A new state law drawing national attention could give most of the estimated 6.3 million California workers with no employer retirement plan an “automatic IRA,” a paycheck deduction that goes into tax-deferred investments.

Retirement savings would get a big boost, some experts say, if a small part of pay, perhaps 3 percent, is diverted before workers face the hard choice between daily spending pressures and providing for the future.

Social Security falls short. Nearly two-thirds of California private-sector workers have no employer retirement plan, and nearly half of all workers are on track to retire with “serious economic hardship,” said a UC Berkeley labor center study.

The new plan puts the payroll deduction into tax-deferred investments with a guaranteed minimum return, backed by insurance. The state and the employer have no liability.

Employers of five or more workers must offer the automatic IRA or an alternative retirement plan. An employer would not be required to contribute to the plan, and workers can opt out.

That’s an ideal version of the plan Sen. Kevin De Leon, D-Los Angeles, pushed through the Legislature after years of trying. The bill Gov. Brown signed last September, SB 1234, is only the first step toward a final plan.

De Leon wants to raise $1 million for a required market analysis to design a workable self-sustaining plan. Federal approval is needed on tax and labor issues. Then comes final legislative approval, giving opponents another shot at the plan.

The new law gave the program a seven-member board, including the state treasure, controller and finance director. In an apparent lack of urgency if not enthusiasm, the governor, senate and assembly have not yet made their appointments.

Sen. Kevin De Leon

The view that many Americans are headed for a much lower standard of living in retirement, or hardship and reliance on the government safety net, is reflected in President Obama’s federal budget proposals for an automatic IRA, ignored or rejected by Congress.

De Leon’s bill is attracting attention as an innovative state attempt to create an automatic IRA. His office said a similar bill has been introduced in Maryland and inquiries have come from New York, Wisconsin, Oregon, Washington and Illinois.

Appearing at national forums, De Leon has discussed his California Secure Choice Retirement Savings Program at meetings of the National Institute on Retirement Security and the Center for American Progress.

“The findings of this market analysis and resulting program design will serve as a blueprint for other states to implement similar savings programs,” De Leon said in a fund-raising prospectus.

This month National Public Radio and Atlantic magazine had stories about De Leon‘s plan. In March a lengthy story about the bill appeared in Roll Call, a Capitol Hill publication in Washington, D.C.

“De Leon’s measure, the first of its kind in the country, has attracted attention from lawmakers in other states and in Congress and has turned the first-term senator into a rising star,” said the Roll Call story.

One of the originators of the automatic IRA concept, David John of the conservative Heritage Foundation, told a congressional committee last year that the proposal has bipartisan support.

“This is not a partisan or ideological proposal,” said John. “In 2008, the automatic IRA won the endorsement of both the Obama and McCain campaigns, and it has continued to enjoy support from all sides of the ideological spectrum.”

John said the automatic IRA concept he developed with Mark Iwry of the Brookings Institution was influenced by the “stunningly good” results of automatic payroll deductions for employer-sponsored 401(k) individual investment plans.

In the California Legislature, however, there was a partisan split. De Leon’s bill got little or no Republican support. Some Democrats welcomed the shift of focus from reducing public employee pensions to boosting private-sector retirement plans.

Opposition listed on a legislative analysis of the bill came from employer, insurer, financial planner and taxpayer groups. Support came from public and private-sector unions and retirement groups.

Some opposition arguments: A state-run plan replaces a free market for retirement services. The state and employers will be liable for losses or shortfalls under federal law. The state has mismanaged other retirement plans, public pensions, and is deep in debt.

Insuring a minimum investment return is likely to be too costly. Administrative costs may be higher than expected. Employers will be burdened with distributing forms, answering questions, collecting opt-out forms and transferring contributions.

While opponents are not persuaded an automatic IRA is workable or needed, advocates can point to a number of studies showing that, without change, many Americans will have a sharply lower standard of living during retirement.

Social Security is said on average to replace about 40 percent of working income, well short of the 65 to 85 percent experts say is needed to avoid a drop in the standard of living after retirement, a Congressional committee report said last year.

A labor-backed group pushing for a Social Security supplement asked for a study by the Center for Retirement Research at Boston College that found a $6.6 trillion shortfall in what American households need to maintain their standard of living.

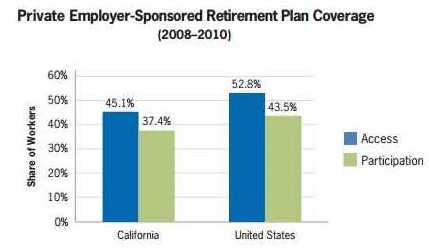

In California, three-year data from 2008 to 2010 shows that 45 percent of workers age 25 to 64 are offered an employer-sponsored retirement plan and only 37 percent participate, the UC Berkeley Center for Labor Research and Education said last year.

“An earlier study found that nearly half (47 percent) of California workers — public and private — are currently on track to retire with incomes below 200 percent of federal poverty level (i.e., about $22,000 a year), a widely accepted threshold for serious economic hardship,” said the UC Berkeley Center research brief issued last June.

The legislation De Leon pushed through the Legislature requires a market analysis to show that the plan is workable and self-sustaining. But state funds can’t be used for the analysis.

De Leon’s prospectus said the program board should be established by late spring of this year. The board will ask for proposals for a marketing analysis, with the goal of awarding a contract by end of the year for completion by the middle of next year.

“To adequately fund all of the components of the market analysis, program design and feasibility study, the goal is to raise $1,000,000 by fall 2013,” said the prospectus. “To reach this goal, a broad spectrum of sources including foundations, nonprofits, labor organizations and private sector businesses are being asked to contribute.”

Graph from UC Berkeley Center for Labor Research and Education brief

Reporter Ed Mendel covered the Capitol in Sacramento for nearly three decades, most recently for the San Diego Union-Tribune. More stories are at https://calpensions.com/ Posted 28 May 13

May 28, 2013 at 5:22 pm

While the idea is a good one, clearly it s being pushed by the Public Sector Unions to distract from (and lessen the justified pressure to REDUCE) the grossly excessive Taxpayer-funded pensions promised Public Sector workers ….. TYPICALLY 2, 4, (even 5-6 times fore Safety workers) greater in value at retirement than those granted comparable Private Sector workers.

The REAL & IMMEDIATE need is to reduce Public Sector pensions for CURRENT workers or service will continue to spiral downward while taxes continue to rise.

May 28, 2013 at 7:32 pm

Just cam here to see Tough Love’s humorous post of the day: “TYPICALLY…..5-6 times fore (sic) Safety workers.” It is really a million-billion times bigger.

May 28, 2013 at 8:07 pm

Well, financial planners oppose it, so that must mean this automatic IRA is a good thing. The financial planning industry siphons billions in fees from the standard DC business:

http://www.pbs.org/wgbh/pages/frontline/retirement-gamble/

Of course for this California automatic IRA to work, the guaranteed return can never be allowed to rise to high.

