Full funding of the troubled California State Teachers Retirement System was approved by the Legislature last weekend, with most of the additional $5 billion coming from school districts that get no offsetting money from the state.

With only one “no“ vote, lawmakers approved Gov. Brown’s plan to phase in a massive rate increase over seven years, nearly doubling the $5.8 billion CalSTRS currently receives each year from school districts, teachers and the state.

A California Teachers Association lobbyist told a two-house legislative committee in February the politically powerful union wanted additional school funding from the state to cover the cost of the rate increase.

But the legislation, AB 1469, does not raise the Proposition 98 school-funding guarantee to help school districts pay the new CalSTRS rates. And a “poison pill” repeals the rate increase if a court ruling requires the state to reimburse districts.

The only apparent relief in the state budget package that might make more money available for teacher salaries is a cap on school district reserves linked to passage of Brown’s “rainy day” state budget reserve on the November ballot.

The reserve cap was backed by the California Teachers Association but opposed by management groups on the other side of the labor bargaining table, the Association of California School Administrators and the California School Boards Association.

“The governor’s proposed increases in CalSTRS alone will phase in higher employer contribution rates for the next years, going from 8 percent (of pay) to 19 percent,” the management groups said in a joint statement before passage of the budget.

“This is more than the increased level of funding many districts will receive via the new funding formula and will have major implications as boards are finalizing budgets,” the two groups said.

A Brown school funding formula enacted last year gives more money to schools with the neediest students. After deep cuts during the recession, school districts are receiving more money from an improving economy and a voter-approved tax increase.

CalSTRS has been trying for about a decade to get a rate increase. Unlike most California public pension systems, CalSTRS lacks the power to increase annual rates paid by employers, needing legislation instead.

Much of the CalSTRS funding gap, now being painfully closed by squeezing school funding, is due to state and teacher contribution cuts and benefit increases enacted around 2000, when a booming stock market gave CalSTRS a brief funding surplus.

The state contribution was cut from 4.6 percent of pay to 2 percent. For 10 years, a quarter of the teacher contribution, 2 percent of pay, was diverted to a new individual investment plan. A half dozen small benefit increases included a longevity bonus.

CalSTRS would have 88 percent of the projected assets needed to pay future pension obligations if it had had continued to operate under the contribution and benefit structure in place in 1990, a Milliman actuarial report said last year.

Now CalSTRS is only 67 percent funded. A Milliman actuarial report in April showed CalSTRS received $5.8 billion from the state, school districts and teachers last year, while spending $11.3 billion on pensions and administrative costs.

Nearly half of CalSTRS costs were paid from investment earnings. Without a rate increase, CalSTRS was expected to burn through its $184 billion portfolio in 30 years, even if earnings average what critics say is an overly optimistic target, 7.5 percent a year.

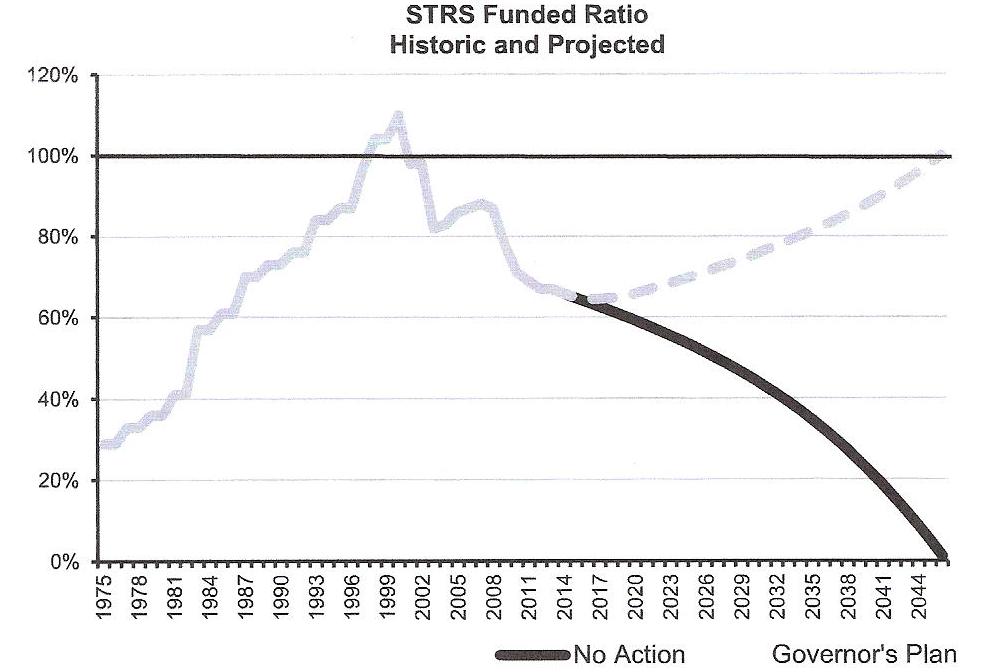

Department of Finance chart shows expected CALSTRS funding

Prompt action by the Legislature on the funding plan proposed by Brown last month is expected to ease or avoid the problem of reporting a huge CalSTRS debt under new accounting rules.

The CalSTRS board was told last September that under the new rules a $71 billion debt or “unfunded liability” (now $74 billion) could soar to a $166.9 billion “net pension liability,” an estimate now outdated by earnings and other factors.

