CalPERS last week gave some 1,575 local governments a small increase in their annual pension costs, one of the last rates kept low by unusual actuarial policies adopted after a $100 billion investment loss five years ago.

As a slowly improving economy bolsters government budgets, CalPERS is considering changes in investment and actuarial policies that could “turn on the spigot” over the next few years, requiring employers to put more money into the pension fund.

CalPERS funding levels are low, around 70 percent. Officials fear another big investment loss could require unworkable rate hikes to get to 100 percent funding. So a risk-based investment policy is being considered to cut losses in future downturns.

The level of the big CalPERS state worker fund is projected to drop to 60 percent in 50 years, even if earnings average 7.5 percent. Proposed actuarial changes would boost funding levels, avoid conflicting debt reports and make employer rates more predictable.

Did keeping a lid on rates put the system in jeopardy to avoid a rate shock that could trigger sweeping reform? Or were government budget cuts prudently eased during a financial crisis by a flexible pension system with a long recovery time?

Whatever the case, twin processes that could result in CalPERS board approval of major policy changes later this year are being led by Joe Dear, the chief investment officer, and Alan Milligan, the chief actuary.

The board is scheduled to consider “capital market assumptions” in May and a risk-based “decision framework” for investments in July. The goal is to adopt a new asset allocation while the economy is relatively good.

“We face higher rates if we do reduce the portfolio return,” Dear told the board last week. “As the charts indicate, this draw-down risk is absolutely associated with the portfolio risk we run with the exposure to growth in the portfolio, and when growth is good the portfolio does well.”

“But what we can’t withstand is another big loss,” he said. “Because in that circumstance we will not be able to grow our way out. Then the only recourse is contribution rates, and those increases would be punishingly high.”

Milligan wants to end the current actuarial clutter: a radical 15-year period for “smoothing” investment gains and losses, a “corridor” to limit smoothed values, rolling “amortization” that refinances debt each year, and two sometimes sharply different estimates of debt or “unfunded liability” based on the smoothed or market value of assets.

The chief actuary is proposing a conservative “direct” smoothing policy that would determine the rate increase needed to reach a funding level of 100 percent in 30 or 35 years, then phase in the rate increase over five years.

An example given the board last week: Under current policy, the employer contribution for most state workers, 20 percent of pay, is expected to increase to 23 or 24 percent of pay over the next two decades before dropping sharply to 12 or 13 percent.

Direct smoothing for full funding in 30 years would increase the employer contribution to a peak of 28 percent of pay in five years, decline over the following 15 years to 23 percent, fall sharply to 15 percent and fall again to 5 percent after 30 years.

These comparisons assume that investment earnings average 7.5 percent. But CalPERS expects to get about two-thirds of its revenue from investment earnings, which are unpredictable and have gained or lost 20 percent or more in a single year.

It’s a giant unknown or X factor, which makes running a California public retirement system a little like placing a bet in a big casino, where the taxpayers pick up the tab if you crap out.

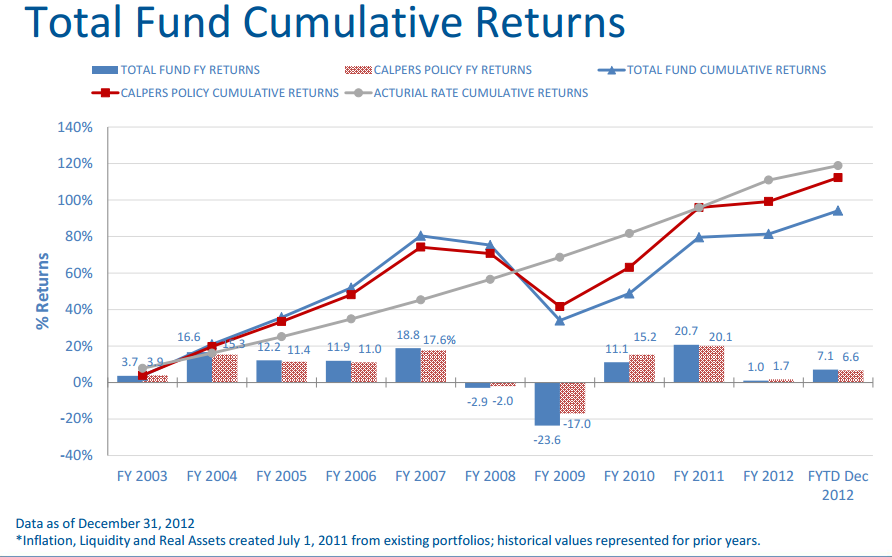

CalPERS 10-year returns: target (gray), actual (blue), policy benchmark (red)

The CalPERS board was shown several examples from 1,500 random simulations of the next 50 years, comparing current policy with proposed alternatives. One takeaway: a small rate increase can make a big difference in later funding and rate levels.

