from accountability. Schools don’t attempt to fire incompetent teachers-and union protections make it nearly impossible to even fire ones accused of abuse and other misdeeds. As government gets bigger and more powerful, government officials have more uncontrolled power over the rest of us-to enrich and protect themselves at the expense of the public good. The public’s servants have truly become the public’s masters.”

December 28, 2013 at 8:18 pm

QuotingSpension…”Guys like Tough Love specialize in comparing inequivalent positions, like, public sector prison psychiatrists with advanced degrees to private sector custodians.”

To be blunt,……….you’re an idiot.

December 28, 2013 at 10:51 pm

” Because that’s not the real issue,,.. which is, that with VERY few Public Sector workers earning less in “cash pay” than their Private Sector counterparts, …..”

You keep repeating that, TL, but Biggs and Richwine, in a report for the Heritage Foundation, say otherwise.

” The most important variables in the list are state and local government status. After controlling for observable skills and a detailed list of personal characteristics, state workers in California earn about 10.2 percent less in wages than private-sector workers. Local workers see a much smaller, statistically insignificant penalty of 0.6 percent. Combining state and local workers together yields a significant penalty of 3.7 percent (not shown in the table).

http://www.heritage.org/research/reports/2011/03/are-california-public-employees-overpaid

December 29, 2013 at 12:08 am

SDouglas47 Says: ……While I would need to review their study to believe it (as well as compare it to other studies with opposite outcomes), for the sake of discussion,lets assume the 3.7% of “cash pay” Private Sector advantage exists.

On a “Total Compensation” (“cash pay” plus pensions plus benefits), that would still put Public Sector workers FAR FAR ahead of their Private Sector counterparts,….justifying the very material pension/benefit reductions that I advocate for.

That conclusion follows form the fact that while Private Sector workers rarely get more than 3%-5% of Pay towards their retirements (in the form of 401K employer contributions) and ZERO retiree healthcare subsidies (in almost all cases today), the level annual % of pay to fully fund the TYPICAL Public Sector Defined Benefit pension over their working career, ranges from 20-40% of pay for non-safety workers, and 40-60% of pay for safety workers…..and YES,these %’s are correct.

And, given the young ages (50-60) that only Public Sector workers typically retire, the heavily subsidized (and sometimes free…e.g. in NYC) retiree healthcare benefits EASILY add $250K in value to the Public Sector worker’s retirement package above and beyond the very significant pension advantage.

So if it makes you happy, the Taxpayers will gladly subtract their (supposed) 3.7% cash pay advantage from, the HUGE 30-50% of pay pension advantage + the Retiree healthcare $250K advantage currently granted Public Sector workers EVERYWHERE.

December 29, 2013 at 1:37 am

I would suggest that public sector workers do NOT “typically retire” at 50-60. CalPERS lists the average age of retirement for miscellaneous workers as 60, as I recall, and 57 years for safety.

HOWEVER, in my personal experience, I knew very few who retired at less than low to mid 60s. How can this be? Keep in mind that the average length of service is 20 years. Fewer than 20% work 30 years or more. All those that worked long enough to vest, but terminated before retirement age are eligible to begin drawing a pension at age 50, even though they may still be working in a private sector job. These persons are not eligible for retiree medical care UNLESS their termination was within 90 days of retirement age.

So someone who worked for a public agency from age 20 till age 30, for example, then moved to a private sector job, is eligible to begin drawing a pension at age 50 (at a reduced formula, i.e. 1 or 1.25%) or wait until age 60 to get 2%. I understand CalPERS says most choose the earlier date.

This tends to reduce the average “retirement age”, which might more accurately be called “pension age” to 60. I don’t have the exact number of those who terminate before age 50, but if the average service is 20 years, and 80% of workers have fewer than 30 years, there must be a lot of these early terminations.

I never worked much with firefighters, but even most of the police and CHP I knew did not retire until early to mid 60s, in spite of the reported average “pension age” of 57.

Again, for the record, those who receive a “full retirement” (90%) at 50, are one percent, or fewer, of retirees. It is NOT typical.

December 29, 2013 at 2:38 am

Tough Love said, “To be blunt,……….you’re an idiot.”

That is all you got, Tough Love? No way you have mathematics and facts on your side, because the mathematics and facts **FAVOR DB SYSTEMS**, like in Wisconsin, Washington, and North Carolina.