It was not clear whether the big new pension debt would be reported by the state or the school districts or both. But there was concern that school district credit ratings might be lowered, increasing borrowing costs.

Under the new Governmental Accounting Standards Board rules, if projected assets using the expected return on investments fall short of covering pension obligations, a lower risk-free bond rate is used for the remainder, driving up the total reported debt.

The new legislation is a major shift of CalSTRS costs to school districts, community colleges and other employers, more than doubling their contribution while the state and teachers get much smaller rate increases.

The CalSTRS contribution from school districts and other employers increases, in seven annual steps, from the current 8.25 percent of pay to 19.1 percent of pay by July 2020.

The legislation reduces the initial school district rate increase proposed by Brown and some of the following step increases, but not the seven-year total. The change eases the impact on districts that already have budgets for the new fiscal year beginning July 1.

Teachers, currently contributing 8 percent of pay, get the smallest CalSTRS rate increase. In three-steps, the rate for most teachers will reach 10.25 in July 2016. For new hires with lower pensions under a Brown reform, the rate peaks at 9.205 percent in 2016.

Lawyers have told CalSTRS that a series of state court decisions mean the pension offered teachers on the date of hire becomes a “vested right” that cannot be cut, unless offset by a new benefit of comparable value.

The legislation provides a new benefit to offset the rate increase by declaring that an annual cost-of-living adjustment of 2 percent, now a routine practice that could be suspended, is vested in years when the rate increase is paid.

The state contribution to CalSTRS, currently a combined total of 5.5 percent of pay to two separate funds, increases in three annual steps to a total of 8.8 percent of pay in July 2016.

The state contribution to an inflation-protection account, which has a large surplus and keeps the pensions of retirees from falling below 85 percent of their original purchasing power, remains unchanged at 2.5 percent of pay.

But the state contribution to the main CalSTRS pension fund with the huge shortfall, now about 3 percent of pay, will increase in three steps to bring the total state contribution to 8.8 percent of pay.

The non-partisan Legislative Analyst’s Office has suggested that CalSTRS be given the power to set employer rates, like other public pension funds. The new legislation does give CalSTRS some rate-setting power, but it’s tightly limited.

CalSTRS can increase the employer rate after 2020 if needed for full funding by 2046, but only by a little more than 1 percent of pay. CalSTRS can increase the state rate after 2016, but only to eliminate debt for benefits in effect prior to 1990.

Reporter Ed Mendel covered the Capitol in Sacramento for nearly three decades, most recently for the San Diego Union-Tribune. More stories are at Calpensions.com. Posted 18 Jun 14

June 18, 2014 at 12:06 pm

Dear Taxpayers…

Refuse to fund anything greater (as a % of pay) than what YOU get towards YOUR retirement from YOUR employer …. rarely more than 3% of your pay into a 401K Plan.

With the new changes, the total ADDITIONAL taxes from YOU is an ADDITIONAL 14% of pay … on top of the 11% you are now paying towards teacher’s pensions …. (via State and local CalSTIRS pension contributions from YOUR taxes)

So they want !4%+11% = 25% of pay for teachers pensions FROM YOU, vs the 3% that you typically get from your employer.

Just say NO !… Reduce the Pensions. No Tax increases. Taxes should be REDUCED, not increased as the current level by itself is grossly unfair.

And…. why should Taxpayers contribute ANYTHING toward the retiree healthcare costs of Public Sector workers when their employers RARELY contribute anything to their own retiree healthcare costs ? Demand that ALL such subsidies end now.

June 18, 2014 at 4:33 pm

Most teachers don’t get retiree health care covered. I know my district doesn’t. With cops and firefighters, considering the damage to their bodies, it seems fair.

June 18, 2014 at 5:13 pm

The Department of Finance chart shows expected CALSTRS funding ratio going up immediately with the governors plan. Is that correct? Isn’t the annual interest service on the existing unfunded liability or $74 billion at 7.5% over $5 billion? (I’m assuming assets aren’t there, unfunded liabilities, need the same return as assets on hand.) Yet the increase in annual funding doesn’t reach that level for years. Wouldn’t that mean the unfunded liabilities would continue to grow, assuming CalStrs existing assets earn their assumed rate of return?

June 18, 2014 at 5:24 pm

Dear Taxpayers…

Please consider the TOTAL COMPENSATION of todays teachers, NOT just the pension costs.

There are studies (with conflicting results, look at several and decide which is is most realistic) which give the total compensation of teachers.

Cash pay plus vacation and sick leave, holiday costs, pension costs (widely varying, look at the TRUE cost discounted at riskless rates) healthcare costs, retiree healthcare costs, etc. Caution, these costs are NOT the same for all teachers or school districts. Many do NOT provide retiree healthcare, and pension formulas are not all the same.

If what is computed as the total compensation is roughly equal to, or less than a private sector worker with similar age, education, experience, responsibilities, etc. they are NOT being overpaid. You are NOT being ripped off.

The pensions are not an additional perk. Their cost is INCLUDED in the total compensation. The rate increases are not an increase in pensions. They are a correction for past UNDERfunding.

AND they are legally required.

June 18, 2014 at 5:58 pm

Sdouglas47, Ok, fair enough. So here’s where we are….