There is a better than 50-50 chance that CalPERS will fall below 50 percent funding at some point. The probability is 59 percent under current policy and 52 to 56 percent under four alternative methods.

The probability of the employer rate going above 40 percent of pay is 13 percent under current policy, 31 percent under the proposal to reach full funding in 30 years. The big difference is in rate shock, a single-year rate increase of more than 5 percent of pay.

The probability of that kind of rate shock is 59 percent under the current policy, but only 8 percent under the direct smoothing proposal aimed at reaching full funding in 30 years.

The board is scheduled to hear the proposed actuarial changes in March, followed by adoption in April. The changes would not affect rates until fiscal 2014-15 for state workers and non-teaching school employees and fiscal 2015-16 for local governments.

But Milligan said projections of the rates resulting from the new actuarial methods will be given to employers in their annual valuations before then, if the board adopts the proposed changes.

“This is along the lines of giving the employers that extra predictability they have been asking for,” Milligan said, referring to a common request at annual meetings, “and I think we should try our darnedest to get that extra predictability for them.”

Another factor likely to raise rates (in addition to changes in investment and actuarial policy): People are expected to live longer.

An insurance executive on the CalPERS board, Dan Dunmoyer, raised the mortality issue last week. He said the average female under 30 is expected to live to be 100.

For CalPERS, that means the average young female state worker could retire after 30 years of service at age 55, then for the following 45 years collect a pension equal to 60 percent of final pay that adjusts for inflation.

Milligan said employers and the board have been told that when a scheduled experience study is completed, probably next February, he will recommend that a mortality projection be included in the actuarial assumptions.

“That will result in an increase in employer contributions,” he said.

The CalPERS investment fund peaked at $260 billion in the fall of 2007, fell to $160 billion in March 2009 and was $253 billion last week. CalPERS had put a lid on rates in 2005 by adopting a 15-year smoothing period, well beyond the usual 3 to 5 years.

But after the big loss in 2008, most employers were still facing a rate increase of 5 to 10 percent of pay. So as part of three-year phase in of the rates, CalPERS temporarily widened the corridor limit on smoothing valuations.

When CalPERS lowered its earnings forecast from 7.75 percent a year to 7.5 percent last March, the resulting rate increase of 1 to 2 percent of pay was phased in over two years, cutting the first-year impact by half.

Under the local government rates set last week for fiscal 2013-14, the average employer contribution for miscellaneous workers increases 0.4 percent of pay to 15.3 percent of pay and for average safety workers 0.8 percent of pay to 32 percent of pay.

Three years ago, the fiscal 2010-11 local government rates averaged 13 percent of pay for miscellaneous and 25.1 percent of pay for safety workers, mainly police and firefighters.

Reporter Ed Mendel covered the Capitol in Sacramento for nearly three decades, most recently for the San Diego Union-Tribune. More stories are at https://calpensions.com/ Posted 25 Feb 13

February 25, 2013 at 12:49 pm

Public Sector pensions are so grossly “excessive”, when compared to what their private sector counterparts get.

When you PROPERLY factor in the very high additional costs of expensive provisions such as the very young full retirement ages and the post-retirement COLA increases (as well as the very liberal definition of “pensionable compensation”), the Taxpayer paid-for share of Public Sector pensions are ROUTINELY 2-4 times (5-6 times for safety workers) greater in value at retirement than the pensions (if any) of their Private Sector counterparts.

Beyond being grossly excessive, unsustainable, and unjust to taxpayers, with Public Sector workers now earning no less in “cash pay” than their Private Sector counterparts (per the US Gov’t BLS), there is ZERO justification for ANY greater pensions (or better benefits) let alone ones that are multiples greater in value. In addition, this “overcompensation” is CLEARLY unnecessary to attract and retain a qualified workforce.