California is a mess, (btw, above, I mistakingly said private pensions are higher than public; that is wrong, it is the other way around).

But your industry is trying to hijack the post-retirement benefits system in the US for its typical disgusting, corrupt ripoffs.

And please compare the deferred compensation of, say, Governor Brown with those of any private CEO in the US who runs a $100-billion/year corporation, if you continue to maintain that the private sector has impoverished post-retirement benefits.

Tough Love, if a fact or a mathematical proof bit you in the posterior, you would think it was a love nip from your dog.

December 29, 2013 at 2:44 am

TL, what written rule is there in the universe that says the total compensation of workers in all similar categories, both public and private should be the same? If a burger joint owner pays his flippers $15 an hour, while the joint down the street pays his flippers $8 an hour, are you going to be the first picket carrier for the $8 worker?

As for DC plans, most government workers have them to go with their DB plans. I personally paid 30% of my gross paycheck to my 457 every two weeks–there was none of that 3% to 5% matching from my government employer. That stuff was for management only–the non-union public workers.

December 29, 2013 at 3:07 am

SDouglas47 Says: Interesting observations as to durations and lengths of Public Sector employment.

Similar employee turnover certainly occurs in the Private Sector (likely at a higher rate since firing incompetents is a LOT easier in the Private Sector, and Private Sector firings are rarely followed by the employee suing the employer to get the job back.

Of course police actually retiring at age 50 is rare, but since many police officers are indeed hired by 25, retirement at 55 cannot be that unusual. Regardless of the exact age age,at retirement, a 90% COLA-adjusted pension valued under REALISTIC assumption for discounting Plan liabilities (consistent with what both GASB and Moody’s are now using) requires a level annual TOTAL contribution just shy of 60% of pay to fully fund (over the working career) a Police officer’s pension who retires after a 30-year career.

Assuming the Officer actually pays say 10% of pay towards his/her pension, that still leaves Taxpayers with a level annual 50% of pay contribution….. roughly12.5 TIMES greater than the typical 3%-5% of pay employer contribution the Private Sector Taxpayers gets from his/her employer.

And while that multiple would be lower (perhaps 5-10 times) for non-safety workers, is remains patently absurd and grossly unfair to Taxpayers for them to be forced to fund such greater pensions for OTHERS when there is little (if any) difference in Public/Private Sector “cash pay” in comparable occupations.(or in occupations with reasonably similar risks, skill sets, educational requirements, and knowledge, if not directly comparable).

December 29, 2013 at 3:09 am

QuotingSpension….”Tough Love said, “To be blunt,……….you’re an idiot.” That is all you got, Tough Love?”

Based on your earlier comment (which I quoted above) that provoked that response,YES, and it was well deserved.

December 29, 2013 at 3:30 am

For anyone curious about how “pension reform” to a hybrid plan works, just look to Rhode Island and Gina Raimondo. Gina was a hedge fund manager who became state treasurer. She championed and fear mongered the public into voting for a hybrid plan. She won’t answer the hard questions about how it is working out, instead she talks about the goals. Goals are noble, but if you are not achieving them, you also have to be noble enough to change course or you are just another snake oil salesman.

Here is the website. Don’t read the numerous Forbes Magazine critiques (yes – even FORBES Magazine) or the union and Rhode Island newspaper critiques, you can simply go to Gina’s own section of the Rhode Island State Government and look at her own track record reported. Wall Street is making out like…well…better than bandits!

http://www.treasury.ri.gov/divisions/finance/pension/expenses.php

in FAQ section on the right, select > “What are the asset manager expenses for the pension system”.

According to Gina in the FAQs…the “asset managers” are paid “Per industry standard, the management expenses for alternatives generally fall between 1.5 percent and 2.5 percent and the performance expenses are generally 20 percent of profits”.

However, if you compare the 2012 and 2013 total investment expense you will notice that $1 billion was placed and $15 million was expensed in 2012. The $1 billion increased by $84 million in 2013 and $45.9 million was expensed. Now even a fool and their money is separated but with some basic math you can easily see that if you made $84 million and were charged $15 million + $45 million, that leaves you with $24 million (ok $23 but I am rounding generously). Which means, that the investment expense was not 20% + 2% +1.5% but 70.58%. Ok, if I am generous and ignore the original $15 million, it is still 53%. I don’t know how Gina does math, but in the real world, it is still 1+1 =2 and $84 -$60 = 24 or 70.58% of the profits.