Tough Love said:`Taxpayer-funded pensions promised Public Sector workers ….. TYPICALLY 2, 4, (even 5-6 times fore Safety workers) greater in value at retirement than those granted comparable Private Sector workers.”

The actual numbers are not 2-4, but 1.26-1.78. Yes, safety are higher, but the private sector safety guys one compares to are minimum wage guys in renta-uniforms.

See page 24 of http://www.fixpensionsfirst.com/docs/Full_Report.pdf .

Private pension value (including DC,DB,SS)… about $470,000

at age 62.

Public pension values… ranges from $590,000 (for CalSTRS) to $840,000 (for Local non-safety).

Not a factor of two. At most local non-safety exceeds private by a factor of 1.78. CalSTRS by only a factor of 1.26.

May 28, 2013 at 8:22 pm

In general what is being proposed is a good idea. However, I do not think that the rate of return should be guaranteed or that an insuance company “guanteed investment contract” (GIC) should be the sole investment option.

While the proposed approach would be great news for the insurance company that is used to provide the GIC investment, doing so provides one or more insurance companies with mandatory GIC sales with no true competition for those investment dollars. Also, what happens if the insurance company(ies) chosen is uanble to meet the GIC promise – then the state is on the hook for the full amount of the guaranteed benefiit.

Instead, like current IRA products and most private 401(k) Plans, the participant’s benefit should equal the account balance, so that the plan sponsor (state) is not on the hook for meeting a guaranteed investment return rate. A diversified investment portfolio that takes into consideration the employee/participant’s age should be used, along with additional investment options at the participant’s election. To determine what investments are to be provided and to do onging due diligence regarding the continued appropriateness of the investments, a committee with the fiduciary duty to act in the best interest of participants should be assembled and monitored.

The primary goal should be to get employees to save for retirement by provinding them with an efficient retirement vehicle that is managed for their benefit and that requires little effort on the part of the employee or their employer, without placing unnessary risk upon the state.

May 28, 2013 at 11:18 pm

Well, TL is consistent. It doesn’t matter what the situation is–private sector retirement plans having nothing to do with the public sector, or the price of oranges–the blame always lies with the Public Sector unions.

May 29, 2013 at 2:42 am

Quoting SeeSaw…”It doesn’t matter what the situation is–private sector retirement plans having nothing to do with the public sector, or the price of oranges–the blame always lies with the Public Sector unions.”

SeeSaw, It won’t matter ONLY when “Total Compensation” (cash pay plus pensions plus benefits) in the Public Sector no longer exceeds that of comparable Private Sector jobs.

And YES, due to the Union/Politician collusion, we have a LONG way to go.

May 29, 2013 at 4:10 pm

Let’s see… Governor of California makes about $166,000 a year in salary, maybe double that with health insurance and pension.

Here are 21 comparable Private sector golden parachutes that top $100 million…

Click to access GMI_GoldenParachutes_012012.pdf

May 29, 2013 at 8:02 pm

Dear Guess Who Says,

I dug up this comment (just below) I put together years ago … very little has changed. But you’re correct, it was a bit short of the 5-6 times, coming in at only 4.55 times greater. Enjoy !

Even if you take (the now rare) Private sector worker who still has the old style (ala what Civil Servants have) Defined Benefit Pension, the “formula benefits” NEVER EVER approaches the Richness of what Police & Fireman get. The REAL costs are well hidden in the “details” as I will demonstrate ……..

A 30 year Private career worker just “might” get a pension annuity of 40-50% of base pay, with NO Post-retirement COLAs, and, if they retire at 55 (vs the more standard 60-65), a 25% “actuarial reduction” in benefits for starting to collect at this earlier age. Also, overtime is NEVER included in pensionable salary in the Private Sector.

So lets work up a comparison for a California Policeman or Fireman (with base salary of $100,000, $50,000 of overtime, 30 years on the job and now retiring at age 55, with a 3%x30 years = 90% of final pay pension), vs the Private Sector worker.

The Private sector worker gets a life annuity (with NO COLAs) of (we’ll use the higher 50% figure) 50% of $100,000 = $50,000 reduced to .75x$50,000 = $37,500 due to actuarial reduction associated with payment beginning at age 55. Using an actuarial table of Life Annuity factors, the Present Value (think of this as the up front money it would take to buy this payout annuity from an insurance company) is approximately $37,500 X 14.24 =$534,000. That’s it, there is nothing else.

The Policeman/Fireman get a life annuity (WITH COLA, the incremental cost of which we will address later) of 90% of ($100,000+$50,000 overtime) = $135,000 annually. With NO post-retirement COLAs, a similar calculation for the Policeman/ Fireman yields (noting that there is no reduction for payment beginning at age 55) $135,000 x 14.24 = $1,922,400.

So, so far (were aren’t done yet) the “Cost” of the Civil Servant’s pension is $1,922,400 vs $534,000 for the Private sector worker MAKING THE SAME PAY.

Now lets address the value of the COLA. The mathematics is quite complicated, but a life annuity of $135,000 to a 55 year old WITH post-retirement COLAs (with an assumed inflation adjustment of 3% per year) is roughly equal to a NON-CLOA life annuity of $169,800. Therefore, on a apples-to-apples comparison with the Private Sector worker (whose pension is NOT inflation adjusted via a COLA) the upfront cost of the Policeman/Fireman’s pension is $169,800 x 14.24 = $2,427,952 (since the 14.24 Life Annuity factor is applicable to a non-COLA-adjusted pension payout)

We aren’t done yet …… since we haven’t considered the ENORMOUS cost of (free or VERY heavily subsidized) RETIREE healthcare afforded to the Policeman/Fireman, but RARELY the Private Sector worker. This cost for someone age 55 (10 years before being eligible for Medicare) is truly HUGH. Rough estimates (with 8-10% inflation in medical costs) for Family coverage typically put this cost at approximately $500,000 (more if subsidized coverage continues post-Medicare age).

So far we have (for the SAME PAY)…..

COST of the Private Workers Retirement benefits = $534,000

Cost of the Policeman/Fireman’s Retirement benefits = $2,427,952 + $500,000 = $2,927,952.

In fairness, Policeman/Fireman contribute a percentage of pay toward their pension (but not retiree healthcare). I could work up an estimate based on assumed year-by-year pay over a career, but for brevity (and since I’m tired of writing), lets assume the accumulated value of these contributions at retirement is $500,000.

We are STILL left with a TAXPAYER FUNDED $2,927,952-$500,000 = $2,427,952 “cost” for the Public Servant vs a $534,000 EMPLOYER FUNDED “cost” for the Private Sector worker …… BOTH with the SAME PAY.

Another way to look at this is that TAXPAYER’S are FORCED to pay $2,427,952/$534,000 = 4.55 TIMES as much as the typical Private Sector employer is willing to pay in retirement benefits……… or alternatively …… TAXPAYERS are FORCED (via their TAXES) to provide a pension to Policeman/Fireman EQUAL IN VALUE (i.e., “cost”) to a Private Sector worker making 4.55 TIMES as much pay.