Right now, ALL public Sector Pensions have significant unfunded PAST service liabilities using the Plans’ highly understated “official” funding figures (e.g., the 70% mentioned for CalPERS), and under PROPER (much more conservative) accounting (that GASB and MOODY’s will soon impose on these Plans) this underfunding will be 2-3 times greater.

But it gets worse …. we CONTINUE (EVERY DAY) digging that financial hole we are in even deeper by continuing to grant additional pension service accruals under today’s formulas and provisions that WE KNOW are unsustainable.

WHY ? Are Public Sector workers so “special” and deserving of MORE than the Taxpayers that pay their way that we should bankrupt our States, Cities, and towns by agreeing to the greedy demands of their Unions and the elected officials they have bought-off with campaign contributions and election support ?

AT THE VERY LEAST …. and putting aside the already huge unfunded pension liability for PAST service ….. we need to stop digging this hole deeper by hard freezing these grossly excessive Defined Benefit Pension for all CURRENT (yes CURRENT) workers and replace them for FUTURE service with a Defined Contribution (401k style) Plan with a modest Taxpayer “match” comparable to what Private Sector workers typically get from THEIR employers.

February 25, 2013 at 4:39 pm

Want grossly excessive? Here is a list of 21 private sector post-employment packages the value >$100 million… many of them from companies that either hold big public sector contracts or extract natural resources from publicly owned land…

Click to access GMI_GoldenParachutes_012012.pdf

And of course, lobbyists from the private sector make sure public taxpayer dollars bail out these companies if they have any problems at all.

For sure public sector pensions in California were raised to high. Why? Both Republican and Democratic legislators, duly elected by voters, voted unanimously or near unanimously for those raises. And both Republican and Democratic governors signed too. No doubt lobbying played a part, just as the private sector lobbies to protect the >$100 million packages in their sector.

The real reason public sector employees get their pensions is quite simple: they have duly negotiated contracts that bind the State of California to pay those pensions.

If any private sector company holds contracts (like, say, Exxon-Mobil’s lease agreements on public lands) you bet their fleet of lawyers work overtime to defend the contracts. Anyone who singles out public pensions for doing exactly the same thing is both ignorant and frightfully biased.

However, there is a way out: sovereign default of the State of California, which is like bankruptcy. Let Exxon-Mobil lose their public land leases as part of that process. Let every State bondholder loose their contractually guaranteed coupons. Let everyone share in the chaos… not just pensioners. No form of State agreement or debt should be privileged. Anyone who argues for special priority for their slice of California debt is just a chiseler.

As for Moody’s…. WHO CARES. They were fraud-plagued in the mortgage bond crisis of the 2000’s. They are a pay-for-play operation who just do what the payer wants.

As for 401(k)s… they are primarily a mechanism for the same investment bankers who crashed the economy in 2008 to get billions in new fees. Anyone who argues otherwise is naive. The average 401(k) fee is >0.8% per year, compared to 0.2% per year for CalSTRS and UCRP (CalPERS is bad, a 0.5% per year fee level, and needs reform).

Plenty of public DB plans in the US work just fine. After Sovereign Default of the State of California, getting back to reasonable public DB plans in California can get done.

February 25, 2013 at 7:39 pm

Quoting …”The real reason public sector employees get their pensions is quite simple: they have duly negotiated contracts that bind the State of California to pay those pensions.

They sure have …. “negotiated” with elected representatives who SOLD their favorable votes on pay, pensions, and benefits in exchange for Public Sector Union campaign contributions and election support …. bribery & racketeering, a crime in any other venue.

Taxpayers … RENEGE on any further funding of these grossly excessive pension “promise”. Who is going to pay for YOUR retirement ?

February 26, 2013 at 12:54 am

You mean those same representatives who have sold out taxpayers to make sure the captains of private industry have >$100 millions?

The taxpayers elected those representatives, TL. Who is at fault, taxpayer? Take a look in the mirror.

February 26, 2013 at 4:05 am

Spension, do you have anything to say regarding this article?

February 26, 2013 at 5:27 pm

I am very interested in the source of Mr. Dunmoyer’s assertion that the average female under age 30 will live to 100. This does not match US Census projections for the same gender and age group.