Taxpayers are not saved any money and the pensioners are giving of COLAs to pay Wall Street who brought us the Great Recession of 2008.

Oh but don’t forget the note at the bottom of the report(s) that states:

* Note: “Fees Paid” column details actual fees incurred, inception through 6/30/2012. Since funds were added to the portfolio at different times throughout the 2012 fiscal year, line items represent partial year expenses over different time frames and are not readily comparable.”

Which means, the fees charged are probably significantly more than 70.58% of the profits.

2013

Click to access Expense-Table-05-22-13-FY12-Actuals.pdf

2012

Click to access Expense-Table-05-22-13-FY12-Actuals.pdf

December 29, 2013 at 4:04 am

BillieSays:,IF(and that’s a BIG if) the fund pulled out higher than agreed-upon expenses, that’s a big problem. Personally, I doubt it as it’s to big a deal to hide,and she knows she is under a microscope.

Why not just ask the Pension administrator for an explanation rather than speculating ?

____________________

Oh…… and wrong. Taxpayers are and will continue to save BIG-TIME via the COLA freeze.

December 29, 2013 at 4:07 am

Quoting Tough Love “QuotingSpension….”Tough Love said, “To be blunt,……….you’re an idiot.” That is all you got, Tough Love?”

Based on your earlier comment (which I quoted above) that provoked that response,YES, and it was well deserved.”

Absolutely false. You have systematically not addressed the serious studies that try to compare apples with apples on salaries.

You are non-mathematically, biased, and incapable of serious reasoning… all your comments are bought and paid for by the corrupt (Boesky, Goldman-Sachs, Madoff etc run) private investment sector.

December 29, 2013 at 4:12 am

SeeSaw

TL is tilting at windmills. Equal compensation is a fool’s errand.

You can’t even get that WITHIN state government. In California, a state electrician in Modesto or Redding earns a little less than a union electrician. In San Francisco, L A, or San Diego, they make about 50% less than private.

A state heavy equipment mechanic in the Bay Area makes 5% more (retention differential) than the equivalent state position in the valley.

Two guys/gals working side by side. Same exact job. Same seniority. If one is single and the other is married with children. The family man could be making $800 more per month (health insurance) than the single man. Is that fair? Even more so, for years I got NO health insurance from the state (I was on my wife’s employer insurance). Equal pay?

It would be impractical to determine relevant benchmarks for public jobs. Compared to what? Generally larger companies can and do pay better for the SAME type of work than a small business can pay. And private sector salaries can increase or decrease much more quickly than public contracts can change.

Studies aren’t much help. Some say public compensation is “roughly equal” even including the cost of benefits. Biggs and Richwine say California state workers make 10% less in salary but “as much as” 30% more when benefits are included. “Benefits” include a 15% “value” of job security.

I believe M Genest produced a study saying roughly the same thing. But then, I also understand, when discussing his own pay and retirement, he was quoted as saying

“We could have made a lot more money in the private sector. We are making more money.”

“Equal pay” is a chimera.

December 29, 2013 at 4:41 am

Quoting SDouglas47Says: …”TL is tilting at windmills. Equal compensation is a fool’s errand. ”

That’s an amusing statement,coming from a Public Sector worker and Public Sector Union member………..

The Public Sector Unions have raised to an “art-form” the chasing of the most minute compensation advantage that can be found in and copied from another city’s employment contracts……..the old “me-too”/”piggyback” demands.

———————————————

And quoting…”“Benefits” include a 15% “value” of job security. ”

I suggest you ask a few of the1.5 million Private Sector unemployed about to run out of extended Federal unemployment insurance benefits what “value” they would assign to the very high job security afforded virtually all Public Sector workers.

December 29, 2013 at 6:06 am

http://thinkprogress.org/economy/2012/05/08/480438/unemployment-without-government-cuts/

……..

In their paper, Biggs and Richwine base their 15% job security benefit on the data that private industry has a 20% turnover rate while the rate is only 6% for public employees.

