New government accounting rules will more than double the pension debt reported by CalSTRS, boosting an “unfunded liability” that is now about $71 billion to a newly calculated “Net Pension Liability” of $166.9 billion.

The CalSTRS board was told last week that it’s unclear whether the new liability figure will be reported by the state or spread among school districts, where more than doubling current debt might lower credit ratings and drive up borrowing costs.

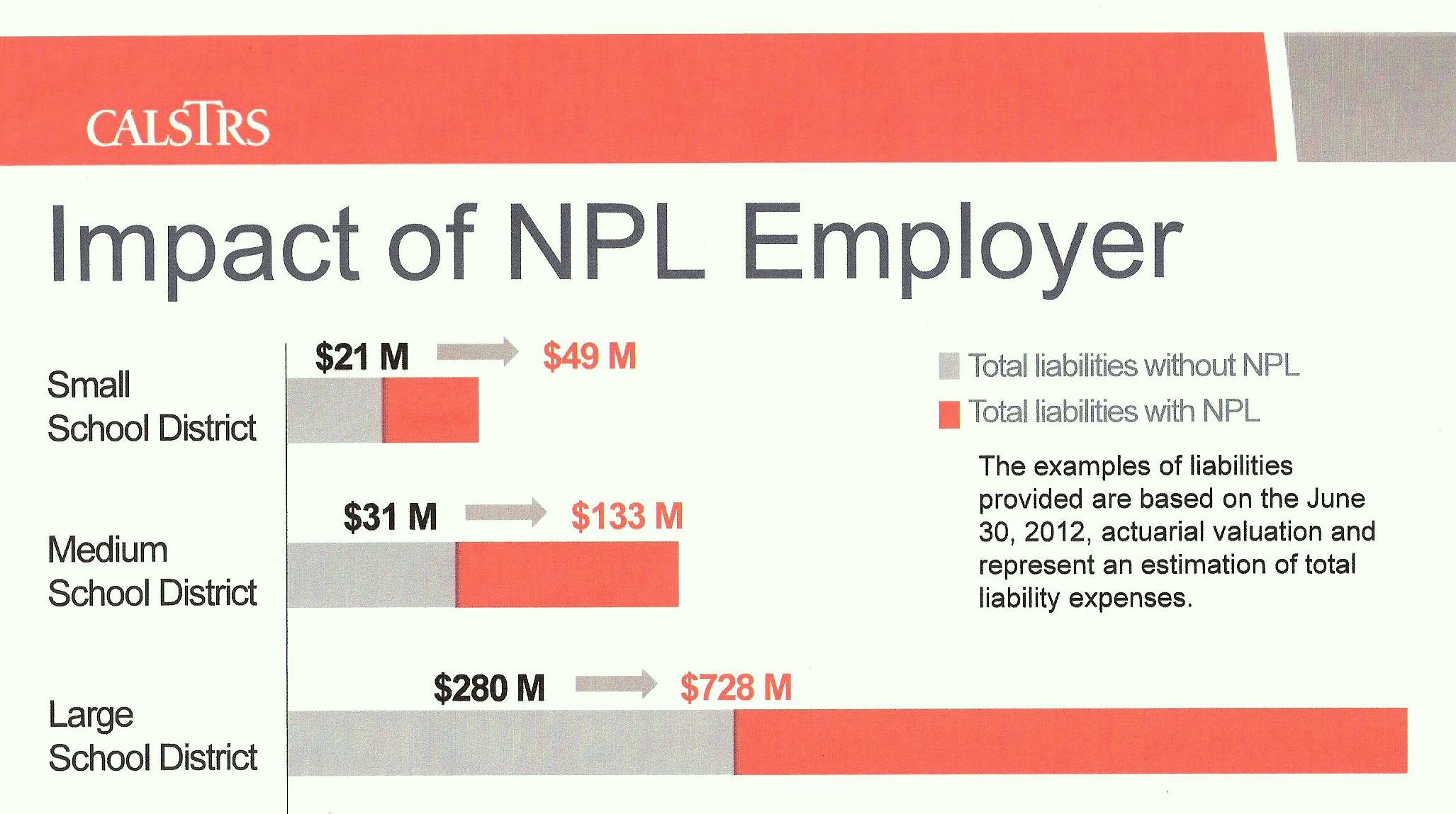

If the “Net Pension Liability” is distributed among employers, the reported total debt of a typical small-enrollment school district might jump from $21 million to $49 million and the debt of a typical large district from $280 million to $728 million.