Isn’t it time for a change ?

May 30, 2013 at 12:01 am

Sure, TL, you can cull/cherrypick the data to pick a high public sector pension (Police and Fire) to the average private sector DB.

Actually, my comparison of 21 private sector golden parachutes >$100,000,000 to the California Governor is far more fair than what you did.

The Fix Pensions First people tried hard to compare apples with apples, unlike you. Their methodology wipes you out.

I have no doubt that I can find private sector security workers (say, at Blackwater or other firms) who make far more than the Police and Fire you compare to, and Blackwater functions primarily on the taxpayer’s dime, on no-bid cost+ contracts. I have no idea what a fair private industry average of comparable fire/police compensation amounts to.

Yes, I certainly think that public sector safety is overcompensated. But anyone who wants to change that has to do a better job of politicking than the safety unions do. Did you notice in the recent dustups over collective bargaining by pulblic employes (Wisconsin, etc) police and fire maintained their collective bargaining rights?

Wailing and whining will get you nowhere, TL. The safety workers unions wipe you out in working our political system.

The only industry better at working our political system is the private sector… Wall Street gets $24 trillion bailouts, local private sector businesses get all kinds of perks like restrictive zoning and licensing to suppress competition.

May 30, 2013 at 2:56 am

Spension ..Your anger seems to have risen a notch or two. Worried that YOUR (or a family member’s) Public Sector pension might go south ?

Your comparison to Private Sector billionaires is meaningless … and nothing but an intentional distraction form the issue at hand … the grossly excessive pensions of CURRENT PUBLIC Sector workers.

Instead of saying something “wipes me out”, be SPECIFIC… tell me …. what did I say or demonstrate that is not accurate?

Sure Police Pensions are one of the highest. So what’s wrong with pointing out the absurd Taxpayer-funded generosity of these pensions and calling for a justifiably reduction?

And our course the Police Unions are good at organizing and politicking. But their many tool is bribing our elected officials, Taxpayers need to raise a fuss (perhaps at the federal level) and get a few of these bribe-accepting officials prosecuted. And yes, I know it’s a long shot.

May 30, 2013 at 1:02 pm

Specifically, you picked a case of a high pension in the public sector with an average one in the private sector.

That is called cherrypicking the data to make your point.

Private sector retirement benefits of executives *greatly* exceed the comps in the public sector.

And as for bribing elected officials, the private sector is second to no-one.

May 30, 2013 at 3:38 pm

Spension, Actually the Private pension I used in that comparison … wherein the worker’s pension formula benefit was 50% after 30 years ( i.e., 1.67% of pay per year of service) might have been typical of the MORE GENEROUS Private Sector DB Plans 20+ years ago, it would indeed be a rarity today, with most of the FEW remaining Private Sector DB Plans having reduced the formula accrual rate for future service years ago, In fact, accrual of any Private Sector DB benefits today even for long time workers is very unusual, most Plans having been frozen over the past 20 years,

The upshot is that I compared ONE Police officer’s pension (granted one of the best in the Public Sector) not to an “average” Private Sector pension, but to one of the richest still out there. The ratio of the AVERAGE Police officer’s retirement package to that of the AVERAGE pension of equally paid Private Sector workers would be greater than the 4.55 TIMES I demonstrated in my above comment.

If you do the SAME type of workup for other categories of Public Sector workers (other than for judges for which it it often even higher), while the relationship is lower, it most often fall between 2-4 times greater for the Public Sector worker. There is simply ZERO justification for this or even ANY greater Public Sector Pensions & Benefits with … as is the case today …. Public Sector workers earning no less in “cash pay” than their Private Sector counterparts.

Your harping in the multimillion $ payouts to a few Corporate CEOs is … again… both ridiculous in this discussion and your attempt to distract the reader from the urgent need to MATERIALLY (by 50+%) reduce the FUTURE Service pension accrual rate for CURRENT Public Sector workers..

May 30, 2013 at 7:41 pm

Poor Tough Love. He must have been fired or wasn’t capable of getting a Public Sector job. I’m really enjoying my Public Safety retirement. Please get a real job so you wont be spending so much time on here. Then you can also contribute to my cost of living raises.

May 30, 2013 at 7:52 pm

But Fix Pensions First made a concerted effort (documented carefully) to compare apples to apples. You pull two cases out of a hat and then jabber about how you are doing something reasonable. Your methodology is laughable compared to theirs. You don’t deserve to shine their shoes, but you don’t have any clean rags in the first place.

The right number is 1.26-1.78 for *pensions* (not 2-4). Now health care in retirement gives a big bonus for public employees relative to private, but that is a different matter, because the crappy US health care system (highest in cost, maybe 50-100th in world performance) is the core issue there.

That is not multimillion for 21 corporate CEOs, but multi-**HUNDRED**-million. Get numerate, Tough Love. Their jobs are absolutely positively fairly comparable to Governors, Vice Presidents, and Presidents.

And those examples are totally pertinent, because the greed in the private sector is used as a justification for the greed in the public sector. If 21 private sector CEOs get away with it (through lobbying and bribery) then 50,000 public employees argue they should do just the same darned thing (through lobbying and bribery).

Never hear you comment on all the graft and corruption and manipulation of the legislative process in the US ***BY THE PRIVATE SECTOR*** Tough Love. You only complain about the public sector.

And don’t tell me the private sector is meritocratic. They survive on cost+ no bid contracts gotten by influence, from the taxpayer’s dime.

May 31, 2013 at 12:00 am

Spension, You state ..”Your methodology is laughable “.

You stop “jabbering” and I challenge you to SHOW ME what in my detailed example is not accurate.

And by the way, MANY times I have agreed with you the greed is rampant in the Corporate Sector, but I can CHOOSE not to use the services of companies whose prices reflect that greed and shop elsewhere. I can’t do so with public Services.

Ed Ring in a Unionwatch web-post said it best …

“Public employees work for an entity that funds its operations not by selling competitively priced products to willing buyers, but by assessing taxes that must be paid under threat of imprisonment. And public employees are managed by elected officials, not business owners, elected officials whose campaigns – especially at the state and local level – are funded by public employee unions. Unionized government workers demand wage and benefit increases from bosses they elected, paid for by government entities that don’t have to earn a profit but can simply take money from other citizens.”

Source: http://unionwatch.org/reforming-public-sector-unions-and-public-sector-pensions-is-not-anti-worker/

May 31, 2013 at 12:15 pm

Tough Love, your example is not a broad apples-to-apples comparison, which the Fix Pensions First study is.

You picked a high public pension and compared it to the private industry averages.

You know exactly what you are doing… you know that the 21 private sector CEOs who get >$100 million post-employment payouts are not a representative sample of the private sector.

Were I compare their payouts to those of public sector janitors, that comparison would be just as fair as your comparison.