With the new proposal, CalSTIRS Taxpayer pension contributions are (from my prior comment) 25%-3%=22% of pay greater than those of Private Sector employers, and (per CalPERS studies, which I’ll assume are comparable to CalSTIRS costs) retiree healthcare is worth a level annual 12% of pay (generally vs ZERO for Private Sector workers).

So we need to start the Public/Private Sector “Total Compensation” comparison with a 22% of pay pension advantage plus a 12% of pay retiree heathcare advantage totaling of 34%. Actually we likely should add something (perhaps another 5+% of pay) for the often quoted “Cadillac” healthcare plan granted ACTIVE Public Sector workers vs the “Yugo” Plan granted typical Private Sector workers.

So …. I challenge ANYONE to show that the 34% (likely 40% with the Active healthcare Plan advantage) Public Sector pension/healthcare “advantage” is offset via wages 34% (or 40%) lower than their Private Sector counterparts.

June 18, 2014 at 7:53 pm

So the children who have been hit with the education budget cutbacks will be paying for the 1999 pension increase when they are working in 20 years, because today’s older folks don’t want to.

June 18, 2014 at 8:31 pm

First: This from Marcia Fritz at Fix pensions first.com, July 7, 2011 :

” Teachers’ retirement benefits aren’t the problem. Our report shows that teachers contribute more of their salaries and collect less in benefits than other public employees. ….. Since teachers aren’t covered by Social Security, their lifetime retirement income is about the same as retirees from large Silicon Valley companies who participate in their employers’ 401(k) plans, earn similar annual wages and retire at the same age.

…………….

Second: as has been stated several times, many teachers do NOT receive retiree healthcare.

…………….

Third: TL math, “assumptions”, and other misleading propaganda:

” I’ll assume………… retiree healthcare is worth a level annual 12% of pay ”

Assume away, but, in addition to the fact that many teachers have NO retiree healthcare, before you fire up your spreadsheet….

“level annual 12% of pay” is an AVERAGE figure, it’s a relatively constant AMOUNT for each employee, not a constant percentage. Employees who earn $30,000 or less will therefore have a higher percentage of income as retiree health costs, while higher earners will have a LOWER percentage. Healthcare and retiree healthcare are a flat dollar benefit, NOT a percentage of pay, on an individual basis.

……………..

Fourth: What, precisely, is your definition of “Cadillac healthcare plan”? I can tell you that the plans offered by CalPERS do not, even remotely, meet the definition used by IRS. I have read of some such ” Cadillac” plans offered to university presidents, city managers, and other high level positions, along with perks like housing allowance, car allowance, etc., but not for anyone I know.

……………….

Fifth: I’m sure you understand the ” true cost” of pension benefits, using risk free rates. These values, or costs, used by financial economists, are usually more than reported ARCs. When an entity contributes less than the true cost, the true total compensation is still the same. Likewise, when the government pays MORE than the true cost, like when in paying down unfunded liabilities, as in this case, the additional payments are NOT calculated as an increase in compensation. Total compensation, whether the government skips payments or pays more than required, is still the same.

This “true cost” is what Biggs and Richwine use in computing total compensation. Their general conclusion:

“Individuals with less than a high school education receive a total compensation of 22 percent…..master’s degree holders a penalty of 3 percent; professional degree holders a penalty of 17 percent; and PhDs a penalty of 18 percent.”

(Keep in mind, these are TOTAL compensation, not just cash wages.)

Biggs again:

“Nevertheless, a significant total compensation penalty remains for both professional and doctoral holders. It is worth considering how government may continue to attract better-educated employeets despite a seeming compensation penalty.

…………………

Finally, Fritz, Biggs, and Richwine are not union thugs or in collusion.

And I am not a teacher, or a police officer.

June 18, 2014 at 8:51 pm

Sorry, “total compensation PREMIUM of 22 percent.”

for those with less than high school education.

June 18, 2014 at 9:40 pm

No Larry, It’s NOT because the “older folk” don’t want to pay for fair-generosity pensions. It’s that they don’t want to pay for the current Grossly Excessive Public Sector pensions & benefits.

The rightful solution is NOT to raise taxes to pay for this GROSS EXCESS, but to MATERIALLY reduce the promised pensions & benefits to a level no greater than what the typical PRIVATE Sector worker gets …….. assuredly, no more than 1/4-1/3 of the current pension & benefit promises to PUBLIC Sector workers..

June 18, 2014 at 11:51 pm

“Grossly Excessive Public Sector pensions and benefits”

The WORD,

according to Tough Love!!!

June 19, 2014 at 12:30 am

SDouiglas47, Your explanations don’t hole water, for the following reasons:

Re your “First” comment:

Marcia Fritz was comparing CA teacher pensions to other PUBLIC Sector CA worker pensions. Sure they are lower, but she wasn’t comparing CA Teacher pensions to typical PRIVATE Sector pensions which would be far lower than those granted teachers. THAT is the PROPER comparison.

And Teachers BENEFIT by NOT belonging to Social Security because SS is a VERY lousy return on investment for all but the lowest paid workers. Assuredly the 6.2% of pay that their employers would have contributed to SS is already in their pay scales, and if they aren’t saving and investing the 6.2% that they would have paid into SS from their own net pay, then that’s THEIR stupidity and not the Taxpayer’s problem.