Neither the state nor the school districts have been including CalSTRS debt in their financial statements. The new accounting rules call for pension debt to be added to employer balance sheets.

“This Net Pension Liability is a hot potato,” Robert Yetman, a CalSTRS financial adviser told the board. “Nobody wants to be the one holding on to it.”

The new Governmental Accounting Standards Board rules, requiring a lower earnings forecast for some pension debt, take effect for CalSTRS financial reports this fiscal year and for the financial reports of employers next year, fiscal 2014-15.

The new rules are a “blended” solution to the controversy over whether the forecasts of investment earnings, often expected to provide about two-thirds of the money needed to pay future pensions, are too optimistic and conceal massive debt.

The usual earnings forecast (7.5 percent for CalSTRS) can be used to project assets needed to pay future pension obligations. But if the assets fall short, a lower bond-based forecast (the cost of borrowing) must be used for the remainder of the obligation.

The California State Teachers Retirement System, which has been seeking legislation for a rate increase for a half dozen years, is projected to run out of money in about 30 years and must “crossover” to the lower earnings forecast, 4.85 percent in one example.

While the new rules show a big CalSTRS debt change, most public pension systems, unlike CalSTRS, can set annual rates paid by employers, allowing them to project enough assets to reduce or avoid the switch to a lower earnings forecast.

A better match with the new GASB rules was one reason cited as the California Public Employees Retirement System, with the goal of full funding in 30 years, approved an employer rate increase in April of roughly 50 percent over the next seven years.

“We expect around the country, at least when you are looking at the larger state systems, most systems will not use a blended rate,” the CalSTRS actuary, Rick Reed, told the board. “They will in fact use a long-term rate.”

How new Net Pension Liability would boost school district debt

A decade ago new GASB rules directed government employers to begin calculating and reporting the debt for retiree health care promised current workers in the future.

The revelation of big debt for retiree health care (estimated to be $64 billion for current state workers over the next year 30 years) prompted some government employers (not the state) to begin pension-like “prefunding” of promised future retiree health care.

The new GASB pension rules are intended to make debt more visible and to aid comparisons among pension funds. In addition to the “net pension liability,” the rules add a new “pension expense” calculation to promptly show annual changes in finances.

But the new accounting rules do not change how retirement systems are funded or managed. The pension systems will continue to use their own actuarial methods to set contribution rates and project future pension obligations.

Another way that CalSTRS is unusual, apart from lacking rate-setting power, is that a non-employer, the state, contributes to the pension fund. School districts contribute 8.25 percent of pay, teachers 8 percent of pay and the state about 5 percent of pay.

“It is important to note the state of California does not currently recognize a liability on its financial statements for the California State Teachers Retirement System,” a CalSTRS fact sheet said.

“GASB has not provided clear guidance for these types of circumstances, therefore it is not clear whether the state or individual districts would disclose CalSTRS NPL (Net Pension Liability).”

Who will decide: the Legislature, the governor, the state auditor? CalSTRS officials said they do not know. But the issue was raised during the long rulemaking process with GASB, which apparently expects the state to solve the problem.

A staff presentation to the CalSTRS board last week showed the main figures if the NPL is reported by the state: Net Pension Liability $166.9 billion, pension expense $12.9 billion, deferred outflow of resources $8.6 billion, and deferred inflow none.

The NPL in the example is based on the main defined benefit pension plan as of June 30 last year. An actual updated NPL would include the much smaller defined benefit supplement and cash balance plans.

To show what happens if the school districts report the NPL the staff gave the 1,700 employers a piece of the NPL based on their percentage of total contributions to CalSTRS. The NPL share was added to the bond and other debt listed by the districts.