In their salary and benefit calculations, they compare, for several reasons, public workers to private sector workers in large companies (500 or more).

Guess

What

The

Turnover

Rate

Is

For

Large

Companies?

Determining or agreeing on “equal compensation” is like nailing jello to a tree.

December 29, 2013 at 6:10 am

Sixty thousand factories closed during the Bush Administration TL and Wall Street caused the whole word to collapse financially. Nobody feels worse about those 26,000,000 left without jobs than I–because I care–not that I was responsible for all that outsourcing off our shores.. And don’t be so snobbish about who those jobless ones are–many of those unemployed workers are from the public sector–oh yes–bet you didn’t think about that did you. If you care about those unemployed, have you sent a message to your rep asking that another extension be put forth tomorrow morning. Oh, I bet you have!

December 29, 2013 at 7:01 am

SeeSaw,…..f you “care” so much for the Private Sector unemployed, show it, by freeing up funds to support their needs by permanently giving up the portion of your pension granted RETROACTIVELY (for PAST service service) for which you contributed absolutely NOTHING.

Oh, but when it hits “home”, and you really have to put up or shut up, what are you going to put up …….besides empty words?

December 29, 2013 at 7:07 am

SeeSaw,

I mentioned before that there really is no distinct line between the public and private sector.

The average length of service for Calpers retirees is twenty years. That math seems to indicate that MOST retirees spent more than half their working careers in the private sector. Fewer than twenty percent of public workers spend more than thirty years there.

And that doesn’t include all the public sector workers who will never draw a pension, either because they didn’t work long enough to vest or because they decided to withdraw their contributions on termination to roll them into an IRA.

I’ve seen quite a few moving back and forth between the sectors depending on economic conditions or personal career goals.

If you look at an unemployed person, can you really say he’s an unemployed public sector worker or unemployed private sector?

And I know some “retired” public sector workers who get more from Social Security than they do from PERS. Because they worked ten years for some local government when they were in their twenties.

I think we all need to step back and take a deep breath. Start looking for common ground and commonsense solutions and stop the witch hunt.

December 29, 2013 at 7:53 am

S Moderation Douglas Says: ,……Your LAST sentence is a good start, and to expand upon that thought, the COMMON GROUND your seek should be EQUAL, but not greater Public Sector Total Compensation.(Cash Pay plus pensions plus benefits) in reasonably comparable jobs.

And no matter how you slice it, with Cash Pay being quite close (one way or the other) but FAR FAR greater Public Sector Pensions and Benefits, the first step in that path is very material pension and benefit reductions for the future service of all CURRENT Public Sector workers.

December 29, 2013 at 3:10 pm

Oh My Goodness!

Grow Up!

The Heritage Foundation says SOME public sector workers MAY be overcompensated by as much as 30%.

MAY BE

They say: ” In the case of California public employees, wages are slightly lower in the public sector. Initially, benefits appear only slightly higher, implying rough parity in compensation between the public and private sectors. ”

But “properly accounting” for retiree health and pension plans generates a premium of 15%.

BUT, in properly accounting, they ASSUME:

” most state and local employees have roughly 25 years of service at retirement and retire in their mid-50s”

To which I say “bunk”.

But mainly, if you look at their study, you will find that when they “properly evaluate” health and pension costs, they are talking about the VALUE of the benefit to the employee, not the COST to the taxpayer.

Health benefits, for example. If an employee had to buy an individual plan it would cost 25% more than the state pays for equivalent group coverage. This is added value to the employee, but not added cost to the tax payer.

Similarly with pension benefits. They say the defined benefit has a greater VALUE than a DC plan, but they do not claim that it costs the taxpayer more.

There IS “rough parity” in total compensation costs between public and private sectors.

December 29, 2013 at 8:10 pm

Quoting S Moderation Douglas Says: ….

“BUT, in properly accounting, they ASSUME: ” most state and local employees have roughly 25 years of service at retirement and retire in their mid-50s”. To which I say “bunk”. ”

And of course we should just believe (not them), but YOU, clearly one with a bias…right ?

____________________________________________

And quoting…”But mainly, if you look at their study, you will find that when they “properly evaluate” health and pension costs, they are talking about the VALUE of the benefit to the employee, not the COST to the taxpayer. ”

Well, if you were properly educated in accounting/economics, you would realize that that the “VALUE” of what’s promised, not what a gov’t entity chooses to “pay” in a given year towards the TRUE COST of the promise,is the CORRECT approach and real “cost” (even if deferred to future years).