Additionally Marcia Fritz’s study was from 2011, so even IF (a BIG IF) teacher compensation is near that of the the small subset of Private Sector works with high “Silicon Valley” retirement Plans, that study certainly didn’t include the ADDITIONAL 14% of pay CalSTIRS is now demanding from Taxpayers. So from that ALONE, there is AT LEAST a 14% Public Sector teacher compensation advantage.

Re your “Second” comment:

You said “many” teachers don’t get retiree healthcare benefits. I doubt that. And is “many” 10%, 30%, 50% ??? Prove that statement from a reliable source (which means one not funded by your Unions).

Re your “Third” comment:

Yes the 12% of pay is the “average” (level annual % of pay) cost of CalPERS retiree healthcare. Of course the actual cost to each member varies with their pay. So what ?

And there is no reason to believe the average cost to CalSTIRS is materially different than CalPERS retiree healthcare costs. Here is the source of the 12% from CalPERS (in the next to last paragraph in this link): http://www.publicceo.com/2014/02/resolving-one-debate-on-public-sector-pay/

Re your “Fourth” comment:

“Cadillac” health Plans are very costly Plans because they tend to include VERY generous benefits, few limitations, low copays, low deductibles, and low (if any) coinsurance share paid for by the insured. These are the Plan most often offered to Public Sector workers and usually with worker-paid premiums far lower that Private Sector workers pay for FAR less-generous coverage.

A good example of “Cadillac” Plan generosity can be found in this article on the Detroit bankruptcy…. here:

http://www.detroitnews.com/article/20140612/METRO01/306120134/0/METRO/Non-Medicare-eligible-Detroit-retirees-given-new-Cadillac-plan-health-care-option

Even though certain younger Detroit retirees knew they were losing their retiree healthcare coverage, they requested that a “Cadillac” Plan (similar to what they received pre-bankruptcy) be made available to them even if they had to fully pay for it. Well, Detroit obliged, with a “Cadillac” Plan with a monthly cost for family coverage of $3,911.17 (that’s $46,934.04 annually !). Yup, THAT’s the coverage level that Detroit’s Taxpayers likely covered pre-bankruptcy. No wonder why they went bankrupt. This level of Public Sector Union/workers greed and avarice for the Taxpayers is disgusting !

Re your “Fifth” comment:

You are likely correct that high level “professionals” (e.g. doctors, lawyers, PHDs, etc) in the Public Sector receive lower “Cash Pay” than their Private Sector counterparts, It’s certainly also true for the executive administrator of major cities such as LA or SF. Whether they earn less in “Total Compensation” is clearly an individual calculation, and because DB pensions are so “back-loaded”, I’d guess that a 30-year career Public Sector CA doctor earns no less in total compensation due to the HUGE pension THEY (but not the Private Sector doctor) will get. Such high level Public Sector professionals who leave Public Sector employment w/o vesting a pension likely do poorer than their Private Sector counterparts.

Keep in mind that these high level professions (in total) are a small proportion of all Public Sector workers, Even IF this small group earns less, that certainly does not justify materially overcompensating the MUCH MUCH larger group of all OTHER Public Sector workers ….. as is indeed the situation today.

June 19, 2014 at 12:44 am

Tough Love, you’re forgetting Social Security.

Before this refinancing plan, districts were paying 8.25%, which was 2.05% higher than Social Security would be if they paid it. Think of it as 2.05% to a defined contribution plan, which is less than the match many private sector employers offer.

Remember, you have to offer competitive compensation to attract and retain a professional workforce. You may not like teachers, but they are all four-year college graduates.

With the new funding plan, their compensation will increase but their salaries, probably not so much.

June 19, 2014 at 1:12 am

Anon Enigma, First of all, it’s not 8.25%. The CURRENT combined State and Local CalSTIRS contributions from Taxpayers is 11%.

And, what makes you think the 6.2% of pay (NOT paid to SS on their employee’s behalf) is not ALREADY reflected in current pay scales? If their employers WERE contributing to SS, the employee’s cash pay would likely be 6.2% LESS to keep Total Compensation the SAME.

June 19, 2014 at 1:51 am

Yeah, TL, I’ll get right on that research for you. Maybe mañana. The pool won’t clean itself, and pool service ain’t in my budget.

LOL!!!

Bottom line, “Grossly Excessive Public Sector Compensation” is a gross exaggeration.

June 19, 2014 at 2:12 am

The idea that teachers should take less because the private sector has walked away from its pension obligations is wrong. Instead, private sector pensions need to be reinstated to their previous levels. As for healthcare, this retired teacher receives zero benefits. Obviously there are haters out there pulling feces out of their rear ends to support their fallacious arguments.

June 19, 2014 at 2:32 am

Bla, bla, when you spend above your means, bad things happen.Period. Any opposition to that is like saying, my farm is great, no care, no rain.daaaaaaa, you starve. I don t have to save, my money will grow at 7.5 percent, no issues ok…..you will be food. Factor that into your retirement plans. Grandma got run over by the reindeer, and grandpa was a dumb ass. Will look good on your grave.

June 19, 2014 at 3:22 am

SDouglas47 Says: “Yeah, TL, I’ll get right on that research for you. Maybe mañana. The pool won’t clean itself, and pool service ain’t in my budget.