Examples (see graph) illustrating the scale of the increase: The total debt of a typical small-enrollment district increased from $21 million to $49 million, a medium district $31 million to $133 million, and a large district $280 million to $728 million.

“To the extent there is a large liability or deferred responsibility, that can have an impact on rating for debt,” the CalSTRS chief financial officer, Robin Madsen, told the board. “We have seen that, in some cases, in write-ups that are coming out in the last three to six months.”

Given the uncertainty, could there be a standoff: Both the state and the school districts simply ignoring the NPL, saying if asked that it’s the other’s responsibility to put the big new debt number on their balance sheets?

GASB is a non-governmental organization with no regulatory power. A CalSTRS board member asked about the “leeway” if a school district decides not to show any of the NPL in its financial statements.

“I think that’s up to them and their auditor in terms of their view or interpretation of their responsibility related to their liability,” Madsen said.

A CalSTRS rate increase would reduce the NPL. As of June 30 last year, CalSTRS was 67 percent funded, had a $71 billion unfunded liability and needed an annual contribution increase of $4.5 billion to project full funding in 30 years.

A $4.5 billion CalSTRS rate increase that would nearly double the total annual contribution from school districts, teachers and the state (about $5.7 billion last fiscal year) is unlikely. The state is still trying to restore deep cuts in school funding and other programs made during the recession.

After a legislative hearing in March, some hoped a smaller rate increase might be phased in over several years — not to reach full funding in 30 years, like the CalPERS rate increase, but to extend the date at which the CalSTRS fund is projected to run out of money beyond 30 years.

When the Legislature adjourned for the year last week, once again there had been no action on a CalSTRS funding solution.

Reporter Ed Mendel covered the Capitol in Sacramento for nearly three decades, most recently for the San Diego Union-Tribune. More stories are at Calpensions.com. Posted 16 Sep 13

September 16, 2013 at 11:57 am

Perhaps the NPL should be allocated by the current level of contributions: school districts 8.5/21.5 or 39.5% employees 8/21.5% or 37.2% and the state at 5/21.5% or 23.3%

September 16, 2013 at 2:29 pm

Quoting … ““This Net Pension Liability is a hot potato,” Robert Yetman, a CalSTRS financial adviser told the board. “Nobody wants to be the one holding on to it.””

YUP, reality is tough, ESPECIALLY if your goal in life is to provide excessive pensions to Public Sector workers, and this throws a wrench into it ….. by showing that the true cost of of those pensions is a LOT higher than what you’ve been saying for many years.

September 16, 2013 at 5:06 pm

Amazing! What a bunch of hocus POKE-US. With the creative accounting all government controlled funds do, its a wonder that CalSTERS isn’t posting a loss every year. CalSTERS’ CAFR is a pure work of fiction. Promote and scream losses and hide assets and profits.

Under the CAFR, “Business-Type Activities” may also be listed as “Non-Governmental Activities” or similar language. This represents government acting in the capacity of a corporation offering a “service” to the people, but not as “taxpayers”. Instead, this is a business that earns money, and the taxpayers are instead “customers” of government.

In fact, Government accounting – it is the most complicated structure of obfuscation ever encountered. Berny Madoff would even be proud…

We need not understand the whole financial report to understand the crime of omission happening in their CAFR. Under the LIABILITIES section, we see a line item titled “NONCURRENT LIABILITIES”. For it can easily slip past your cognition if you aren’t ultra aware of what you are reading. In this case, CalSTERS has just listed its current assets and compared those assets to its future liabilities.

Why is this significant?

Well, imagine if you were reporting your own assets and liabilities to the IRS after it informed you that it required this information for an audit. And let’s say you wanted to play a creative accounting trick on the IRS to hide your real current asset holdings. While this little trick would actually be illegal for you to do, in government it’s perfectly OK and legal, and even promoted in standards of practice. After all, government wont punish itself for its own lies – for the lie is the basic foundation of government accounting as recommended by itself!!!

And there it is… Perhaps you still don’t see it, and that’s OK. For most people have hope and faith that government has integrity and honesty even within its own required Federal and State accounting principals. Perhaps you have even heard your mayor, council members, and even your governor talk about their “intent” to do right by the people? But in reality, nothing could be farther from the truth. We are all just customers of Government in their profit machine. Why else would they all be incorporated and have a DUNS number?