December 29, 2013 at 10:32 pm

Good thing YOU’RE not biased.

LOL

It’s Sunday, you’ve been at it for days now. You have my blessing to take the rest of the year off

December 29, 2013 at 11:04 pm

SDouglas47 Says:

Your new year’s resolution should be to stop BS-ing the readers, admit that your Promised pension is grossly excessive and unsustainable, and if still working, AGREE to a 50% reduction in the pension accrual rate for future service…..noting that it would STILL be better than even the most generous Private Sector pensions.

And if you are already retired, you’d be wise to advocate for such cuts from those still working, because the fate of your accrued pension benefits is on the line as well.

Happy new year.

December 30, 2013 at 4:10 am

Tough Love said… “..noting that it would STILL be better than even the most generous Private Sector pensions.”

Wow, greater than the $100 million post-employment packages (with the highest over $400 million) given in the Private Sector….

http://abcnews.go.com/blogs/business/2012/01/golden-parachutes-21-ceos-landed-100m-plus/

Too bad Tough Love is so innumerate he can’t tell the difference between trillion, billion, million, and thousand.

December 30, 2013 at 5:15 am

Spension,

Anyone with a brain understands that my statement meant that it is STILL better than the best Private Sector pension “Formula and Provision combination”, NOT better than the single largest Private pension than can be found. HUGE Defined Benefit Pensions in the Private Sector exist BECAUSE the Pensionable Compensation is huge, not because the Plan is a richer formula.

You’re still an idiot, and the more you say the clearer it becomes.

December 30, 2013 at 4:18 pm

Tough Love,

Anyone with a brain reads the words you wrote, that SDouglas47’s Promised pension is “STILL be better than even the most generous Private Sector pensions.”

The most generous private sector pension was had a value of over $400 million.

If you meant something else, you should write what you mean. If you didn’t mean what you wrote, you should apologize and correct yourself.

But in your world, the world of Madoff, Boesky, Enron, Goldman-Sachs, JP Morgan, etc, there is no right and wrong, no apologies for unethical behavior, just pure power. And anyone who points out the gross immorality of your world is called (by you) and idiot.

December 30, 2013 at 6:44 pm

Spension, As I said earlier…… you’re an idiot.

Each additional comment from you just reinforces that.

December 30, 2013 at 7:01 pm

Spension,

I knew what he meant. I just don’t agree with him.

For one thing, I have a mother in law living on a private sector pension from her deceased husband. And another relative living on his own pension from IBEW. They are both retired quite comfortably, and they are not CEOs.

For another, I have read TLs posts for several years. He seems to be fond of doing math and showing his work, but using some of the most extreme examples. Like those in the $100,000 pension club (about 3% of retirees) and safety retires who “retire at 50 with 90% of pay” (about 1% of retirees.)

He also seems to DOUBLE COUNT retirement benefits for public sector workers.

Biggs and Richwine in the Heritage Foundation study concede to MOST other studies that

” the wage penalty and benefit premium for state-local workers either cancel out or tilt in favor of private workers.”

They diverge, however, in the value of health and pension benefits.

TL constantly argues that public sector workers earn as much as their private sector counterparts…PLUS…a pension that is 2 to 3 times the pension of the “average” (non CEO) private sector worker. (Or up to seven times, if I read correctly, in the case of some safety workers.)

I agree, public sector pensions are 2 or 3 times greater than most private retirements, but I say the COST of those pensions is INCLUDED in the “roughly equal total compensation”.

Basically, to quote Girard Miller, (and ToughLove), “interest follows principal”. I agree. But, unlike TL, I say it is MY principal, once my employer contributes it to MY pension system, as one facet of MY total compensation.

For your daily dose of vitriol, check the LA Times recent opinion piece on pensions. (” When it comes to pensions, California is no Detroit”). I haven’t seen TLs name yet, but there seem to be a LOT of commenters who are convinced that MOST public sector workers retire at 50 with 90% of pay, and other modern urban myths.

My new year’s resolution will be to continue to debunk those myths where I see them, with logic and verifiable facts.