LOL!!!

Bottom line, “Grossly Excessive Public Sector Compensation” is a gross exaggeration.”

Give your argument a well deserved rest, SDouglas. Grossly excessive public sector compensation, which rarely accounts for unfunded pension liability costs, or unfunded retiree-health care costs, at least when it comes to the BS comparable compensation salary-surveys, which only use a select few other government agencies to compare/justify their excess, is just plain nonsense.

I know what I see – and none of it supports your argument.

June 19, 2014 at 3:39 am

I know a retired school admin getting $100k pension. His child is a beneficiary and will receive 50k for the rest of their life.

If they both live to 70 it puts this single retirement package around $4 million.

http://www.pensiontsunami.com

June 19, 2014 at 3:49 am

deadsurfer Says: “The idea that teachers should take less because the private sector has walked away from its pension obligations is wrong.”

The private sector hasn’t walked away from anything. Actually, they’re getting screwed. The reason the teachers pension is onlly 67% funded, instead of 88% funded, is because the teachers only contributed 75% of their required contribution for over a decade, while diverting investment returns to perks other than their pensions (seperate cash balance accounts, longevity bonuses of 500 dollars per month, retiree healthcare subsidy accounts, 85% buyer protection accounts – all while they were receiving 2% COLA’s that were never a part of their contract with the state of CA – Why? Apparently the CTA is dictacting terms & conditions and our lousy politicians continue to cave).

The teachers union, with the help of CalSTRS, have created their own mess and now they want our school districts to pay for their BONE-HEADED attempts to feather their own nests while the Pension Egg rotts. Ultimately the school districts will cry poverty, say something about “it’s all about the kids”, and ask for money from tax payers. CalSTRS and the Teachers Union will endorse the PARCEL TAXES, SCHOOL BONDS, INCREASED SALES TAXES, AND EVERY BALLOT MEASURE that provides additional pension funding – “because it stays in the classroom”.

While all this was happening the CalSTRS Board just approved an additional 300 million dollars in Teacher Perks which will be charged to … the taxpayers. Based on that decision you’d never know the pension system was projected to go broke in 30 years. You just can’t make this stuff up.

June 19, 2014 at 8:24 pm

First:

The value of benefits accruing in a given year is the normal cost. It is NOT the amount the employer contributes to the plan in that year.

A 14% increase in contributions is NOT a 14% increase in Public Sector teacher compensation, any more than an employer “holiday” from pension contributions is a reduction in teacher compensation.

June 19, 2014 at 10:06 pm

Second:

https://www.google.com/url?sa=t&source=web&rct=j&ei=51yjU-W6GcaFogSt7IGwBw&url=http://www.calstrs.com/sites/main/files/file-attachments/employer_health_benefits_study_2012.pdf&cd=1&ved=0CB4QFjAA&usg=AFQjCNHa9Z-WbkHoT1LcNcuzQyP1tO9fUg&sig2=e8FxfToHG30kPc4bFlj-PQ

June 19, 2014 at 11:00 pm

SDouglas47, Seems that you have not been accurately following the proposal for increases in the taxpayers (via increases at the State & Local levels) CalSTIRS contributions.

The proposal is for a total (State + local) increase of 14% of pay.

That’s certainly NOT a 14% increase in the the prior level of Taxpayer contributions, but INDEED it is a 14% increase in compensation costs to the Taxpayers.

June 19, 2014 at 11:29 pm

Third:

OK, you got that completely bassackwards. The PERCENTAGE varies with pay. The actual cost does NOT very with pay. It is a flat dollar benefit. Biggs uses an example of $12,802 (that is healthcare PLUS retiree health care accrual, presumably on a national average)

Whether one makes $34,000 or $90,000, the benefit is still $12,802. So for the $34k employee, health benefits are 38% of salary, and for the $90k employee, it is 14%

Why is that important? Because some innumerate dildo with a spreadsheet will combine two facts: the average cost of retiree healthcare is 12% of pay, and this teacher earns $100,000 a year, therefore: this teacher receives $12,000 a year for retiree healthcare. He would be wrong. He would also be wrong if he calculates that a $30,000 a year employee receives $3,600 towards retiree healthcare.

That is why we laugh at TL math.

GIGO

………………..

” And there is no reason to believe the average cost to CalSTIRS is materially different than CalPERS retiree healthcare costs.”

There is one very good reason….. CalSTRS does not provide health or dental insurance coverage. It’s all done through local districts. Hence the great variety in coverage.

June 19, 2014 at 11:49 pm

TL: ” So from that ALONE, there is AT LEAST a 14% Public Sector teacher compensation advantage.”

SD47: ” A 14% increase in contributions is NOT a 14% increase in Public Sector teacher compensation, any more than an employer “holiday” from pension contributions is a reduction in teacher compensation.”

…………….

I don’t know how I can make that more clear. Unless there is an increase in the retirement formula, there is NO increase in teacher compensation. No teacher will receive ONE MORE DIME as a result of this change in funding.

June 20, 2014 at 12:08 am

Fourth:

CALPERS rates are $642 for an individual, $1,218 for employee and one dependent, and $1,559 for a family.

Not Cadillac.