Haha, very funny about your union example. Can I CHOOSE not to use the defense and pork related services of Lockheed, Boeing, Northrop Grumman, General Dynamics, United Technologies, L-3 Communications, Oshkosh Truck Corporation, etc, etc, who play the influence game of elected officials better than unions?

Of course not. They all get cost+ no-bid contracts for billions, and pay there executives way, way higher than the public sector.

Never hear a peep from you about that problem, Tough Love. Now why is that?

May 31, 2013 at 3:11 pm

Spension, You so full of it (with MORE of your intentionally distracting BS).

I gave you a VERY specific workup showing ALL the details (unlike the Fix Pensions First study) … and you can’t find even one thing wrong with my workup. Because you know it’s correct and there is no mistake.

What justifies the TAXPAYER-funding of Police Officer retirement packages 5 times greater in value than what a Private Sector worker making the SAME pay, having the SAME years of service , and retiring at the SAME age ?

Nothing !

May 31, 2013 at 5:15 pm

The problem that we are dealing with is an aging workforce. This is particularly the case if the pension plan is providing port-retirement COLA adjustments as do most state and federal retirement programs.

Pension plans are to be funded evenly over an employee’s years of service with the employer. However, as wages increase the promised benefits also increase and the funding must catch-up. The result is required increased employer contributions to fund the promised benefits. COLA adjustments are another way that benefits can increase without the necessary funding to provide for the increased benefits.

When a large portion of the employees are older – i.e. baby boomers – the employer contributions grow to the point that the employer can no longer cash-flow the contributions required to provide the increasing benefit, so it freezes the plan and converts to a 401(k) plan where theemployer contribution cost can be controlled.

Because State and Federal employers do not need to earn their revenue in the marketplace, they have not frozen or terminated their defined benefit pension plans, but instead just seek more and more revenue via higher taxes and deficit spending.

However, we have gotten to the point that this has become unfair to persons who work in the private sector who have had their benefits reduced but are having to pay ever increasing taxes and deficit spending for the ever increasing pension liability of the state and federal employees.

May 31, 2013 at 8:48 pm

Tough Love, what justifies Jack Welch, whose company got rich on taxpayer-funded bailouts and no-bid contracts from the government, and whose job was considerably less difficult than that of the Governor of California, getting >$400 million in post-employment benefits?

Your workup was a laughable distraction. There is no attempt on your part to survey a broad selection of workers and no attempt to do a fair apples to apples comparison. That is a devastating criticism and fatal flaw to your `analysis’ (really just a random anecdote).

And what justifies Lockheed, Boeing, Northrop Grumman, General Dynamics, United Technologies, L-3 Communications, Oshkosh Truck Corporation, etc getting no-bid contracts and paying their executives huge salaries and post-employment benefits through *their* influence over elected officials?

You won’t answer, so it is fair to conclude: you are paid by non-public sector companies like those to post here.

I’m in a DC plan as are my relatives, BTW. So stop your non-sequiturs attacking me. It is by analyzing my DC plan that I realized how awful the DC industry is in the US.

June 1, 2013 at 1:59 am

Spension

Still can’t find even ONE error in my (above fully-detailed) workup demonstrating that the Taxpayer paid-for share of Police Officer retirement packages are worth almost 5 times that of the comparable Private Sector worker ?

And STILL even MORE distraction from the ROOT CAUSE of our financial ills …. the grossly excessive Public Sector pensions, by AGAIN bringing up excessive Private Sector CEO pensions ? Who cares about the CEO pensions. If their cost makes the company’s prices too high, I can shop elsewhere. I can’t do that for town and state services.

Your pathetic.

June 1, 2013 at 2:50 pm

Greatly exceeded in the pathetic category by you.

The GROSS error you make is comparing ONE category of public sector workers to ONE RANDOM ANECDOTE from the private sector. Fix Pensions First carefully compared apples to apples, broad groups of similar workers to one and other. You clearly have no numerical or statistical ability.

Did I mention you couldn’t tell the difference between a few million $and $100 million? You are innumerate, Tough Love.

Go try to shop elsewhere for all the no-bid, cost+ contracts that the private sector loves, where no taxpayer can shop elsewhere for the products from Lockheed, Boeing, Northrop Grumman, General Dynamics, United Technologies, L-3 Communications, Oshkosh Truck Corporation. Your denial of the fact that the private sector is JUST AS BAD as the public sector is pathetic, Tough Love.

And that doesn’t even mention the same (and actually more costly analogies) in the health care, where hospitals whine and moan about only getting cost+ (where part of the cost is $1 million + salaries for executives of modest ability). Go try to walk away from the hospital in most towns in the US, Tough Love.

You’re so pathetic you love the Donkey Punch the private sector in the US deals you every day.

As for comparisons, remember, CEOs subsidized by the taxpayer get >$100 million post-employment payouts. You love that, Tough Love. Likely they are paying you to post your innumerate errors here.

Did I mention the $24 trillion by the taxpayer (according to the SIGTARP) given to Wall Street private sector for their irresponsible and innumerate behavior? Go try to shop elsewhere to avoid that problem, Tough Love.

I always agree that public pensions are too high in California. But a substantial contributing factor is the stealing from the private sector at the many-$trillion level the private sector conducts with just the same tactics of influence that public unions learned from the private sector. You are a freier and a dupe for that private sector, Tough Love.

June 1, 2013 at 9:52 pm

Spension, So, you STILL can’t point out even ONE error in my (above fully-detailed) demonstration that the Taxpayer-funded share of Police retirement packages are almost 5 times greater in value at retirement that of a Private Sector worker making the SAME pay, retiring at the SAME age, and having the SAME years of service…. and STILL more attempts at diversion form the issue at hand …………..

The Grossly Excessive Taxpayer-funded (to the tune of 80-90% of total Plan costs) PUBLIC Sector pensions …. always multiples greater in value at retirement than those granted their Private Sector counterparts.

ALL of you (diversionary) efforts to draw attention to the excesses in the Private Sector are irrelevant. Taxpayers do NOT pay for those excesses and have CHOICES where to shop for PRIVATE Sector products and services …. unlike for PUBLIC Sector service for which we are a “captive” consumer (like it or not). We are FORCED pay for the excessive pensions & Benefits granted PUBLIC Sector workers.

June 1, 2013 at 11:03 pm

Your are both right.

Many in the private sector would be helped by a state run program, but not if it is going to be poorly run and funded out of excessive taxes!

June 2, 2013 at 12:17 am

I have OBVIOUSLY pointed out a HUGE error in your above, pathetically UNREASONABLE and INCONCLUSIVE comparison: you don’t survey broad categories of workers and make a fair comparison. Fix Pensions First did.

Public pensions are too high, but not by the factors your ERROR-PRONE comparison alleges, Tough Love.

The EXCESSES of the PRIVATE SECTOR are a significant driving force for the EXCESSES in the PUBLIC SECTOR.