Click to access 12s0104.pdf

February 26, 2013 at 11:40 pm

“Public Sector workers now earning no less in “cash pay” than their Private Sector counterparts (per the US Gov’t BLS)”

Repeating this will not make it so.

When comparing total compensation in the general population, private compensation averaged $28.95 per hour. State and local compensation averaged $41.65 per hour. (Sept. 2012)

This is the infamous “apples to oranges” comparison. The BLS caveat on page four states, as always: “Compensation cost levels in state and local government should not be directly compared with levels in private industry.”

Either of two methods corrects this error: When comparing SIMILAR public and private occupations, total compensation is “roughly equal” or, even comparing “apples and oranges” between public sector workers and employees of large companies (500 or more employees), total compensation is roughly equal.

TOTAL COMPENSATION.

For private sector workers, cash pay accounts for 69.2 percent of compensation. For public sector workers, 64.7 percent

February 27, 2013 at 2:54 am

Douglas, while I not sure you are aware of the flaw, the fatal flaw in that comparison is inaccurate/misleading Govt data. While Private sector Plans report TRUE retirement costs (either because they are direct 401k contributions or because ERISA requires proper DB Plan funding), Gov’t entities report as the year’s retirement expenses what they CONTRIBUTE to the Plans in that year, NOT the MUCH MUCH MUCH higher actuarial ARC’s (annual Required Contributions) that they SHOULD be contributing. The same is true with respect to retiree healthcare promises. Gov’t entities report what they Pay in retiree healthcare costs in the year, not the MUCH MUCH higher amount accrued.

With that correction (which has been identified and pointed out by researchers), Public Sector “Total Compensation” (cash pay plus pensions plus benefits) is much greater, not in the ‘Cash Pay” component, but in the pensions & benefits components.

So now that YOU have been educated, I’m assuming you won’t repeat such incorrect comments, right ?

February 27, 2013 at 9:33 pm

Contra Costa County’s 37 Act system today dropped its rate from 7.75% to 7.25% matching that of Orange County’s system.

February 27, 2013 at 10:05 pm

I am reluctant to use the trite “LOL”.

I have been educated?

1) “with Public Sector workers now earning no less in “cash pay” than their Private Sector counterparts (per the US Gov’t BLS)”

or, 2) “much greater, not in the ‘Cash Pay” component, but in the pensions & benefits components.”

Which one are we going with? According to the BLS, total compensation is roughly equal, but benefit cost are a greater portion of public compensation, therefor cash pay is less, by definition.

Normally I would ask you to cite your studies, but I think I have read most of them. There is by no means a consensus.

Years ago, I heard Jim Eason on KGO talk about growing up in North Carolina. His aunt stopped by on her way home, and Jim’s mom said she had just picked some green beans, told her sister to take a “mess” home with her. His aunt said she had used most of her canning jars and couldn’t use a mess of beans. Jim’s mom said, “Well, take a half a mess, then” and she did.

I don’t know the difference between a “mess” and “half a mess”. Nor do I know the difference between “MUCH MUCH higher” and “MUCH MUCH MUCH higher”

If I remember correctly, the extra “MUCH” may be due to the notion some people have that “interest follows principal”, therefore taxpayers actually pay 90% of pension costs. Keep repeating that, also. Doesn’t make it so.

February 27, 2013 at 10:37 pm

Quoting …”Which one are we going with? According to the BLS, total compensation is roughly equal, but benefit cost are a greater portion of public compensation, therefor cash pay is less, by definition.”

Wow, did you not understand ANY of what I said in my last comment?

Let’s try again …

The BLS statement that “Total Compensation” (the total of cash pay, pensions, and benefits) is roughly equal in the Public and Private Sectors is WRONG, because while the Private Sector send CORRECT data to the BLS, the Public Sector sends INCORRECT data that significantly understates the true cost of annual pensions and benefits ……. the error being that they report what they SPEND in that year rather what is ACCRUED by its employees in that year.

And by the way … Interest DOES follow principal. You are in serious need of a financial education…..and clearly brainwashed by your Union’s BS.