June 20, 2014 at 1:40 am

Fifth:

TL: ” I’d guess that a 30-year career Public Sector CA doctor earns no less in total compensation due to the HUGE pension THEY (but not the Private Sector doctor) will get.”

……………

You might “guess” that, but Biggs and Richwine “data” says professionals and PhDs have a 35 to 37 percent disadvantage in cash pay, and 17 to 18 percent disadvantage in total compensation. The total compensation INCLUDES the cost of pensions and retiree healthcare, computed at a risk free discount rate.

The HUGE pension THEY will get is already calculated in. It’s not an extra perk. Don’t count it twice.

By the way, their calculations show those with a BA have approximately a 2% advantage over equivalent private sector workers (total compensation.) I would call that “roughly equal”, and most over that level would be UNDER compensated compared to the private sector.

Probably more than ” a small proportion of all Public Sector workers,”

Briggs and Richwine are not in collusion with my union.

But then, I don’t have a union, so………

June 20, 2014 at 2:04 am

SDouglas47 … clearly you have a PHD in twisting the truth.

June 20, 2014 at 3:21 am

I’d ask you to be specific, but I’m afraid I’d just see more of that ludicrous math.

June 20, 2014 at 4:07 am

You can’t make this stuff up!

June 20, 2014 at 1:03 pm

SDouglas47,…. YOU can, YOU have.

June 21, 2014 at 12:34 am

SDouglas47 Says:

“CALPERS rates are $642 for an individual, $1,218 for employee and one dependent, and $1,559 for a family. Not Cadillac.”

Note true – at least for every California state/local employee group I’m aware of. Maybe you can provide the link? What is true is that these costs are mostly UNFUNDED (for yet to retire employees and retirees. There are STILL many employees receiving medical benefits of 24K per year. You know, the ones with the front of line/concierge service. As ridiculous as that sounds it is very true. But who cares, It’s only taxpayer dollars!

June 21, 2014 at 4:44 pm

Can’t find that link. While searching, I did find a site indicating one California city (forgot which one) that had an employer contribution of over $1,900 a month for family coverage (three or more persons) for law enforcement. That’s close to $24k per year. A LOT of money. I am sure that’s not the only entity with that kind of insurance.

If I may, this is one of the reasons I don’t mind being a pest on these boards. There are problems with pension costs. There are problems with insurance costs. They should be dealt with.

Properly.

Not knee jerk counterproductive emotional BS.

TL’s post:

” Actually we likely should add something (perhaps another 5+% of pay) for the often quoted “Cadillac” healthcare plan granted ACTIVE Public Sector workers vs the “Yugo” Plan granted typical Private Sector workers.”

Implies, whether intentional or not, that Cadillac health plans are the norm. They are not. As I recall (and no, I don’t have a link) the average for CalPERS is a little over $10k per year, considering the mix of single, married, and family subscribers. And, yes, as TL mentioned, there is an ADDITIONAL benefit of 12% (average) for the value of future retiree healthcare, calculated at the risk free discount rate. (Actually, the most up to date figures I saw say 13%)

Minor point. When the “Cadillac” healthcare tax kicks in, it will be for those benefits over $27,500. For Law Enforcement, and certain other occupations, it will be $31,000.

………….

$100,000 pensions. Full retirement at 50. Free healthcare for life. These things do happen. But I get the distinct impression reading these blogs that most people believe this is typical public sector pay. It is not. And there are some simplistic, frankly dumbassery, remedies.

“Cap all pensions at $50,000”. (That one wouldn’t affect me personally, but it’s dumb anyway.)

“MATERIALLY reduce future service accruals by 50+%, ..” (total, simplistic, inane dumbassery)

“Convert all DB plans with defined contribution.” (Throw the baby out with the bathwater)

…………

” BS comparable compensation salary-surveys, which only use a select few other government agencies to compare/justify their excess, is just plain nonsense.” said the Captain.

?????????

The paradox; there are THOUSANDS of public sector retirees who actually retire with about what is called the “average” pension of $2,400 a month. I’m not talking “those who retired long ago under lesser formulas, or survivors on half pensions, or part career workers”. People who retire THIS year, after thirty years or more. CalTRANS maintenance workers, many clerks and laborers, even with Social Security, and (non Cadillac) healthcare, will be at or near poverty level.

BUT WAIT!!!!

They will be better off than private sector workers of ” equivalent” education and work experience.

Correct. The lowest paid public sector workers are typically (nothing is “always”) the MOST “overcompensated” in comparison with their peers. *much of the reason for this is healthcare. If a worker with $3,000 month salary has a family, his healthcare benefit alone is an additional $1,500 or more.

And many (again, not “always”) of the highest paid and benefitted employees and retirees are the MOST ” under compensated”.

Most of the knee jerk proposals will make them even more under compensated.

June 21, 2014 at 5:46 pm

Part deux……….

” BS comparable compensation salary-surveys”

I believe a have posted links, cited, or referenced, several times, studies on BOTH sides.

Particularly:

http://www.heritage.org/research/reports/2011/03/are-california-public-employees-overpaid

http://www.publicsectorinc.org/2014/06/public-employee-pay-state-by-state/

Yes, most other “liberal” studies will say that public workers are compensated……

ON AVERAGE…..(capitalized, stressed, emphasized. )

“less than OR roughly equal to” equivalent private sector workers. Total compensation. Including the present cost of pensions and retiree healthcare.