THEIR WAS NOT SHOPPING FOR THE EXCESSIVE MILITARY CONTRACTS, HEALTH CARE CONTRACTS, and WALL STREET BAILOUTS. THE TAXPAYER HAD TO PAY BECAUSE OF THE INFLUENCE OF THE PRIVATE SECTOR ON LEGISLATORS, ELECTED AND APPOINTED OFFICIALS.

Keep your head buried in the sand, Tough Love, while your private sector friends do what they will with the parts above ground.

June 2, 2013 at 1:35 am

Quoting …”I have OBVIOUSLY pointed out a HUGE error in your above, pathetically UNREASONABLE and INCONCLUSIVE comparison: you don’t survey broad categories of workers and make a fair comparison. ”

No you haven’t.

Go back to my (above) long & detailed demonstration of exactly how the Taxpayer paid-for share of the Police Officer’s retirement package is almost 5 times greater in value at retirement than that of the comparable Private Sector worker.

I’ve challenged you to even one small mistake.

You simply can’t get yourself to admit that it’s correct … and that you’re wrong.

**************************

Aren’t all those CAPITAL letters consider internet yelling? You’re losing it .

June 2, 2013 at 4:08 pm

Yes, and every one of these private sector employees of companies with HUGE taxypayer bailouts and no-bid cost+ contracts:

Click to access GMI_GoldenParachutes_012012.pdf

Had post-retirement payouts 208 times GREATER than that of a CalSTRS teacher. One got a payout 870 times GREATER than that of a CalSTRS teacher.

Tough Love, you’ve never found a single error in my analysis.

You pretend that the taxpayer has SOME KIND OF CHOICE ABOUT USING THE SERVICES OF THOSE COMPANIES. BULLOCKS, YOU MICROCEPHALIC.

Tough Love, you find it completely acceptable that $400+ million payouts to a single individual, based largely on taxpayer subsidies, go to your buddies. But you shriek bloody murder when public sector employees copy the private sector and use influence to get their overlarge payouts.

OF COURSE I CAPITALIZE MY CONDEMNATION OF YOUR DUPLICITY.

June 2, 2013 at 8:08 pm

Spension,

Well, you”almost’ stopped with the Caps … that’s progress.

But … you STILL can’t find even one single error in my (above) lengthy and detailed “demonstration” of exactly how the Taxpayer paid-for share of the Police Officer’s retirement package is almost 5 times greater in value at retirement than that of the comparable Private Sector worker (comparable in cash pay, in age at retirement, and in years of service).

Not up to the challenge ? No math skill ? Concentrate, it’s actually quite easy to follow it through to my conclusion… 4.55 times greater for the policeman than the Private Sector worker.

June 2, 2013 at 9:35 pm

Spensions- God Bless ya for trying but the tlovr is a bit slow.

June 2, 2013 at 10:00 pm

Tough Love, you STILL can’t find a one single error in my (above) lengthy and detailed “demonstration” of exactly how the Taxpayer paid-for share of one Police Officer’s retirement package is totally not representative of any useful comparison of public and private sector pensions. Your argument has been trashed, go back to getting your drinking water from your commode.

In fact, in the private sector, people get 800 times the benefits of public workers, as documented on these two websites (you never refer to any websites to back up your made-up numbers);

Click to access GMI_GoldenParachutes_012012.pdf

Click to access Full_Report.pdf

June 3, 2013 at 3:25 am

Wow spension, I don’t think even you want this schnook Bjoren on your side.

And what ..”lengthy and detailed “demonstration… from you?

No spension, a demonstration is your own MATH workup and can be examined and challenged … as I have put forth;

You just like to parrot others, have little original to say, and quite apparently either do have the ability to critique my demonstration or know it’s accurate and just can deal with that.

And then AGAIN you go back to the “private” sector diversionary tactics..

LOL

June 3, 2013 at 3:33 pm

Your `demonstration’ is mathematically inadequate, as you are in everything. It is *you* who brings up the private sector as some sort of holy church, and you always avoid any discussion of all the ways the private sector is identical to public sector unions.

Shows who is paying you, TL.

LMFAO.

June 3, 2013 at 5:41 pm

Spension,

Sorry spension, but when a fully and complete demonstration with every step is presented, simply “saying” is mathematically inadequate” isn’t saying anything at all ….. EXCEPT supporting my assertion that you can’t find ANYTHING wrong.

I’ll bet that bugs you.

June 3, 2013 at 9:53 pm

No, nothing you write bugs me. You are about as serious as a 1-year old. Nothing they say bugs me either. You have no idea how to do a fair, apples-to-apples comparison, and that is what is wrong.

Oh yes, of course, in your view the private sector can do no wrong, whether it is their graft and corruption of elected officials, their $24 trillion bailout, Enron, Madoff, Long-Term Capital Management, etc, etc.

June 3, 2013 at 11:09 pm

Spension, Nah…doesn’t bug you….. but::

(a) You repeat ad-nausea the distraction about Private Sector excesses when the issue at hand is the Grossly Excessive PUBLIC PUBLIC Sector pensions and benefits…. from which Taxpayers have few (if any) ways to escape to cost. Nobody care about excesses in the Private Sector…. because in the PRIVATE Sector we have CHOICES, and can shop elsewhere if that greed translates into higher prices.

(b) You can’t find ANYTHING Wong with my above long and clear (step-by-step mathematical) demonstration that the Taxpayer-paid-for share of a Police Officer’s pension is almost 5 times greater in value at retirement than that of the Private Sector worker making the SAME pay, with the SAME yeas of service, and retiring at the SAME age.

You have no math skills (a few others) and just like the hear yourself talk.

June 4, 2013 at 2:54 pm

Tough Love,

(a)*you’re* the one that keeps bringing up the private sector. The Grossly Excessive private sector behaviors ($24 trillion bailouts, Enron, Randy Cunningham bribed by defense contractors, Madoff, etc) were done on TAXPAYER’s MONEY. Yes, public pensions are too high, and you do have a choice… move to Somalia or Mali where you won’t have to pay anything. THERE IS NO CHOICE WHEN IT COMES TO ALL THE PRIVATE SECTOR EXCESS IN WALL STREET, THE MEDICAL SECTOR, PRIVATIZATION OF PUBLIC UTILITIES, YOU DUMMKOPF. That you maintain otherwise proves you are paid by those interests to ignore their excesses.

(b)Your comparison is not representative of the broad cost of public pensions versus private sectors. The Fix Pensions First study was much more accurate than your cherry-picked anecdote.

Unlike you, I don’t have to talk when I read or write, Tough Love. Enjoy talking to yourself.

June 4, 2013 at 7:01 pm

Tough Love, I think you win the battle in this thread. Your assumptions were reasonable in the scenario and you showed your math.

The numerous corrupt military contracts spension are best dealt with on blogs for that purpose. $100M golden parachutes, too big to fail banks and crony capitalism bailouts are best dealt with by electing the bums out.