December 30, 2013 at 8:32 pm

Good job Douglas!

December 30, 2013 at 9:02 pm

Tough Love, as you continually show, you respond to facts, logic, and mathematics with personal smears… that is all you have, you have insufficient intelligence to do anything else.

December 30, 2013 at 9:06 pm

SDouglas47, actually, I think in California insufficient contributions were made to cover the pension promises. The volatility of securities markets and the consequences were underestimated in the projections used for the 1999 benefits increases, etc.

Of course DB pensions are by nature more economical and stable than DC plans, when correctly managed.

December 30, 2013 at 10:32 pm

Quoting SDouglas47 Says: …. “He (TL) also seems to DOUBLE COUNT retirement benefits for public sector workers. ”

If you feel I’m Double counting retirement benefits, please sate where and.I’ll either agree, or explain my statement if I disagree with you.

————————————————————–

And you’re correct that (in a comment to a different post) I a gave a long mathematical demonstration that the Taxpayer paid-for share of the 3%@50 pension of a CA Police officer is 4-5 times greater in value at retirement than that of the TYPICAL Private Sector worker retiring at the SAME pay, with the SAME years of service, and with the SAME age at retirement.

But where you are wrong, is by dismissing that as irrelevant because police officers get the best pensions. And specifically, you are wrong BECAUSE Public Sector non-safety worker pensions are generally 2/3-3/4 as generous as those of Police officers, and since pension costs are proportional to the generosity of the formulas & provisions, instead of non-safety pension being 4-5 times greater in value, then they are 2/3 to 3/4 of that multiple, meaning that they are (using the mid-points if these ranges) 3-3.25 times greater than those of their Private Sector counterparts.

And as we’ve discussed before, with little difference in Public/Private Sector cash pay, there is no justification for ANY greater Public Sector pensions let alone ones that are 3+ times greater for non-Safety workers and 4-5 times greater for safety workers.

December 30, 2013 at 11:43 pm

Technically, I guess, insufficient contributions were made at both the state and local level.

When some people complain that we are stealing from our grandchildren to pay for employee expenses today, I must point out that 10 to 12 years ago, government contributions were near zero, so those taxpayers reaped the benefit of the long term leveling effect of a DB system.

Benefits for employees can be relatively stable, and the cost to taxpayers smoothed out over years (and economic cycles).

But whose fault is it if sufficient contributions are not made? Since the 1990s, I believe, CalPERS has had plenary authority. They unilaterally determine the rate and the state and local governments MUST ante up. At the start of the century, CalPERS was fully funded and determined most governments required very low, or NO contributions.

1. Even though governments had these “pension holidays”, normal deductions were still withheld from most employees.

2. The 2012 pension reform dictates there will be NO MORE pension holidays.

3. In the last round of contracts several years ago. Those greedy union “thugs” (sarcasm) negotiated pension contributions increases of 3% to 5% for most state employees. Maybe larger increases for safety workers, I’m not sure. Oddly, instead of CalPERS using these higher contributions to offset the unfunded liabilities, they REDUCED the employer (AKA “taxpayer”) contribution by an equal amount. This saved the taxpayer billions of dollars in the short term, but didn’t do anything to reduce unfunded liability.

CalSTRS doesn’t have the same authority CalPERS does to demand contributions, but they have been making similar bargaining concessions to ease the pension problems.

December 30, 2013 at 11:52 pm

T Lovey— you debate like a cowardly child with the off remarks and then have the tumarity to ask/pose civil questions like you’re an adult? Do you expect ANYone to take you seriouisly?

December 31, 2013 at 12:05 am

In the words of Rodney King, can’t we all just get along?

December 31, 2013 at 12:53 am

Quoting Ed Towner Says: ……. “T Lovey — you debate like a cowardly child with the off remarks and then have the tumarity to ask/pose civil questions like you’re an adult? Do you expect ANYone to take you seriously?.”

So please, tell me why anyone (without an agenda) reading this blog should take seriously the comments of Current or Retired Public Sector workers (such as yourself) sucking excessively on the Taxpayer’s teat, and wanting to continue doing so for as long as possible?

December 31, 2013 at 1:06 am

YOU say there is “little difference in Public/Private Sector cash pay, ”

I say there is little difference in “total compensation” and pension costs are part of the total.