February 27, 2013 at 11:04 pm

As for wage and total compensation comparisons, Chapter 2 of

Click to access Full_Report.pdf

starting on page 73 has a fairly involved discussion. There are all sorts of fine points, like, low-wage workers get better pay in public sector, and are fairly numerous, but high wage workers get worse pay in the public sector. Big companies in the private sector pay better than small companies. State government pays less than local government in California. Lots of issues… in the end the table on page 85 is their `typical’ comparison. The typical public sector worker makes $5,000 less per year than the big company worker, but gets $15K more in employer-paid pension and post-retirement health benefits.

As for this actual article by Calpensions: it is good that CalPERS is starting to run scenarios to see how often they end up in the soup. I just wish they would different scenarios: I wish they would evaluate alternatives where employer contributions were held constant, at, say, 17.65% (could be 16.2% pension + 1.45% for for CalSTRS or 10% pension + 7.65% for SS+Medicare), and then lowered pension benefits until the % funding stabilized in the long run.

I think post-retirement health care is not appropriately part of this discussion… the dysfunctional US healthcare system just confounds the pension discussion. In any case, I don’t think health care benefits in retirement are vested and thus can be reduced by a vote of the CA legislature + signature of the governor.

February 27, 2013 at 11:41 pm

1. I have no union.

2. Of COURSE interest follows principal. But once the employers contribution is transferred to CalPERS, the principal is the property of the retirees, managed by CALPERS.

My interest follows MY principal.

February 28, 2013 at 1:41 am

Douglas, You have a very short memory. Why re-visit the “Interest Follows Principal” discussion when we already discussed it at length last December. I made the following comment (addressed to you …. and to which you replied “No”. What has changed?):

***********************************************************************

Douglas, That’s fine … we can agree to disagree (re interest follows principal, etc.). But just a thought, between Girard Miller and CalPERS, who has more of a vested interest in distorting the truth ?

But here is an example to consider. One way to look at it is that “pre-funding” (which creates the asset pool from which interest is earned) is simply a mechanism to change the cash flow pattern between 2 extremes (Lump sum pre-funding of all costs up front, and pay the costs as they occurs with zero pre-funding). Now consider the extreme lump sum prefunding case….. say the promised benefit will be $1 Million payable in one payment 20 years in the future, and assume assets will earn 6%. Then a lump sum of $311,804.73 is required, becuase it would grow over 20 years to the $1 Million at 6% interest. Now suppose the split of costs between workers and Taxpayers is 25%/75% so the workers pay $77.951.18 and the Taxpayers pay $233,853.55. In THIS case you would argue that the Taxpayers’ cost is $233,853.55.

At the other extreme, neither the workers nor Taxpayers pay anything until 20 years hence, and then the workers pay $$250,000 and the Taxpayers pay $750,000. I’m sure, in THIS example you would agree that the Taxpayer PAID $750,000 for the SAME fixed benefit that has been promised the workers.

But how can that “fixed” benefit have 2 different costs ????

Now lets try this ….. we indeed choose to make one one payment at the end of the 20 years, the Taxpayers’ payment being $750,000. But quietly on the side, the Taxpayers (huddle amongst themselves and put $233,853.55 into a 20 year bank CD with a guaranteed return of 6%). Well voila, that $233,853.55 has grown to $750,000 at the end of the 20-th year … of which $750,000-$233,853.55=$516,146.45 is earned interest. Now no one would argue that the $516,146.45 is the Taxpayers’ money since it is in a CD in THEIR name.

So, is there really a difference if they pay the full $750,000 cost at the end or put $233,853.55 in year 1 into a CD and earn $516,146.45 in interest to get to the same $750K, and THEN take it out of THEIR pocket and pay the bill ?

February 28, 2013 at 5:01 am

“No” meant your argument was meaningless. While I was working, my employer paid me my salary. They deducted five percent for CalPERS, and paid “matching funds” (averaging about ten percent), also into CalPERS. These contributions to PERS were part of my total compensation WHILE I WAS WORKING. MY principal. MY interest.

When I first started with the state, there was no 401(k) or 457 program. After they became available, I began investing 5% monthly. By your reasoning, the return on that money is a “taxpayer” cost?

Sorry, “No”

February 28, 2013 at 3:05 pm

Take some classes …. economics or finance 101 …. usually free for old-timers at the local Community College.

February 28, 2013 at 3:19 pm

Douglas, The point isn’t WHO owns the interest (investment earnings). It’s that the only real monetary sources to pay for these pensions are the direct contributions from the workers and the Taxpayers, and those 2 sources ONLY share (in the proportions that they contribute) the TOTAL COST of the promised pensions, NOT that total cost less some artificial subtracted anount for investment earnings.