June 4, 2013 at 10:53 pm

Electing those out who made the public pension deals is a good idea too…

Here is the reference for the study that gave public pensions only 1.26-1.78 higher when compared apples-to-apples.

See page 24 of http://www.fixpensionsfirst.com/docs/Full_Report.pdf

Indeed safety is higher, but that is because (as proven in Wisconsin, San Diego, etc) there is an electoral consensus to give police/fire a sweet pension deal. Gov. Walker in Wisconsin did not eliminate collective bargaining for police/fire unions, and the various changes in San Diego didn’t touch the police/fire.

June 5, 2013 at 2:09 am

spension goes a bit nuts on beating up defense, etc, but he wins the basic point on this thread.

June 5, 2013 at 2:24 am

Somewhere, somehow, dollars to donuts, spension (of a family member) benefits from a continuation of the grossly excessive pensions and benefits afforded Public Sector workers today … and GROWING every day we delay in putting an end to it (for CURRENT, not just new workers)

P.S. I’m STILL waiting for you (spension) to find even one thing wrong with my mathematical demonstration that Police office pensions are almost 5 times greater than a similarly situated Privater Sector workers.

In my opinion, either you’rr not up to the challenge or you know it’s correct … and that REALLY REALLY bugs you.

June 5, 2013 at 5:45 pm

Spensions clearly gets the math and argues with respect and little emotion. Poor t love has an agenda that is a mile wide and an inch deep. Apples are apples.

June 5, 2013 at 6:34 pm

Bjorne, Tell us what you do for a living so we can determine if you have an “Agenda”?

And FWIW, I don’t, other than strongly advocating to reduce what I see (as someone very well dedicated in this subject) as Grossly Excessive pensions and benefits (multiples greater than their Private Sector counterparts get) which, when added to “cash pay” that is no less than that Private Sector counterpart, results in unnecessarily generous “Total Compensation” in the extreme.

Let me venture a guess as to you occupation and “agenda”…

Public Sector worker, with a simple agenda …. no matter how generous, how costly, how excessive, and how burdensome to Taxpayers (who foot 80-90% of the total cost) …. you will not give an inch of pay, pensions, and benefits in helping solve the financial mess we are in.

Ok, yes, maybe one inch for each MILE we need in givebacks.

June 5, 2013 at 6:36 pm

“dedicated” was supposed to say “educated” in my above comment.

June 5, 2013 at 7:00 pm

Somewhere, somehow, dollars to donuts, Tough Love (or a family member) benefits from a continuation of the grossly excessive bailouts, no-bid & cost+ contracts, etc to the PRIVATE SECTOR … and those are GROWING every day we delay in putting an end to it.

The mathematical demonstration, Tough Love, is: you cherrypicked one anecdotal example. Fix Pensions First made a concerted effort to compare apples-to-apples. Your work is hopelessly biased, from picking a single anecdotal example. BTW, the safety portion of the Fix Pensions First starts on page 33. You don’t bother to read it, or grapple with the problem of finding a private sector equivalent to safety employees. Use Blackwater? Use William Bratton? Go figure. Your example is so contrived that it is laughable. AND not even Gov. Walker in Wisconsin got reductions in safety benefits.

As for what to do practically with high CA pensions you have offered no useful or practical solutions. I have. I agree CA public pensions are too high. But negotiations backed up with preparation for sovereign default are the only practical solution.

Nothing you write bugs me, nor does your need to speak the words out loud when you read or write bug me, Tough Love.

June 5, 2013 at 7:50 pm

Quoting Spension … “Somewhere, somehow, dollars to donuts, Tough Love (or a family member) benefits from a continuation of the grossly excessive bailouts, no-bid & cost+ contracts, etc to the PRIVATE SECTOR … and those are GROWING every day we delay in putting an end to it.”

You never “listen”. I agree with you in wanting and feeling we need to address and fix the issues in your above quote. I have simply chosen not to fight that battle (and need) as I feel the impact of those things much less directly than the excessive taxes I must pay today (and will likely increase dramatically w/o the reductions I advocate for) to support the absurdly generous compensation of Public Sector workers.

ALL of the issues you mentioned need fixing …. It’s just that YOU use THAT need as an excuse to minimize, distract from, and NOT pursue the HUGE need for intermediate and very material reductions in the grossly excessive pensions & benefits granted Public Sector workers.

While I don’t really “know” if you are benefiting for the status quo of excessive Public Sector pensions, your endless distracting tactic of pointing to the ills of the Private Sector certainly makes it look like you do.

***************************

And you STILL can’t find any mistake in my demonstration. If not, what’s so hard to just admit that my example is correct, certainly implying that Private Sector Taxpayers are getting a royal screwing with the pensions we are being forced to to pay Police Officers. …. and that they should be materially reduced for FUTURE Service pension accrual of CURRENT workers.

Do you think your “saying” … “Your example is so contrived that it is laughable. ” ……. means anything without specifics ? It just makes you look foolish.

June 6, 2013 at 12:04 am

This `spension’ makes sense to me. You can’t generalize from one example of a police pension to all those public workers, Mr. Tough Love.

June 6, 2013 at 2:13 am

Max, I wasn’t “generalizing”,nor did I ever say I was.

That being said, if Public Sector jobs for workers with pension/benefit formulas less rich than Police Officers come in at only 2-4 times greater (as they do …. under a similar analysis) vs the 4.55 times greater for Police officers in my above example, should Taxpayers (whose Public Sector pension contributions and the investment earnings thereon) pay for 80-90% of total Plan costs find that acceptable ?

I was giving ONE specific example comparing a TYPICAL California Police officer’s retirement package (which I feel is an absurdly generous) to a comparably situated Private Sector worker …. clearly *step-by-step” demonstrating that the Police officer’s retirement package is 4,55 times greater in value at retirement,

The current (grossly excessive) structure for ALL Public Sector pensions and benefits is simply a financial rape of Private Sector Taxpayers.

June 6, 2013 at 2:26 am

Max, you don’t need to generalize from one group to another. You can look at each group separately and easily come to the conclusion that each groups pensions are placing a huge burden on all levels of government and, by extension, all taxpayers. Of course some public employee groups pensions cost more than others, but most cost 2-3 times the normal cost (or more), and it’s about to get much worse.

If the employee unions do not want to contribute more toward their own pensions, or even reduce the formulas going forward, what makes you think taxpayers want to pay more?

TL makes sense to me. I like spension but I’m not a fan of his “sovereign default is the best option” claim. IMO, what spension is saying is we should just accept failure and then pick up the pieces later. That’s a defeatist strategy in my book, and I think we should be able to do much better. Let’s see how the whole sovereign default strategy plays out in Illinois why we work on fixing our problems here in CA.

June 6, 2013 at 3:01 am

Captain, Your last sentence is on point. Often it takes witnessing a disaster for it to sink in that it could also happen to you.