A typical state worker has about 20% (long term average) of his total compensation diverted to pension investments. A typical private sector worker might have 6 to 10% diverted. (401(k) with employer matching).

I wonder which one would have two to three times greater pension???

The private sector has a smaller retirement but more money to spend while working. The public sector worker has less take home pay to spend while working, but a better retirement.

Ironically, the public sector worker individually has NO CHOICE. It is a forced saving. If the private sector worker chooses, he can divert an extra 10 to 15% of his TOTAL compensation and have a retirement as good as the public sector (well, almost as good. There are still those inherent DB advantages).

If you count that public sectors pension CONTRIBUTIONS while he is working, forget about his pension. It doesn’t matter if $10,000 or $100,000. Its already accounted for.

December 31, 2013 at 1:09 am

SDouglas47 Says: Interesting points, but your focus is on the lack of consistent employer “funding”, which of course means the funding of the Promised pensions.

I see a lot of comments like that in many articles. What they all seem to miss is that the ROOT CAUSE of the problem (WAY before the issue of “funding” arises) is that the promised pensions are simple excessive (by ALL reasonable metrics) … and multiples greater than their Private Sector counterparts, as I commented upon above.

Just as there was ZERO justification in the first instance in granting such excessive pensions (often RETROACTIVELY, which was nothing but a theft of taxpayer wealth), there is certainly no justification (for TAXPAYERS) to fully fund an unjust and excessive “promise”.

December 31, 2013 at 1:10 am

Mike, this is kiddy court. Check out the “discussion” in LA Times latest pension column.

Good thing I have a thick skin.

December 31, 2013 at 1:33 am

Tough Love said:`…. meaning that they are (using the mid-points if these ranges) 3-3.25 times greater than those of their Private Sector counterparts.

The actual numbers are not 3-3.25, but 1.26-1.78.

See page 24 of http://www.fixpensionsfirst.com/docs/Full_Report.pdf .

Private pension value (including DC,DB,SS)… about $470,000

at age 62.

Public pension values… ranges from $590,000 (for CalSTRS) to $840,000 (for Local non-safety).

Not a factor of two. At most local non-safety exceeds private by a factor of 1.78. CalSTRS by only a factor of 1.26.

Tough Love is simply incapable of doing math; he feebly responds by simply calling people names. His best move is to just stop posting; every inaccurate post he makes just proves he is not quite as capable as Popo the Clown.

SDouglas47… somehow CalPERS simply didn’t get their formulas right. My best guess is that their internal actuaries screamed bloody murder prior to the holidays and the benefits increases, but were hoisted by the petard of the illusory `110% funded’, which was based on a flawed calculation. The actuaries knew the funded ratio has huge errors on it (BTW, the low funded ratios aren’t much better, but that is not a cause for relaxing) but higher decision making levels are so innumerate they have no clue or basis for understanding the actuaries’ concern.

December 31, 2013 at 2:13 am

On second thought, Mike, you have a good point.

I think I will get along.

Happy New Year

December 31, 2013 at 3:34 am

Quoting SDouglas47 Says: ….. “A typical state worker has about 20% (long term average) of his total compensation diverted to pension investments. A typical private sector worker might have 6 to 10% diverted. (401(k) with employer matching). I wonder which one would have two to three times greater pension???”

Let analyze that and I’ll point out the flaw…

Yes, I agree that the combined Private Sector employer/employee contributions to 401K Plans are likely in the 6-10% of pay range you noted.

But now lets look at your claimed 20% of pay total employer/employee for the Public Sector worker. For the sake of argument let split the 20% into a likely reasonable 5-10% employee contribution and a 10-15% Employer (meaning Taxpayer) contribution. Ok so far?

Now here’s the flaw…..YES, most gov’t Plan sponsors likely “CONTRIBUTE” 10-15% of pay (on average) into the pension Plans of their workers, but that’s FAR less that the contribution necessary (using reasonable assumptions for discounting Plan liabilities… consistent with what Moody’s and GASB now use) to fully fund the promised pension benefits over the working careers of the employees. The correct amount (i.e.,,the real true cost of these very generous promised pensions) is likely double that for non-safety workers and triple it for safety workers.