February 28, 2013 at 11:10 pm

Tough Love, as far as it goes, I see your point.

However, absent from your analysis is the value of the work performed by the employee.

The fix pensions first report made there typical example: public employees earn $5K less per year than private sector, but got $15K/year more in pension benefits, for a net compensation addition of $10K/year for the public sector.

So a reasonable argument might be to say 1/3 of the public sector pension was earned by the public sector employee, in exchange for fairly compensated work.

But there are complications… should public sector employee compensation be compared to large companies or all companies in the private sector? In most ways the public sector resembles a large company… but the confounding fact is that salaries in the CA public sector is often highest in the smallest entities… for example, my local water district has been incredibly generous in salary to its employees.

And that largess is provided by a locally elected district board, well known to everyone in my community. Local direct democracy in action. Go figure.

March 1, 2013 at 4:29 am

Spension, Here’s something that needs to added to these discussions (but is never mentioned), especially for the higher paid Public Sector workers with the most generous pensions (such as policemen & firefighters).

I have read numerous times (and the figures are consistent with my own calculations) that the 3@50 COLA-adjusted pensions costs a level annual 50+% of cash pay,

If the workers are contributing say 10% of pay, that leaves 40+% of pay due from the Taxpayers, which with (say) a $100K salary is $40+K from taxpayers.

Never discussed is that these workers are essentially getting a “tax-deferred” benefit double the 401K maximum allowed to Private Sector taxpayers. Another unfair benefit ……. perhaps any taxpayer pension contributions in excess of the year’s 401K maximum should be included in the workers taxable income.

If we are to ever fix the crazy CA structure that so benefits the workers to the determinant of Taxpayers, ALL of the beneficial elements (including the less noticeable ones such as this) must be factored into the “fix”. Getting rid of ALL unused sick day payouts and all pension “spiking” CERTAINLY belongs on such a “fix” list.

At some point an elected official needs to stand up to the Unions using words like …”Enough”, “No”, and “We don’t care what you got LAST YEAR.” and “Tough”.

The Target goal should be Total Compensation (cash pay + pensions + benefits) EQUAL (but not better) than their private sector counterparts.

March 1, 2013 at 1:07 pm

Sure, you can pick out cases like safety employees where the pension benefits are very high… or, perhaps, the case of Mark Yudof, UC President, who gets at $200,000/year pension for 5 years of employment.

It is as pertinent as my pointing out that in the private sector, 21 executives got >$100 million golden parachutes:

Click to access GMI_GoldenParachutes_012012.pdf

Both private and public sector have terrible excesses, and both get taxpayer bailouts. On the private side, look at AIG… and don’ try to tell me they all paid it back… they didn’t pay back the market-rate interest on the $trillions they borrowed, and they just borrowed more to apparently pay back the bailout.

On average, your favored DC plans just transfer more in fees (0.8% per year on average) to the Wall Street fraudsters. DB plans (well, except for CalPERS) have way less annual fees, like 0.2%, and with $100s of billions at stake, that is real money.

On average, lots of US public entities have good DB plans that are not in dire straits like California’s. So let’s stick with DB plans.

March 1, 2013 at 3:50 pm

Here something upon which I’d bet you would agree with me:

30-40 years ago the ratio of CEO pay to that of the average worker was about 20 to 1. Today it is 300-400 to 1. The result has been that the vast majority of all productivity gains have gone to the most senior management and business owners.

Fixing THAT should be the Democratic theme (because that “problem” is understandable …. even to the conservative middle class who usually support the Republicans) … that it needs to come WAY down, and since “business” and the “rich” will fight such “gross” pay reductions, then the citizens are justified in accomplishing that goal via VERY high (and progressively higher) taxes on those with the highest incomes to bring “NET” pay to a more reasonable level.

Essentially, if the powerful and wealthy won’t share the spoils of direct labor on the “front end”, than we should accomplish that “sharing” on the “back end” via a very highly progressive income tax structure.

My suggestion for marginal FIT rates:

$250K-$500K – 40%

$500K-$750K – 45%

$750K-$1M – 50%

$1M-$5M – 55%

$5M-$25M -60%

$25M+ -65%