June 6, 2013 at 3:28 am

There isn’t going to be a one-shot fix for the desperate state in which more and more Public Sector pension Plans are finding themselves. Most states, cities, & towns have a fundamental STRUCTURAL problem which MUST be addressed.

Long ago, Civil Servant “cash” pay was quite a bit less than Private Sector pay in incomparable jobs. This justified a better pension & benefit package.

Per the US Gov’t BLS, cash pay alone is now higher in the Public Sector than in the private sector. This justifies AT MOST comparable (but certainly NOT better) pensions & benefits.

More valuable Public Sector pensions comes from multiple sources: (1) higher formula per year of service, (2) basing pensionable compensation on the final 1 year instead of 3 or 5 years of service, (3) including post retirement COLAs, (4) arbitrary end-of-career promotions or excessive raises to “spike” the pensionable compensation, (5) allowing the soon-to-be retired to load up on overtime includable in pensionable compensation, (6) including payouts of unused vacation, unused sick days, uniform, parking, and other miscellaneous “allowances” in pensionable compensation, etc.

In MOST Corporate Pension Plans NONE of the above are included. Why? Because the cost would have to be paid for by the employer, and none of these being really justified, employers are not foolish enough to waste THEIR money this way.

In the Public Sector ALL, of the above are generally included/allowed. Why? Our Politicians aren’t spending THEIR money, their spending YOUR money (via your taxes) while they curry favor for campaign contributions and election support.

Sometimes, Corporate Sector Pension Plan sponsors realize that the plan is no longer affordable, so they reduce cost via formula reductions, increases in the retirement age, etc., for NEW employees and for FUTURE years of service for CURRENT (yes CURRENT) employees. This is ROUTINE in the Private Sector and is allowed by ERISA (the Federal Law that governs Private Sector Plans).

Just as in the Private Sector, CURRENTLY EMPLOYED workers in the Public Sector have already “accrued” pension benefits for PAST service. To this will be added benefits for FUTURE years of service. However, in the Public Sector (and there are variations from State to State) the ability to reduce the pension formula for FUTURE years of service for CURRNT employees is “questionable”.

Of course, the employees and their Unions say it cannot be reduced for anyone already employed (even for those very recently hired). There are many variations, e.g., NJ’s Office of Legislative Service said that cannot be changed only for current employees who already have 5 years of service. In some States, the rules that govern such potential Plan changes are in the State Constitution. In others, in Laws/Regs., and in others via Court Case law.

One important consideration in examining the DIFFICULTY in reducing pension for (FUTURE years of service ONLY) for CURRENT employees is that the legislators, judges, and staff (such as in the NJ example above) that “opine” that such reductions are not allowed are THEMSELVES participants in these same pension Plans and would be negatively impacted by such formula reductions.

Hence, they are hardly disinterested parties, but come with a built-in conflict of interest. These persons should not be making decisions that favor THEM (as beneficiaries of their own decisions) but add to the taxpayers’ burden.

The financial situation across the country is getting more dire, and the ROOT CAUSE must be addressed. Stated another way, we must once and for all, address the STRUCTURAL imbalance between income and expenses.

Way too much focus has been placed on the government entity’s neglect to “fully fund” the Plans. This is certainly true (to varying degrees across the nation). What is often given short-shrift is the “expense” side of the income statement. No one ever says …gee … funding a VERY generous pension plan is VERY expensive, and then moves to the logical next questions, that being, is it too expensive BECAUSE it is too generous and perhaps we such make it less generous.

But what exactly is “too generous”? Well, given that “cash” pay in the Public Sector now exceeds that of the Private Sector in comparable jobs, maybe a Public Pension Plan that is more than MARGINALLY higher is too expensive.

Above, I enumerated 6 items which make Public Sector Plans more expensive. Few people not educated in pending funding understand just how VERY valuable (and hence EXPENSIVE) these differences are. One thing is certain, the Public employee Unions know. That’s why they fight tooth-and-nail to stop changes.

Here is an accurate comparison of the costs of Public vs Private Sector retirement packages (pension plus retiree healthcare, if any) …. The value (i.e., cost to purchase the pension/benefit package) at the time of retirement of the employer-paid (i.e., Taxpayer) share of the typical (non-safety) worker’s retirement package is 2-4 times that of employer-paid share of the comparable (in pay, years of service, and age at retirement) Private Sector worker, and that multiple increases to 4-6 times for safety workers (policemen, firemen, corrections officers, etc.).

I’ll bet you had no idea that this HUGE disparity exists. Given that it does, and given that Public Sector “cash” pay by itself is higher, is it surprising that States, cities, towns are being so squeezed to fund this? Not at all.

So what is the solution? Of course Civil Servants deserve “fair” pay as well as “fair” pensions & benefits, but “fair” should mean COMPARABLE to what their Private Sector Taxpaying counterparts get. Right now, this is anything but true.

The EXPENSE side of the income statement has been neglected far too long. To reach a “structural balance” we need to reduce current pensions (as well as retiree healthcare subsidies) in the Public Sector to a level comparable to that of the Private Sector. A few more progressive States & Cities (or perhaps, those in the greatest financial pain) know they must look at this and are beginning the baby steps.

But the BIG problem is the conflict-of-interest conundrum that reducing pensions for CURRENT employees will (in many cases) reduce there own pensions. So, they ONLY propose plan reductions for NEW employees. To be fair, this may be happening not because they just “cave” on addressing such reduction, but because they really believe it is not possible.

A disinterested party might look a bit harder. Perhaps we need to get opinions from outside this circle, e.g., from university scholars. Or perhaps challenges should be brought in the Federal Court system where the conflicted parties are no longer the decision-makers.

Not addressing the huge cost of future accruals for current employees is wishing-away current financial reality. The dire financial problem is here NOW. Reducing pensions ONLY for NEW employees will have little impact for 20-30 years until they begin to retire. We will never make it. But also, given that most (objective) observers agree that current pensions & benefits are overly generous (compared to Private Sector plans … while appropriately taking into account compensation levels), why should we CONTINUE to layer on MORE excessive pension accruals?

It’s been said that the first step in getting out of a big hole is to STOP DIGGING. Well, every day we allow the current plan to continue, the hole gets deeper.

Somehow we need to find the way to reduce pensions (not for PAST) but for FUTURE years of service for CURRENT employees. That, along with a significant reduction in the retiree healthcare subsidy just MAY save us.

June 6, 2013 at 4:02 pm

Spension, In response to an SEIU demand for cash pay increases (money which the Sttae of CA says it does not have to offer) in THIS article,

http://blogs.sacbee.com/the_state_worker/2013/06/seiu-1000-president-contract-fight-is-on-with-jerry-brown.html

I posted this comment (just below). Your thoughts ?

——————————————————————–

What we should do … Step-By-Step:

(A) —- The State should do a side-by-side comparison of the pensions promised these SEIU workers and those of typical Private sector workers assuming the SAME pay, the SAME years of service and the SAME age at retirement. Then deduct the accumulated value (with investment earnings) of any REAL employee contributions for both the Public and Private Sector worker to get he net EMPLOYER-PAID pension cost.