September 19, 2013 at 4:02 am

So if I understand this correctly, this “new accounting method” makes “mark to market” look like a good idea. By the way, last time we had m2m the Great Depression resulted. In 2007, we decided m2m needed a second chance. That wasn’t good enough. We now need to make pensions look too expensive to have.

Use this mortgage calculator below to see how much home you could qualify to purchase if you had to use the same accounting method and had no other debt except the home you were purchasing. Enter the cost of the home, then add all the PMI, Interest, and tax payments you would make for 30 years of the loan and see if you can get a bank to qualify you.

In the example of a home purchase price of $300,000 and $20,000 down, you would need to qualify to purchase a $650,000 + home under this type of accounting.

In fact, you would have to report $350,000 in liabilities on the asset/income/liability verification document even though you hadn’t incurred those liabilities until you are given the loan.

One could easily make the argument that building/repaving roads is far to expensive to have or do. Bridges? Forget it. Insurance Companies? Too expensive to have!

See what you qualify for under this “new” accounting procedure.

http://www.mortgagecalculator.org/

September 20, 2013 at 12:44 am

Billie, Sounds like you’re riding the Public Sector Pension gravy train and don’t want it derailed..

You certainly don’t understand finance.

September 20, 2013 at 7:10 am

Wow! So what does the unfunded liability of the US military look like, under these same accounting rules? Another public sector gravy train, or SHADDUP IT’S UNPATRIOTIC TO QUESTION THE MILITARY?

September 20, 2013 at 10:51 pm

I think that audited financial statements with unfunded pension liabilities ought to be forced to put an “Alpa date” in the results. That date would be the estimated date at which the invested fund will run out of invested funds and the pensioners will need to switch to Alpa dog food to survive. The percentage funded ratio or billions of shortfall we currently use don’t seem to make much of a public impact. IMHO using Alpa dates will help Joe Sixpack understand how precarious some of these pensions are.

September 20, 2013 at 10:52 pm

Oh, I’m not a dog person. My son reminds me that it’s “Alpo,” not “Alpa.”

September 21, 2013 at 4:23 pm

If insurance companies had to account for “unfunded liabilities” in the same way for every car/home/life policy there would be no profits or bonuses or commissions to pay let alone salaries.

And ToughLove, you sound like an angry uninformed person who lost their 401k because the “free market” needed a bailout.

September 24, 2013 at 12:59 am

Responding to “Billie Says”, You are in serious need of a class in basis finance, and FYI the reporting and “reserving” requirements of the insurance industry are so much stronger than the (complete lack of honest) reporting and reserving requirements in the Public Sector, that they are on a different level completely. Ever hear of Sarbanes-Oxley ?

And no, I was quite fortunate in the financial crash of 2008-2009.

I strongly advocate for Public Sector pension REFORM (meaning very material reductions in the pension accrual rate for the FUTURE service of all CURRENT Public Sector workers) and the near elimination of all retiree healthcare subsidies ………. because (with essentially EQUAL “cash pay” in the Public/Private Sectors) there is simply no justification for the FAR greater Public Sector pensions and MUCH better benefits, 80-90-% on the Taxpayers’ dime.

September 26, 2013 at 5:17 pm

This is a great article. The accounting industry has been changing every year and a lot of new rules have been set in place. The big 4 are starting to dominate the markets. Fortunately, there are programs and services that are helpful towards small accounting firms.

October 24, 2013 at 2:24 am

Toughlove,

I’m glad to see you agree with my comments on 9/19 and 9/21. You have not refuted my statements only tried to tell me I am not “learned” enough and that the insurance industry has high standards. That and $5 will get you a cup of coffee.

Funny you mention the insurance industry reserve standards. Why I have never heard of the industry players throwing up their hands and asking for a bailout or looking for ways to not pay claims due to fire, flood, hurricane or earthquake and chalking it up to a difference of opinion. Aren’t they supposed to plan for those things they insure? Start with AIG and work way through the rest of the alphabet.