Both the above studies, by Biggs and Richwine, come to a different conclusion:

ON AVERAGE…..(capitalized, stressed, emphasized):

California public workers* are compensated at “as much as” 130% of their private sector counterparts.

*the first study, as I recall, is all state AND local workers, while the second is state workers only, because it’s intention is comparing all state workers nationwide.

Point being, the headlines and the bloggers will stress the 130%. Little or no mention of methodology or specific data within the study.

130%!!!!!

AVERAGE?????

I encourage anyone to read, carefully, with an open mind, twice, if necessary, both reports. Particularly the latest.

Page 46:

Individuals with less than a high school education receive a total compensation premium of 22 percent: high school graduates receive a premium of 19 percent: individuals with some college receive a premium of 13 percent: college graduates receive a premium of 2 percent: master’s degree holders a penalty of 3 percent: professional degree holders a penalty of 17 percent: and PhDs a penalty of 18 percent. *

……….

Nevertheless, a significant compensation penalty exists for both professional and doctoral degree holders. It is worth considering how government may continue to attract better educated employees despite a seeming compensation penalty. *

*1. There are no quotation marks above because I was not able to copy and paste from the PDF. I manually typed the paragraphs, and proofread, but there MAY be errors. I encourage everyone to read the original. All of it.

2. There are several sentences I omitted between these two statements. It was for the sake of brevity, not meant to mislead. Again, please read ALL the original.

3. As I understand, the above figures are NATIONAL averages, not specific to California.

June 21, 2014 at 7:25 pm

Part tres…………..

What does it matter? Who cares? Why compare compensation anyway?

Since I can’t copy and paste, again, please read the introduction (read the whole report) of the second link in particular:

http://www.publicsectorinc.org/2014/06/public-employee-pay-state-by-state/

It is not a direct link, click the “working paper” link in the article.

……………..

If public workers are OVER compensated, it is a needless expense to taxpayers. If they are UNDER compensated, the state will have difficulty attracting and retaining the employees it needs.

Simple answer; if California state workers are compensated thirty percent above equivalent private sector workers, reduce everyone’s compensation by thirty percent.

” For every complex problem there is an answer that is clear, simple, and wrong.”

H. L. Mencken

It matters very much who you cut, and where. Across the board cuts won’t cut it. (Sorry, couldn’t help myself)

Cut the cash pay of professionals by 30%, and you will have no more professionals. Cut the cash pay of lowest paid workers by 30% and you violate minimum wage laws. (Many of the lowest paid state workers already qualify for various public assistance programs: section 8 housing assistance, child care subsidies, SNAP, WIC, EIC, etc.). But not MediCAL.

Cut healthcare costs? Keep in mind what I (attempted to) explain to TL: healthcare is a constant dollar benefit. On average, if your cash wages are $30,000 a year, your health benefits are a little over $10,000 a year. If your cash wages are $150,000 a year, your health benefits are still $10,000 a year.

(Yes, retiree healthcare costs, even though unfunded, are a constant dollar benefit also.) Equal to about 13% of AVERAGE salary. If you “ASSUME” the average cash salary is $70k, then the value of retiree healthcare would be about $9,100 additional “compensation” per year. In that case, it would be $9,100, whether the worker earns $30,000 or $150,000. Still $9,100. A $150,000 employee does NOT have a retiree health compensation of $19,500 a year ($150k x 12%), it doesn’t work that way. (And, it is MUCH more complicated. Do NOT try to put any of these numbers in a spreadsheet. “Don’t try this at home”. )

My sincere apologies for the SDouglas math. I can state with utmost certainty that the value is NOT $9,100. A classic example of GIGO. It was an example of the principle ONLY.

Point being, even though I, and certainly other researchers, will have criticisms of Biggs and Richwine’s data and/or methodology, the importance of their study, after being properly vetted and critiqued, is not the GOTCHA. “132%”!!!!! average public pay advantage.

AVERAGE

(capitalized, stressed, emphasized. )………..AVERAGE

The point is to look at the mix of cash pay, benefits as a percentage of pay, and constant dollar benefits and see where cuts (or increases) can be made to reasonably attract and maintain a quality workforce without unnecessarily wasting taxpayer money. It’s not as easy or simple as you might think. In fact, it’s most likely a Gordian knot. You will NEVER satisfy all parties and NEVER have TLs dream that public sector workers will have NOT ONE PENNY MORE (or less) than the taxpayers who “support” them.

If you don’t like the “liberal BS studies” which I have cited and linked in the past (by the way, I would strongly encourage reading some of them ALL the way through, not just the “roughly equal” conclusion), and you disagree strongly with Biggs and Richwine when they say the “average” is 130%…BUT…some professionals are under compensated (significantly), then I suppose the final arbiter might be Rush Limbaugh:

” but you tell me why somebody on your street should pay you twice what he earns and then promise you health care and salary for the rest of your life after you quit working?”

The ultimate of dumbassery, on SO many levels.

If you still think I’m blowing smoke up your skirt, so be it. I have been wrong before.

June 21, 2014 at 7:31 pm

Finally, while my “comment is awaiting moderation”

( I can’t imagine why, since my middle name IS “Moderation”.)