When one realizes the VERY high cost of

(a) the much richer formula,

(b) the MUCH younger full (unreduced) retirement age,

(c) the inclusion of post retirement COLA increases,

(d) the MUCH more liberal definition of “pensionable compensation”,

(e) etc. etc, etc

it’s not hare to see how the Public Sector worker’s pension ALWAYS comes out 2-4 times (5+ times for safety workers) greater in value at retirement than that of the comparable Private Sector worker.

(B) — Next, we should do a similar analysis for any Retire heathcare subsidies promised the Public and Private Sector workers, noting that

(a) While such subsidies are virtually universal, and often a high (even 100% in some cases) percentage of the total cost in the Public Sector, VERY few Private Sector employers subsidize retiree healthcare any longer, and of the diminishing number that still do, most often, they pay a very modest share of the costs.

(b) Healthcare costs grow rapidly with attained age, and 55-64 year olds use MUCH more healthcare services than say 30-39 year olds. Therefore, pre-age 65 (and not Medicare-eligible) retirees have VERY high costs. Since it is VERY common for Public Sector workers to retire in the 50’s, their pre-Medicare health costs are very expensive ….. and typically hundreds of thousands of dollars (and often doubling it if other family members are covered as well) … vs almost ZERO for the Private sector worker (who rarely gets any employer subsidy).

(C) — Next we should determine the value of any

miscellaneous benefits, life insurance subsidies, disability insurance subsidies, transportation allowances, etc.

(D) — Next we should determine “cash pay.”

(E) — Next, we should (separately for the Public and Private worker) express each of the pensions/benefits in (A), (B), and (C) as a level annual percentage of “cash pay” (the item in (D)) sufficient to fund that pension/benefit over the working career of the employee, using reasonable but conservative assumptions (so as to have a high probability that the pension/benefit is FULLY funded by the time that employee retires).

(F) — Since a reasonable (i.e., intelligent, non-greedy) person should agree that EQUAL Public and Private Sector “Total Compensation” (“cash pay”, plus pensions, plus benefits) in comparable jobs (or jobs with comparable risks, educational requirements, knowledge, and skill sets if not directly comparable) is a fair and appropriate goal, we should …. separately for the Public and Private Sector worker ….. add to “cash pay” from item (D), the level annual % of pay values for pensions and benefits from item (E). The result is “Total Compensation” separately, for the comparable Public and Private Sector worker.

(G) —- If the SEIU worker’s “Total Compensation” from (F) is lower than that of comparable Private Sector workers, it should indeed be raised to that level. Under the same (very FAIR) logic, If the SEIU worker’s “Total Compensation” from (F) is greater than that of comparable Private Sector workers, it should be lowered to that level. In the latter case, is clear that doing so (actually LOWERING their compensation) is, shall we say “complicated”. In that situation the Public Sector worker’s “cash pay” should be frozen until (with the expected growth in Private Sector “Total Compensation” over time) the

Public Sector “Total Compensation” equals that of the comparable Private Sector worker.

Readers …… For WHICH (the Public or Private Sector) worker do you think “Total Compensation” (as determined by my above-outlined steps) will come out higher, and by how much (expressed as a level % of “cash pay”) ?

June 6, 2013 at 11:44 pm

TL, go read the Fix Pensions First study. Pretty much did what you recommend.

Captain, the contracts held by the unions and other state employees (isn’t there something about contracts in the US constitution, maybe in Article I, Section 10, Clause 1?) are pretty strong. As far as I can tell, the only 2 options are a)negotiate reductions, which seem hopeless, unless backed with a credibly thought out and serious b)plan for sovereign default.

One cannot maintain that greed is good for the private sector and bad for the public sector. It has to be: greed is bad in both sectors.

June 8, 2013 at 4:56 am

“One cannot maintain that greed is good for the private sector and bad for the public sector. It has to be: greed is bad in both sectors.”

Who says the private sector is all about greed, other than you and a few movies? What you call greed in the public sector I call collusion. Public sector employees are free to join the private sector anytime they want.

June 12, 2013 at 5:51 am

Uh… ever heard of Wall Street, Captain?

June 12, 2013 at 9:57 am

Yes, Spension, I’ve heard of Wall Street.

Not sure what your point is but I do know that CalPERS is continuing to place large “bets” on very risky and speculative gambles. And, of course, If CalPERS continues to lose they will just continue to increase the cost, as of percentage of payroll, that taxpayers will be stuck paying.

IMO, CalPERS is Gambling with other peoples money – taxpayer money. And the CalPERS crooks are no better better than the MOB.

June 12, 2013 at 9:34 pm

Uh… try a huge number of books, government reports, blue-ribbon panels (http://en.wikipedia.org/wiki/Financial_Crisis_Inquiry_Commission) indicating the overwhelming greed driving our Private Sector.

Sure, public pensions caught the fever from the Private Sector.

June 13, 2013 at 12:03 am

Cal Pers value…..267 Billion!

Gambling indeed!

June 13, 2013 at 12:13 am

Tough love. I have to laugh, u want me to reveal personal info out here? You would have been good in 1938 Germany. What a joke.

I am a physician. I live in Orange County. I have been a resident here for many years. What does this have to do with anything? Would you like to contact me? I can arrange that.

June 14, 2013 at 3:16 am

Bjorne ….. A physician working for the Public or Private Sector ?

June 14, 2013 at 2:37 pm

What are you, a Nazi? I guess you have a chilly view of free speech. Laughable.

June 14, 2013 at 5:27 pm

Bjorne, Isn’t that a wee bit extreme …. calling me a Nazi because I strongly advocate to rightfully reduce the grossly excessive pensions granted PUBLIC Sector workers, 80-90% paid for by TAXPAYERS contributions and the investment earnings thereon …. earnings that (in the absence of the need to fund these grossly excessive pensions) would have stayed in the TAXPAYERS’ pockets, perhaps to fund there much SMALLER pensions ?

July 26, 2013 at 4:07 pm

As a Californian, let me assure our Golden State employers that, once this program is in place, a “fairness” adjustment will be made by our thoughtful state legislators. After all, why should the employee plan contributions not be matched by those greedy capitalist employers? Given that we are often now ranked the worst business climate state in nation, what’s to lose?

Also, expect further benevolent state guidance as to what INVESTMENTS constitute a “prudent selection” for participants. Either through incentives or edict, Sacramento will point this new pot of money towards progressive-favored (and riskier) investments (solar, wind, city rejuvenation, etc.) or outright government enterprises such as subsidized housing and the “loans” to government.

Any Californian who believes that the employers and/or CA taxpayers are not in fact on the hook for any “unexpected” shortfalls in the plan’s investment fund haven’t been paying attention these past 30 years.

Oh yeah, this is gonna go well.