There is no free lunch. VERY generous pensions are VERY costly to “PROPERLY” fund. If you underfund the promises you have made today, they will come back and bite you later. Up until recently, while many Public Sector workers realized that their Plans were not properly “funded”,few cared, relying on past history of pension payments having always been made in full and on time, and on Constitutional, Statutory, and Case Law that seemed to provide iron-clad protection that they would always get what has been promised…no matter how absurdly generous, excessive, unnecessary and unjust to Taxpayers (who have historically been called upon to pay for shortfalls)

Well, unless you are a Trust fund baby (in which case your pension is not a primary source of your income in retirement), I’d suggest saving mightily outside your pension (just like all Private Sector workers must do to have even a MODEST retirement). I wouldn’t count on your full promised pensions to be there long-term.

December 31, 2013 at 6:17 am

Unfortunately, Tough Love, your exaggerations concerning the cost of public pensions are contradicted by serious studies, like that by Fix Pensions First.

And the private sector has been so corrupt in managing its pension system (as documented by the Wall Street Journal reporter Ellen Schultz) any comparison to private sector pensions is invalid.

So, once again, you have proven you are ridiculous, Tough Love.

December 31, 2013 at 8:52 am

“spension Says: Unfortunately, Tough Love, your exaggerations concerning the cost of public pensions are contradicted by serious studies, like that by Fix Pensions First.

And the private sector has been so corrupt in managing its pension system (as documented by the Wall Street Journal reporter Ellen Schultz) any comparison to private sector pensions is invalid.

So, once again, you have proven you are ridiculous, Tough Love.”

– Grow up Spension. This Blog is about California pensions for public employee union members. If you can justify the 90-100 percent pensions yourself and CalPERS are claiming are warranted you can probably justify anything. If you need 60-70 percent of working income during retirement, as most financial experts claim (and that’s for people that retire in their 60’s – as opposed to the BS 50-55 retirement age for Public Employee Union Members) why are taxpayers paying for 90 – 100 percent of replacement income in the form of pensions?

And now we know that paying for these outrageous pensions is costing THREE TIMES what we were told. Is it a bait & switch scheme being perpetrated against California Taxpayers or is it just corruption? I’m going with corruption!

CalPERS is a BIG part of the PROBLEM. CalPERS IS CORRUPT!

December 31, 2013 at 2:34 pm

Spension, You weren’t able to identify even one single error in my mathematical demonstration that the CA Police Officer’s pension is 4-5 times greater than that of a comparably paid Private Sector worker, yet you still spew this BS.

Your protests as to the true Public Sector “advantage” makes it eminently clear you or a family member is benefiting from a continuation of the Public Sector pension/benefit ripoff.

January 1, 2014 at 6:02 am

Tough Love wrote… “Spension, You weren’t able to identify even one single error in my mathematical demonstration that the CA Police Officer’s pension is 4-5 times greater than that of a comparably paid Private Sector worker, yet you still spew this BS.”

Show me a Private Sector worker who is a sworn officer and then let’s do the comparison. However, mathematically, the number of such people is zero, so I have demonstrated mathematically that your comparison is an absurdity.

Tough Love wrote… “Your protests as to the true Public Sector “advantage” makes it eminently clear you or a family member is benefiting from a continuation of the Public Sector pension/benefit ripoff.”

What `advantage’? My point is that non-safety non-healthcare California public employees post retirement benefits exceed comparable private benefits by a factor that ranges from 1.26 to 1.78, not a factor of 3 to 3.25 as you claim. The serious study by an anti-public-pension group, Fix Pension Firsts, is my source. You have nothing but handwaving and shadow puppets as your source, Tough Love.

That DB plans are more economical than DC plans is freshman mathematics: reduction of the longevity risk is the principal mathematical term. But also keeping your industry’s (and the likes of Boesky, Madoff, Enron, Milken, Goldman-Sachs, etc) paws off the money to the maximum extent possible is also a very important efficiencies.

You are merely reduced to asserting I have some financial interest in a public pension. That is false.

On the other hand, you clearly have a financial interest in getting rid of DB plans, as you have said earlier. You should preface every post you make here with the disclaimer `My industry will make money if we destroy all public pension systems’.

BTW, the DB pension systems in Wisconsin, Washington, and North Carolina are doing just fine.

January 1, 2014 at 6:07 am