The pH in the pool is 7.4, water temperature 82, and my current library book is due back by Monday, so I wish you all a pleasant weekend while I work on my melanoma.

June 22, 2014 at 9:25 pm

round and round the argument always goes…

As for the private sector, here is a list of 21 private sector CEOs with post-retirement packages that exceed $100 million:

Click to access GMIRatings_GoldenParachutes_012012.pdf

Let’s see a list of public sector employees that get greater than $100 million in post-retirement benefits.

Of course the rank and file in the private sector don’t get $100 million payouts. The Fix Pensions First report (Page 24 of

http://www.fixpensionsfirst.com/docs/Full_Report.pdf ) shows the comparison of all post-retirement benefits… about 20% higher for teachers than for the private sector.

As for what happened to the private sector, well, it is quite clear that the CEOs (who get the $100 million payouts) used every trick they could think of, including consultants, law changes, Washington regulatory influence, etc, to grab $ out of the private retirement pools:

http://www.retirementheist.com

Remember: Tough Love is someone who benefits from the privatization of retirement funds. He has no interest in being fair in any way.

Me, I’m just a girl who started studying my totally Defined Contribution system, and realized the private sector was charging trips to the Kentucky Derby for executives etc to the fees I had to pay for investment houses to hold my funds. And they have arbitrary power to hike fees for any reason and no reason… read about Shankar Iyer at:

The 401(k) industry is even more corrupt than the worst things Tough Love says about the public sector… see:

http://www.pbs.org/wgbh/pages/frontline/retirement-gamble/

No way should the 401(k) industry get public retirement funds. That public pensions got to high is absolutely true, but guys like Tough Love just want to steal every penny they can.

June 23, 2014 at 12:32 am

My employer’s contribution to my medical coverage after the required 25 years’ service is $532/mo for ABC, PPO. My premium is $1,000/mod for coverage secondary to Medicare. I pay the difference, plus another $1,000 for my dependent spouse. There is nothing Cadillac about that, Captain. If you know all there is to know about the medical coverage of hundreds of municipalities in CA and the other counties, and special districts, you are certainly busy minding everyone’s business but your own. When do you find time to make your own living?

June 23, 2014 at 1:53 am

Quoting Spension ..”Remember: Tough Love is someone who benefits from the privatization of retirement funds. He has no interest in being fair in any way.”

Remember ?

Form Where? Form What? From When?

I have not and do not (and will not) make ANYTHING from “privatization of retirement funds”.

Lying ASSHOL*

June 23, 2014 at 2:04 am

Contrary to what the enormously biased Spension says ……… the following is a link to an unbiased “scholarly” (and well footnoted) article discussing the many myths about switching Public Sector pensions from DB to DC Plans ……. the title of which is:

“Addressing Common Objections to Shifting from Defined-Benefit Pensions to Defined-Contribution Retirement Plans”

http://reason.org/news/show/pension-reform-defined-contribution

June 23, 2014 at 4:57 am

Wait for it……………

June 23, 2014 at 2:45 pm

OK,

Spension is “enormously biased”.

Reason.org is ” unbiased and scholarly”???

June 23, 2014 at 3:54 pm

Its just another offshoot of the California Public Policy Center, SD47; the premier haters of public sector workers.

June 23, 2014 at 5:20 pm

YES

June 23, 2014 at 9:46 pm

I didn’t want to belabor the point, SeeSaw.

It’s too obvious.

Sixty seconds on any search engine and D Koch stands out as a major contributor.

BUT………….

They got footnotes!! Must be true!!

LOL!!!!

June 23, 2014 at 11:18 pm

SeeSaw, and wouldn’t it be MUCH more accurate to call the group … “Citizens for Retirement Security”…..

the … “Public Sector Union suck-the-money-out-of-the-taxpayer’s-pocket Advisory Center” ?

June 24, 2014 at 1:23 am

THIS article sums up the Public Sector pension fiasco situation EVERYWHERE perfectly.

Just substitute YOUR City/State for Illinois:

http://www.chicagotribune.com/news/opinion/letters/chi-letter-taxpayers-are-the-real-victims-of-pension-underfunding-20140623,0,5874616.story

June 25, 2014 at 7:17 pm

Tough Love is in the private investment management industry, which always benefits from the conversion to DC funds.

As for http://reason.org/news/show/pension-reform-defined-contribution, the acknowledge the extra costs of DC plans, and they try to get around the problem by concocting a solution that is not on the table in any discussion. Might work, might not, but there is no regulatory corpus nor is the private investment management industry (where Tough Love works) lobbying for it.

Ditto for longevity risk.

The reason.org solution: if elephants were pink and could fly, all would be well. But real elephants are grey and can’t fly.

June 26, 2014 at 2:26 am

Spension, Ho hum, just more BS to further your self-interested support for the untameable DB pension structure.

June 27, 2014 at 5:41 am

Tough Love, Ho hum, just more BS to further your self-interested support of your own bank account. How much do the investment banks pay you for your spam? Is it by the word?

June 27, 2014 at 8:40 pm

spension, ZERO. I comment solely as a well trained (very frustrated) Taxpayer who fully understands the huge depth of the Public Sector Union/worker pension & benefit financial “mugging” of the Taxpayers.

I don’t think anyone pays YOU, I think you’re just nuts.